{kind=link}

In one of the doubtlessly transformative coverage modifications within the historical past of upper schooling coverage, President Biden’s Division of Training proposed on January 10, 2023, to fully redo the Revised Pay As You Earn (REPAYE) program to make it extra beneficiant for thousands and thousands of debtors. Two teams of debtors will see the largest advantages: low-income and high-income debtors.

The Modified REPAYE would change the principles to permit the next:

- A poverty line deduction of 225% as an alternative of 150%.

- Married debtors might file taxes individually to exclude a partner’s earnings.

- 5% of earnings for undergrad-only debtors. 10% of earnings for grad-only debtors, and a weighted common of these numbers when you have debt from each undergrad and grad faculty.

- Forgiveness after 20 years for undergrad debtors and 25 years for graduate debtors. Exception: in the event you owe lower than $12,000, it will occur after 10 years.

- Mum or dad PLUS debtors are excluded however might entry this new plan by means of the double consolidation loophole.

- Ultimately, you would swap to the brand new plan with out capitalizing your curiosity underneath new guidelines. In the event you’re already on REPAYE, you wouldn’t want to change.

We’ll look first at how the advantages of the Modified REPAYE plan would have an effect on lower-income households, after which we’ll have a look at the advantages that will likely be delivered to higher-income professionals with graduate levels.

Modified REPAYE would ship free group faculty

The typical group faculty pupil mortgage borrower graduates with about $13,000 of pupil debt.

The brand new modified REPAYE plan would give a shorter 10-year timeline to forgiveness for debtors with $12,000 or much less in pupil loans — that would come with most debtors at public group schools.

Based on the identical website I linked above, the common group faculty grad earns about $33,000 10 years after commencement.

The brand new REPAYE guidelines would enable a borrower incomes lower than $30,578 to pay $0 month-to-month with no curiosity accrual. In the event you earned above that quantity, you’d solely pay 5% of the marginal earnings above that stage.

Add in a partner or youngsters, and your deduction can be far increased. A household of 4 might earn over $62,000 earlier than paying something.

Underneath current REPAYE guidelines, a group faculty borrower would pay about $100 a month, which suggests forgiveness shouldn’t be actually an choice on a debt as small as $12,000.

Different advantages of the brand new IDR plan for low and middle-income debtors

Check out the current discretionary earnings definitions for IDR reimbursement plans and the way it compares to the brand new proposed guidelines.

Relying on your loved ones dimension, low and low-middle-income households might see their funds decreased 100% to $0 a month.

These modifications would have the best influence on households with numerous youngsters.

Whereas low-income households would see the largest proportion modifications in what they pay, higher-income households would see the largest greenback financial savings.

Modified REPAYE would additionally create nearly free faculty for many

Think about this case. You’re employed your manner as much as a place as a undertaking supervisor at a Fortune 500 firm and earn $100,000 a 12 months. Your partner earns $200,000 as a gross sales supervisor. Your mixed earnings is $300,000. Assume there are three youngsters, as nicely.

Underneath present IDR guidelines, there’s no manner a borrower on this state of affairs might obtain forgiveness on her pupil loans.

However underneath the brand new Biden REPAYE guidelines, she might.

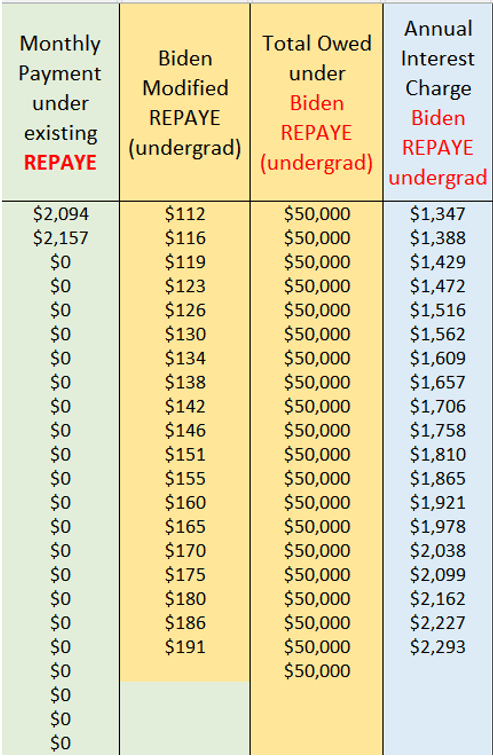

Faux the undertaking supervisor owes $50,000 from undergrad, and she or he recordsdata taxes married submitting individually.

