{kind=link}

FICO Scoring Fashions is the most typical time period amongst credit score customers. There’s hardly a credit score person who finds it new terminology. That’s FICO’s impression on the credit score world. However, do you know that FICO is just not the one one? Sure, there are a complete lot of scoring fashions within the credit score {industry}. This text will take you thru the dominance FICO rating has over different such scoring fashions, and temporary you extra about its newest variations.

FICO Scoring Fashions – The Extensively Used One

FICO (Truthful Isaac Company) is the earliest credit score rating group that launched a correct framework for evaluating customers’ creditworthiness. Later, many new credit score scoring fashions, like Vantage fashions, sprouted. However nonetheless, FICO has set its personal stage amongst credit score customers and credit score issuers. An evaluation says that greater than 90% of bank card issuers, lenders, and different monetary firms favor FICO scoring fashions over others.

If you’re a credit score person, or a credit score lender making an attempt to determine your borrower’s credit score rating, you possibly can depend on FICO scoring fashions. FICO’s scoring mannequin has designed a set of standards for credit score analysis. Additionally they hold updating their scoring mannequin to remain in tune with the present development.

How Lenders Use FICO Scores

Mortgage lenders don’t approve loans for everyone who applies for one, or a bank card. They analyze your potential to repay the mortgage. They don’t favor their capital to change into a charged-off debt. To make sure your capability, they anticipate a convincing level that demonstrates how succesful you might be.

That is the place they arrive to credit score scores. They depend on the 3-digit credit score rating of candidates that claims their repaying potential. They search assist from three main credit score bureaus Equifax, Experian, and TransUnion, who principally use the FICO scoring fashions to judge your credit score scores.

Contemplate, if you’re making use of for a house mortgage in ABC funds. The lender ought to now flip extra serious about understanding your credit score habits. At this level, after they can’t spend their entire time analyzing your efficiency, they merely get assist from any credit score reporting company that makes use of the FICO scoring sample.

How People Use FICO Scores

It’s not simply lenders who search for candidates’ credit score scores. Any citizen who’s eager on sustaining disciplined monetary conduct would possibly take a look at their credit score scores. Steadily checking your credit score reviews may help you are taking wanted actions to enhance your credit score scores.

Each particular person can test their credit score rating annually freed from cost. Annualcreditreport.com provides you a whole report of your credit score behaviors in current instances. This would possibly push you to change into extra accountable along with your funds and warn you about your current credit score rating vary. In the event you had been in a dangerous zone, like a poor credit score rating vary, you would possibly work on enhancing your scores.

How Is It Calculated?

By intently analyzing your credit score habits prior to now, credit score lenders decide your accountability and capability in repaying this mortgage. To help the lenders with this course of, FICO has curated an inventory of standards that may clearly point out an applicant’s credit score habits.

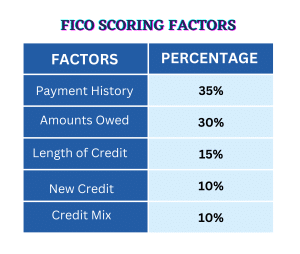

5 Main Elements

The first components used to find out credit score scores are listed beneath.

FICO Scoring Elements

Fee Historical past – This issue holds a big portion of the credit score rating calculation. This analyzes how common the customers are of their month-to-month dues. 35% of your credit score rating relies on this issue. Being on time in cost historical past positively impacts your credit score rating.

Credit score Utilization Ratio – This considers the present credit score steadiness to start out new credit score. If the out there credit score steadiness is excessive, the possibilities of credit score approval are additionally excessive. As this issue holds 30% significance in your credit score rating, at all times be sure to didn’t use most of your credit score from the out there credit score you may have.

Size of Credit score – The size of the credit score can be thought-about when calculating credit score scores. That is additionally immediately proportional to the credit score rating. This has an excellent impression on the credit score rating and holds 15% of the general credit score rating.

New Credit score Accounts – It’s not advisable to have too many credit score accounts. You possibly can at all times get one whether it is mandatory, however be sure that it’s mandatory and manageable along with your out there steadiness and potential.

Credit score Combine – The sorts of credit are additionally measured throughout a credit score calculation. This doesn’t imply you need to preserve quite a lot of credit for certain. However having completely different credit score accounts has a ten% impression in your credit score rating.

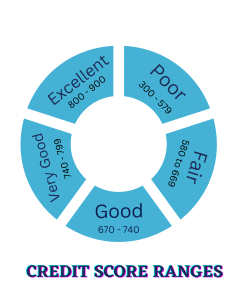

Credit score Rating Ranges

The calculated three-digit FICO scores that vary from 300 to 900 is categorized into 5 completely different ranges. This categorization is devised in a manner that the upper the credit score rating, the upper the creditworthiness.

FICO Scoring Ranges – 5 Ranges

- Poor – Scores between 300 to 579.

- Truthful – Scores between 589 to 669.

- Good – Scores between 670 to 740.

- Very Good – Scores between 740 to 799.

- Excellent – Scores between 800 to 900.

Variations of FICO Scores

FICO Scoring Fashions has launched many variations proper from the day it got here into existence to now. One of the best factor about FICO Scoring Fashions is that it’s designed in a technique to undertake modifications and hold enhancing them then and there. Listed below are a couple of extensively used variations of the FICO scoring fashions.

