{kind=link}

Now that the housing market is popping in favor of dwelling patrons, the phrase “vendor concessions” may develop into much more widespread.

Over the previous decade, dwelling sellers have had the higher hand, typically unloading their properties above checklist worth.

In lots of instances, dwelling patrons had been pressured to enter bidding wars, assuming they had been fortunate sufficient to get the chance.

However now that mortgage charges have doubled, and residential costs are on a downward trajectory, the state of affairs is sort of the other.

In the event you’re a potential dwelling purchaser, it’s essential know what vendor concessions are and the way they work.

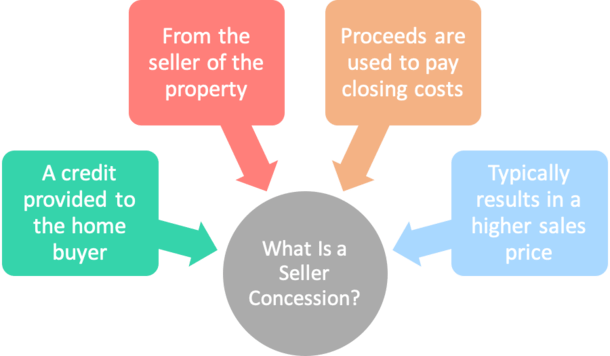

What Are Vendor Concessions?

A vendor concession is a monetary contribution from a house vendor that reduces a house purchaser’s closing prices.

One of many greatest hurdles potential dwelling patrons face, aside from DTI constraints, is having the mandatory funds (belongings) to shut on a house buy.

Vendor concessions reduce that burden, making it simpler to qualify for a house mortgage and purchase a property.

The funds are sometimes generated through a barely greater contract worth, which reduces the client’s out-of-pocket bills.

Nonetheless, this implies the borrower will wind up with a bigger mortgage quantity, and finance these prices over time through a better month-to-month mortgage fee.

For instance, if a purchaser gives $360,000 for a property with $10,000 in vendor concessions, the vendor could say, “Certain, it’s all yours for $370,000.”

You’re not likely getting cash at no cost because the buy worth rises by the quantity requested. However it does cut back the amount of money due at closing.

In a nutshell, it means you’re paying for that $10,000 through the upper gross sales worth over time as an alternative of at closing.

Remember that the property should then appraise for that greater quantity to ensure that the mortgage financing to work out.

And your down fee could change consequently, assuming you wish to hold your loan-to-value (LTV) ratio the identical.

Whereas they weren’t fashionable when the housing market was pink sizzling, vendor concessions have since develop into much more widespread as patrons acquire the higher hand.

In reality, a brand new report from Redfin discovered {that a} report 42% of dwelling gross sales within the fourth quarter of 2022 included concessions to the client.

What Can Vendor Concessions Be Used For?

The proceeds from vendor concessions can be utilized for quite a lot of prices related to the house buy.

This may embrace lender charges, third-party lending charges, taxes, insurance coverage, HOA dues, buydowns, repairs/enhancements, and rather more.

After all, in case your inspection finds that actual repairs are needed, these ought to cut back the gross sales worth or be taken from the vendor’s proceeds with out rising the gross sales worth.

Lender charges

Mortgage origination charges

Low cost factors

Title insurance coverage

Escrow charges

Appraisal charges

Lawyer/recording charges

Inspection charges

Property taxes

Switch taxes

Owners insurance coverage premiums

Mortgage insurance coverage premiums

Funding charges

Pay as you go objects for an impound account

Curiosity costs

HOA dues

Mortgage buydowns

What Can’t Vendor Concessions Be Used For?

Vendor concessions sometimes can’t be used for sure issues, such because the down fee. Nor can the client obtain money through the vendor’s contribution.

To that finish, the concessions you obtain can’t exceed your closings prices, so be certain you don’t ask for greater than you want.

In the event you do wind up with an extra, you possibly can discover paying mortgage low cost factors to decrease your mortgage fee. Or load up a mortgage impound account.

