{kind=link}

“Each enterprise will turn into a financial institution” has turn into a standard chorus amongst tech circles. If Apple is something to go by, it’s turning into much less of a prediction and extra of a truth.

A mixture of embedded finance and open banking are the cocktail for reaching this prophecy. As extra developments towards open information sharing diminish banks’ proprietary benefit and digital options are explored, it has turn into simpler and cheaper for any model to supply its personal monetary merchandise.

“This gorgeous distinctive mix of issues is altering available in the market proper now,” stated Brian Hanrahan, CEO of Nuapay. “You had embedded finance making regular steps for the final a number of years. What’s taking place now along side it’s instantaneous funds rails, after which you will have open banking on prime of that.”

“It’s a mixture of issues that didn’t exist earlier than and positively didn’t coexist. So I feel the suppliers of those options have the potential to scale. Nonetheless, I feel for a lot of different companies with that client contact level, it should permit them to maximise their income and their features from the shift as effectively.”

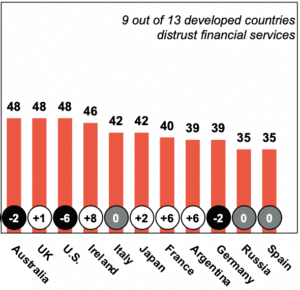

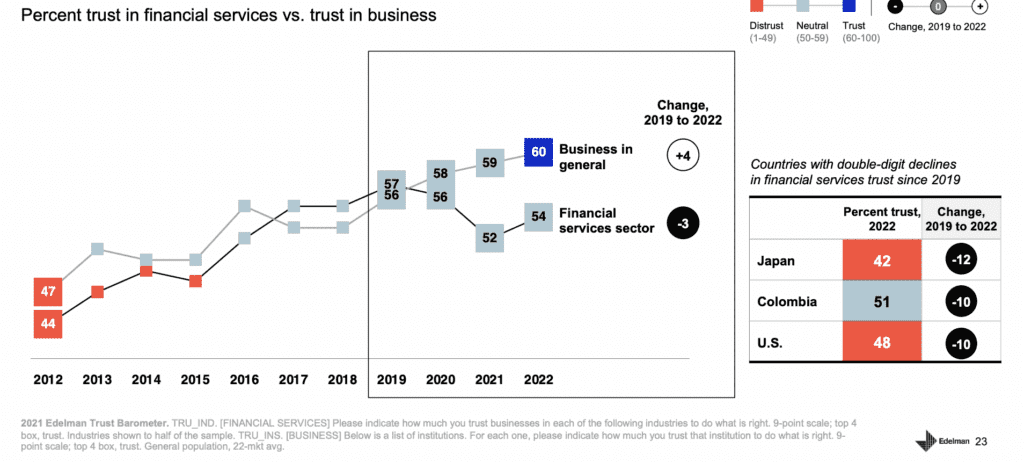

Belief in monetary establishments dropping

Banks themselves have undergone a disaster of confidence over the previous month. The delicate material of belief that was nonetheless being constructed up since 2008 has been disrupted, as soon as once more, by a spherical of financial institution closures.

In Edleman’s most up-to-date survey, it was discovered that belief was at an all-time low. Monetary companies fared as one of many worst, dropping ten proportion factors within the US, becoming a member of a lot of Europe in rallying mistrust. Digital funds have been the one subsector that resisted this pattern.

Youthful generations place much more doubt on monetary establishments. The World Financial Discussion board discovered that solely 28% of GenZ and Millenials trusted their banks to be honest and trustworthy about their merchandise.

Then again, belief in companies has elevated, which may lay fertile soil for manufacturers trying to incorporate monetary companies of their product stack. Shoppers looking for reliable monetary merchandise could also be extra inclined to observe their most popular manufacturers’ lead loyally.

The perpetual ‘yr for embedded finance’

Embedded finance drives the cost towards the courageous new world, making it more and more simpler for non-finance corporations to combine monetary merchandise into their providing.

Whereas it isn’t a brand new idea, digitization has supercharged the sector, opening out a scope of alternative that may be customized to fulfill client wants.

“If you consider embedded finance, like in a pre-digital period, you will have use instances, like folks going right into a automotive dealership and being provided a mortgage by the automotive dealership,” stated Hanrahan. “You’re transferring the service or the product to the purpose of want.”

“It’s a delicate distinction, however it’s actually vital. It’s an enormous distinction when it comes to the worth out of the vendor, the chance of the sale, the affiliation, and rising the order worth. So the dynamic adjustments totally once you transfer one thing to the bodily level of want.”

“Now all that’s taking place is digitalization,” he continued. “APIs and cellular banking permit us to try this in additional compelling methods.”

Open Banking boosts improvement

Open banking is the most recent piece, including to the scope for elevated embedded finance.

Banks’ long-standing benefit of retaining entry to buyer info has now been disrupted. With the UK main the best way, jurisdictions worldwide are adopting their very own approaches to open banking. The shift may instantly affect embedded finance.

“You possibly can tailor merchandise and provides to folks way more successfully when you’ve got higher information on them,” stated Hanrahan. “With open banking, the paradigm adjustments much more from being locked right into a proprietary stack.”

“You may supply an ideal account however should supply it on a selected financial institution’s license. Whereas with open banking, you’ll be able to decouple the layers of the worth chain. Shoppers can now get an ideal app, which then plugs into any of the banks that they occur to wish to depart their cash with.”

He defined it had allowed various cost strategies to be built-in into the product, corresponding to direct fund transfers, permitting prospects to bypass card funds if required.

As well as, the convergence of the 2 applied sciences permits companies to concentrate on creating monetary merchandise particular to their enterprise and buyer base.

“It’s fairly a compelling factor for lots of corporations to get entangled with as a result of the monetary companies sector is likely one of the largest industries on the earth. Folks collaborating in it could usually at the very least differentiate themselves or possibly even massively enhance their revenues.”

Firms’ engagement with their prospects can even lengthen to their monetary well being. Hanrahan defined {that a} aspect impact of the shift has allowed corporations to view their prospects’ affordability, permitting them to be extra accountable in accepting petitions for loans.

Within the UK, with new Buyer Obligation legal guidelines coming into impact this yr, it will permit companies to retain compliance and assist belief that the corporate is working in shoppers’ finest curiosity.

“It’s a fairly thrilling time when it comes to what’s doable,” stated Hanrahan.

RELATED: Why licensing issues: how banking licenses affect embedded finance