FICO 8 – The Most Frequent

FICO 8 is essentially the most generally used model of all FICO scores that had been launched in 2009. Although the credit score {industry} has witnessed two extra FICO variations. Nonetheless, model FICO 8 is ruling the credit score world. This model collects information from three credit score bureaus and focuses extra on credit score utilization ratio and cost historical past. That’s, if you’re making use of for credit score, your out there credit score steadiness is the first criterion. Contemplating the used-up credit score and the remaining steadiness, the credit score lenders calculate your creditworthiness.

FICO 9 – Added Benefit

FICO 9 inherits all of the options of the sooner variations, and values credit score utilization price and former historical past, like FICO 8. The add-on characteristic in FICO 9 is, it has a special method with regards to assortment accounts, particularly medical collections. That’s, when you have any medical or hospital assortment in your credit score, like surgical procedure collections, it won’t have an effect on your credit score scores the way in which different collections do. Although this was launched in 2016 and has a couple of benefits over the older variations, that is nonetheless not extensively thought-about as FICO 8.

FICO 10 and FICO 10T – Specialised in Trended Knowledge

This FICO Rating 10 Suite was launched lately in 2020 with an up to date characteristic of trended information. This current replace had change into the discuss of the city throughout its launch. Credit score customers had been barely panicked, because it was anticipated that their credit score scores would possibly drop by 20 factors. That is the most recent FICO scoring model that specialised in conventional and trended information. Along with the present standards, this FICO Rating 10 Suite extremely regards the final one-year credit score historical past of the people.

Credit score Rating vs. FICO Rating

Many have a tendency to make use of the phrases FICO rating and credit score rating interchangeably. Although there are extremely related, there’s a seen distinction for certain. Sure. All FICO scores are credit score scores. However not all credit score scores are FICO scores. The FICO rating is a sub-set of a credit score rating. A FICO rating is the title of an evaluating mannequin the place the credit score rating refers to all of the scores whatever the scoring fashions. Undergo this weblog on FICO Vs. Credit score Rating to know how they differ from one another.

Different Credit score Scoring Fashions

Other than the popularly identified credit score scores, just like the FICO rating there are different credit score scores, like Vantage Scores, TransRisk, CE Credit score Scores, and Credit score Skilled Credit score Scores.

The FICO Scoring Fashions – FICO holds an extended historical past within the area of interest, because it was the primary of its form. This was devised by Mathematician Earl Isaac and Engineer Invoice Truthful in 1958 to find out creditworthiness and make enterprise selections. That is efficiently standing as essentially the most most well-liked scoring mannequin of all.

The Vantage Scoring Fashions – Three main credit score bureaus Equifax, Experian, and TransUnion got here up with a standard scoring sample known as Vantage Rating variations. This scoring mannequin was launched in 2006 and managed to face because the second most well-liked credit score rating amongst credit score bureaus, lenders, and customers.

TransRisk – This TransRisk rating was launched by the favored credit score bureau TransUnion. This scoring mannequin is sort of completely different from others. TarnsRisk extremely focuses on analyzing the applicant’s credit score. When different rating variations discuss concerning the historical past of a person’s present credit score accounts, TransRisk says the doable threat of availing of a brand new credit score account.

Business-Particular Scores by FICO Rating

Out of a number of FICO rating variations, the industry-specific FICO rating works uniquely for every {industry}. Along with the fundamental standards, it additionally considers data that’s extra particular to the {industry}. In, every sort of credit score utility, they’ve a related scoring mannequin. Say, like mortgage lending FICO scores for residence loans, FICO auto scores for car loans, and FICO private scores for private loans. Additionally they have bank card FICO scores and FICO bankcard scores for bank cards.

Steadily Requested Questions

1. Which is the most recent FICO scoring model among the many FICO scoring fashions?

The newest model of the FICO scoring mannequin is the FICO rating 10 suite. This mannequin has been in existence since 2020 and has put many credit score customers liable to shedding their credit score scores. However, this was simply designed to reinforce the standard of lenders’ selections when it comes to credit score approvals.

2. Can I get a mortgage with a low FICO rating?

A FICO rating is the essential factor in your mortgage approval. However, it doesn’t imply that you’ll by no means safe a mortgage if you happen to aren’t in a greater credit score rating class. There are a couple of mortgage distributors and different mortgage choices which are much less dependent in your credit score rating. However nonetheless, having an excellent credit score rating is an natural manner of qualifying for a mortgage with none dangers.

3. What’s the distinction between the FICO rating and the credit score rating?

Many would most likely mistake FICO scores and credit score scores for being the identical factor. The precise factor is that they’re fairly shut when it comes to context, however not precisely the identical. FICO scores specify a scoring mannequin, the place credit score scores usually consult with all fashions of credit score scores.

Associated Reads

Closing Ideas

After this detailed understanding of FICO scores, it’s clear that each credit score person should preserve an excellent FICO rating. Sure, your credit score lenders are primarily searching for FICO scores to estimate your potential to pay again their mortgage on time. On this case, you need to consider a number of methods to safe an honest place on the credit score scale.

To maintain you extra relaxed, credit score restore companies, like TheCreditPros will give you end-to-end help by frequently analyzing your credit score reviews, and taking all mandatory steps to enhance your credit score scores.