Moreover, concessions can’t be utilized to satisfy reserve necessities, or minimal borrower contribution necessities.

And the quantity of vendor concessions should be at/under the restrict set forth by the related mortgage kind used for financing.

Vendor Concession Limits by Mortgage Kind

Fannie Mae and Freddie Mac confer with vendor concessions as “ get together contributions,” or IPCs for brief.

Fannie Mae considers IPCs to be both financing concessions (extra widespread) or gross sales concessions (much less widespread).

As to what they take into account gross sales concessions, these “are IPCs that take the type of non-realty objects,” equivalent to money, furnishings, vehicles, shifting bills, together with financing concessions that exceed Fannie Mae limits.

The excellent news is lender credit should not thought of IPCs even when the mortgage lender is taken into account an get together.

So you will get lender credit to scale back your closing prices AND credit from the house vendor (through concessions) to scale back your outlay.

Each Fannie and Freddie again nearly all of dwelling loans that exist, identified collectively as conforming loans.

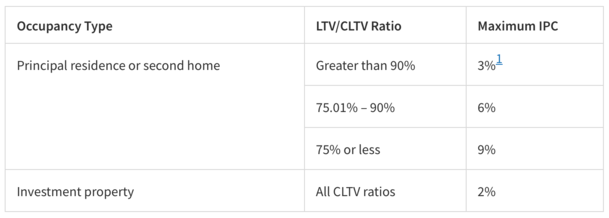

On conforming loans, vendor concessions are restricted to 2-9% of the gross sales worth, as seen within the desk under.

If the property is a main residence or second dwelling, the restrict ranges from 3-9% based mostly in your loan-to-value (LTV) ratio.

The larger the down fee, the extra you possibly can obtain in concessions. To calculate vendor concessions, merely multiply the proposed gross sales worth by the proportion allowed based mostly on the LTV.

Be aware that non-realty objects and IPCs in extra of the bounds are thought of “gross sales concessions,” and would require the property gross sales worth be diminished by the worth of such gross sales concessions when calculating the LTV ratio for underwriting/eligibility functions.

For funding properties, IPCs are capped at 2%, no matter LTV. So if the acquisition worth had been $300,000, you’d be capped at $6,000.

If it’s a HomePath property, the max IPC is 6% of the acquisition worth, even when above 90% LTV.

The utmost vendor concessions on an FHA mortgage is 6% of the lesser of the property’s gross sales worth or the appraised worth, no matter LTV. (part 4155.1 2.A.4.a)

The utmost vendor concessions on a USDA mortgage is 6% as effectively, although some say mortgage quantity and others say gross sales worth (supply)

Both method, most debtors who take out USDA loans put nothing down, so it’s probably moot.

The utmost vendor concessions on a VA mortgage is 4% of the appraised worth/gross sales worth (supply).

Nonetheless, “regular low cost factors and fee of the client’s closing prices” don’t should be included in that tough restrict. In different phrases, it is likely to be attainable to get greater than 4%.

Max vendor concessions on jumbo loans will differ as a result of they aren’t topic to 1 set of tips just like the mortgage varieties above. However there’s a very good likelihood the bounds will likely be comparable.

Make certain your actual property agent, mortgage officer (or mortgage dealer), and vendor are all conscious of those limits.

As to why there are vendor concession limits within the first place, it’s to make sure dwelling costs aren’t artificially inflated, and to make sure debtors are correctly certified.

Vendor Concession Instance

| Concession Quantity | $0 | $10,000 |

| Gross sales Worth | $360,000 | $370,000 |

| 20% Down Fee | $72,000 | $74,000 |

| Mortgage Quantity | $288,000 | $296,000 |

| Month-to-month Fee | $1,680.69 | $1,727.38 |

| Fee Distinction | +$46.69 | |

| Closing Prices | $15,000 | $15,000 |

| Out-of-Pocket Bills | $15,000 (plus down fee) | $5,000 (plus down fee) |

Let’s take a look at an instance of vendor concession in motion. Think about you discover a home you want and supply $360,000, however want $10,000 in closing value help.