Her fee underneath REPAYE falls from $2,094 a month to simply $112 a month. That’s a 95% lower in funds.

Her rate of interest “falls,” too. Her statutory fee is unchanged, however after the brand new curiosity subsidies from the New REPAYE are utilized, her curiosity can be within the 2% to 4% vary.

When you may put cash in Vanguard’s Federal Cash Market and earn over 4%, there can be no cause rationally to pay down this debt extra shortly.

What if this borrower contributed the utmost to her 401k? In that case, her fee would fall to $0 a month.

Underneath the New REPAYE plan, {couples} incomes $200,000, $300,000, and even $400,000 might qualify without spending a dime faculty.

Biden promised solely that public faculty can be free. However this plan goes far additional than that.

Mum or dad PLUS is excluded from new IDR, however there’s a loophole

One of many least recognized loopholes within the pupil mortgage drawback is one thing referred to as “double consolidation.”

Mum or dad PLUS loans can not entry any reimbursement plan apart from ICR.

That’s as a result of a consolidation mortgage that paid off Mum or dad PLUS can not entry different reimbursement plans by statute.

However a consolidation of a consolidation is underneath no such restriction.

Senior Pupil Mortgage Advisor Meagan McGuire, CSLP®, breaks it down in this text, however right here’s an instance:

So, fake you may have 4 loans. You’d consolidate them individually by sending two to at least one servicer and the opposite two to a distinct servicer. Look ahead to that consolidation to complete, then consolidate the 2 consolidation loans collectively.

The brand new consolidation mortgage can now entry REPAYE.

And if a retired couple has a excessive earnings, they may file individually and get a fee of virtually $0.

Underneath the brand new guidelines, a household that actually understood their choices might ship all of their youngsters to nearly any faculty within the nation without spending a dime.

How?

- Borrow as much as the utmost for Stafford loans within the little one’s title.

- Then, put limitless Mum or dad PLUS loans for as many youngsters as you may have within the title of 1 mum or dad.

- Consolidate twice after the final one graduates.

- And file taxes individually so you may pay nearly $0 month-to-month for 20 years, with no curiosity development, whereas the total steadiness is forgiven.

Recall the film Ladybird? Her father took out a mortgage to ship her to NYU.

Mortgages should be paid again in full.

As an alternative, he might have borrowed $200,000 underneath Mum or dad PLUS and used this loophole to entry New REPAYE and pay nearly nothing.

Professionals with graduate levels get large curiosity subsidies and far decrease funds usually

Up to now, debtors would wish to decide on between 20-year forgiveness with Pay As You Earn (PAYE) and 25-year forgiveness with REPAYE.

Moreover, married {couples} needed to file collectively with REPAYE. Solely underneath PAYE and IBR might married debtors exclude their partner’s earnings from their funds.

However this new IDR plan would enable debtors to file individually, get 25 years till forgiveness, and get all unpaid curiosity backed.

Underneath the previous REPAYE plan, the lack to file individually considerably restricted the curiosity subsidy for the highest-income {couples}.

No extra with New REPAYE.

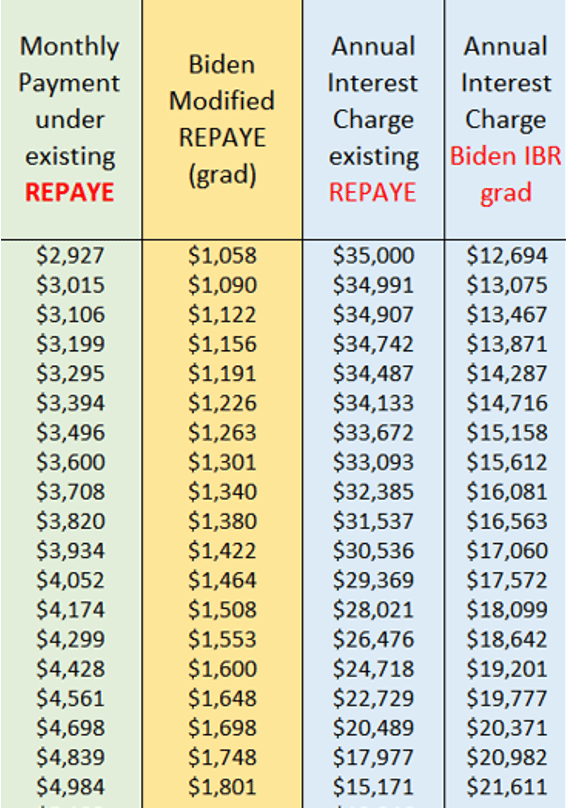

Think about the instance of two married dentists, every incomes $200,000 a 12 months, the place solely certainly one of them owes pupil debt. We’ll say he owes $500,000 at 7% curiosity, they’ve a few youngsters, they usually file taxes individually.

Notice the almost two-thirds discount in each their funds and curiosity. It’s really gorgeous.

Examples like this present why the White Home is mistaken when it says that debtors within the high 30% of earnings will solely see their funds fall 5%. They’re not considering married submitting individually.

New complexities for debtors with future excessive incomes: the PSLF conundrum

Underneath different proposed rule modifications to pupil loans, the Division of Training will enable debtors to depend financial hardship deferment in direction of PSLF.

Think about the case of a resident doctor.

Underneath the New REPAYE plan, she might pay about $0 a month for the primary two years and get a subsidy of 100% of her curiosity.

However in 12 months three, her fee would bounce to $230 a month if she was single.

If she was positive of going into non-public apply or uncertain of which path she would take after coaching, she ought to persist with the New REPAYE.

But when she was sure she can be taking a job at a not-for-profit, she would wish to swap to deferment in 12 months three to keep away from making funds on her loans whereas nonetheless getting PSLF credit score.

Such an motion would save her roughly $2,700 over two years, assuming a four-year residency.

And such an motion would enlarge the financial savings over longer coaching durations.

Would PAYE, Previous IBR, and New IBR have makes use of anymore?

Sure. Stunningly, the Division of Training is proposing to maintain the forgiveness timeline for grad college students underneath REPAYE at 25 years (see web page 72).

We nonetheless must see what the ultimate guidelines are, however presumably, the New REPAYE rule wouldn’t have a cap on funds just like the PAYE and IBR plans do.

So debtors needing a shorter reimbursement timeline and people needing a fee cap may benefit from the prevailing plans.

For a borrower with a really excessive earnings, this fee cap might enable somebody to qualify for PSLF who would in any other case not qualify.

In excessive earnings conditions, this fee cap could be useful for 20-year forgiveness too.

It’s unlikely that each one makes use of of those previous plans would go away, however the administration does need to maneuver most debtors to this new plan by sunsetting entry to the previous ones.

Modified REPAYE will result in an explosion of borrowing

The neatest motion a borrower might take after this new IDR plan turns into legislation can be to borrow each dime they presumably can.

Many group faculty graduates don’t tackle debt however might. The rational selection can be to maximise loans due to these new advantages.

For debtors in a conventional four-year faculty, the flexibility to file taxes individually sooner or later would encourage any pupil to borrow the max they qualify for since they may simply exclude their partner’s earnings sooner or later.

In truth, debtors who each have loans might double dip on the household dimension deduction. There’s not as a lot incentive to do this with a 150% poverty line deduction, however with 225%, much more financial savings alternatives can be found.

Graduate debtors will now have entry to a low or zero-interest line of credit score throughout their research. Whilst you’re theoretically not allowed to make use of pupil mortgage funds to take a position, cash is fungible, so there can be no enforcement mechanism to cease somebody from taking out a bunch of loans to pay lease and utilizing the cash they’d’ve used on lease to take a position.

With out capping pupil loans, the disaster will proceed.

The NY Fed has present in prior analysis that a rise in backed pupil mortgage limits will increase tuition by about 60 cents for every $1 restrict enhance.

This new REPAYE plan would successfully flip all graduate loans into digital backed loans. The one distinction is that the subsidy interval can be 20 to 25 years AFTER commencement as an alternative of the 4 years DURING research.

One would anticipate faculties to catch on and double or triple their tuition over the following decade if allowed.

What ought to debtors do subsequent?

We might nonetheless see authorized motion over this new REPAYE plan, so debtors ought to keep tuned.

Do not forget that many debtors don’t must recertify their IDR fee till as late as 2025.

Since many debtors have seen incomes go up considerably, it’s not a foregone conclusion that you’d swap to this plan as quickly as you’re in a position.

Debtors ought to look fastidiously at present fee obligations, how lengthy these would final, and when the correct time to change to New REPAYE can be. We can assist with that. And we’ll have extra for you because the New REPAYE guidelines proceed to develop.