The vendor says no drawback, we will promote for $370,000 and offer you a $10,000 credit score to cowl your prices.

You’re placing 20% down, so the down fee will increase $2,000 to account for the marginally greater gross sales worth.

The vendor concessions don’t change the rate of interest you qualify for, which is 5.75% in both state of affairs.

What does change, other than the down fee is the mortgage quantity, which will increase from $288,000 to $296,000.

Consequently, the month-to-month fee additionally rises from $1,680.69 to $1,727.38, a $46.69 distinction.

Certain, it’s almost $50, however you won’t discover it. You’ll definitely discover $10,000 much less in out-of-pocket bills at closing although.

And that additional money may turn out to be useful relating to making your first mortgage fee, or furnishing your new digs.

Vendor Concessions vs. Decrease Worth (or Worth Discount)

Now you is likely to be pondering, why not simply take a cheaper price as an alternative of the concessions. That method you’ll want a smaller down fee and also you’ll have a decrease mortgage fee too.

The issue, as evidenced within the instance above, is {that a} barely decrease gross sales worth does little to maneuver the needle.

An additional $50 a month is negligible for many dwelling patrons buying a near-$400,000 property.

However getting $10,000 to scale back your precise out-of-pocket bills is large. In spite of everything, most Individuals have little or no socked away in financial savings.

So having to surrender $10,000 on high of different dwelling shopping for associated bills may deplete your checking account.

As an alternative, you choose to pay a barely greater mortgage fee and hold your financial savings intact, hopefully.

It is a comparable argument to taking a lender credit score as an alternative of paying mortgage factors, as extra is saved in your pocket.

The one actual draw back to the concessions, aside from the upper fee, is a better tax foundation on the upper gross sales worth. However once more, it’s not going to be a serious distinction.

Are Vendor Concessions a Good Deal?

From the house purchaser’s perspective, vendor concessions can reduce the monetary burden at closing, however enhance the acquisition worth.

So it’s mainly a case of paying much less at this time, however extra sooner or later through a bigger mortgage quantity. Nonetheless, it may possibly hold issues inexpensive and extra liquid.

In spite of everything, you’ll probably want additional money available after shopping for a house to account for mortgage funds, shifting prices, new furnishings, and so forth.

If attainable, it is likely to be higher to ask for restore credit as an alternative, wherein case the acquisition worth doesn’t enhance consequently. For this reason a high quality dwelling inspection is so vital.

It may also be attainable to get the very best of each worlds in the event you supply a barely decrease supply and ask for concessions. This is likely to be a greater solution to negotiate vendor concessions.

Utilizing our instance above, you supply $350,000 with $10,000 in concessions, bringing the gross sales worth to the unique $360,000.

You get your $10k in closing value help with out the gross sales worth being inflated.

Be strategic and ensure your actual property agent will get it.

For the house vendor, providing concessions could also be a relative no-brainer if the acquisition worth is adjusted consequently, particularly in a down market.

You’re mainly increasing the pool of eligible patrons with out giving freely an excessive amount of in your finish.

After all, it may alter the actual property agent’s fee very barely based mostly on the distinction in gross sales worth.

But when the vendor concessions get you to the end line, they might be effectively price it. Not solely in additional simply discovering a keen/ready purchaser, but additionally one who has a better time qualifying for a mortgage.

Execs and Cons of Vendor Concessions

The Good

- Reduces out-of-pocket bills if money is tough to return by

- Is likely to be simpler to qualify for a house mortgage (asset-wise)

- Can hold you liquid after an costly dwelling buy

- Might solely bump up your month-to-month mortgage fee barely

- Permits for the acquisition of different objects after closing like furnishing, shifting, and many others.

- Can entice extra dwelling patrons (in the event you’re the house vendor)

The Perhaps Not

- Will probably enhance the gross sales worth of the property (by the quantity conceded)

- Your month-to-month mortgage fee will likely be greater (bigger mortgage quantity)

- Closing prices are paid over time as an alternative of upfront (elevated curiosity expense)

- Larger property taxes if gross sales worth is greater