{kind=link}

Debt forgiveness happens when a lender forgives both a portion of or your entire debt owed by a borrower from a mortgage or credit score account.

Debt forgiveness happens when a portion of a mortgage or your entire remaining quantity of a mortgage or credit score line is canceled, relieving the borrower from the duty of compensation. Earlier than shifting ahead with debt forgiveness, it’s vital to think about the potential advantages and downsides so that you simply’re totally ready.

It’s additionally vital to notice that debt forgiveness differs from debt aid, which entails reorganizing debt to facilitate compensation—however doesn’t cancel the debt.

Proceed studying to study extra about debt forgiveness and discover totally different choices that you could be qualify for.

Debt forgiveness advantages

Debt forgiveness can present aid to those that are struggling to make funds, and it has the next advantages:

- You’ll be able to keep away from submitting for chapter: Debt forgiveness can stop the necessity to file for chapter, which might severely injury your credit score for as much as seven to 10 years.

- You’ll be able to pay lower than your authentic obligation: Whereas the quantity you’ll pay varies relying on this system you select, it’s usually a lot lower than the quantity you initially owed.

- You’ll be able to pay your money owed faster: Via debt forgiveness, you may considerably cut back your debt in a a lot shorter time-frame than you initially anticipated.

Debt forgiveness drawbacks

Then again, debt forgiveness has the next downsides that you need to be conscious of:

- You might owe taxes on the quantity that’s forgiven: Typically, canceled debt is taken into account taxable earnings that you could be be accountable to cowl.

- You possibly can owe greater than your authentic obligation: Many debt aid corporations cost extreme charges that might equal or exceed the quantity you initially owed. Moreover, it’s vital to vary your monetary habits so that you don’t proceed to rack up debt.

- Your credit score might take successful: Relying on the kind of debt that’s forgiven, you would discover a unfavourable impact in your credit score. Nonetheless, this may probably not be the case if the debt in query is pupil loans or medical payments.

Due to these drawbacks, you might wish to take into account different debt administration choices.

Debt forgiveness vs. debt consolidation

An alternative choice to debt forgiveness that you could be wish to take into account is debt consolidation. Whereas this technique doesn’t cancel the debt, it may well show you how to pay it off quicker and accrue fewer curiosity expenses.

One of the vital frequent debt consolidation strategies is a steadiness switch, which entails shifting debt to a brand new bank card that provides 0% APR for a number of months. Throughout this time, you may work to repay your debt with out racking up curiosity.

Different choices embrace taking out a private mortgage or residence fairness mortgage to repay your debt. The technique right here is that your new mortgage would have a decrease price than that of your present debt, permitting you to avoid wasting on curiosity

Simply be cautious of for-profit corporations that promise debt aid by way of consolidation, as they’re usually dear. As an alternative, look to nonprofits such because the Nationwide Basis for Credit score Counseling.

get debt forgiveness

When you’re shifting ahead with debt forgiveness, you’ve got a number of choices relying on mortgage sort and your total private and monetary state of affairs.

Federal packages

One of many few methods to get true debt forgiveness with out penalties is to see when you’re eligible for a particular program. Sometimes, these are solely supplied for pupil mortgage debt and residential mortgages:

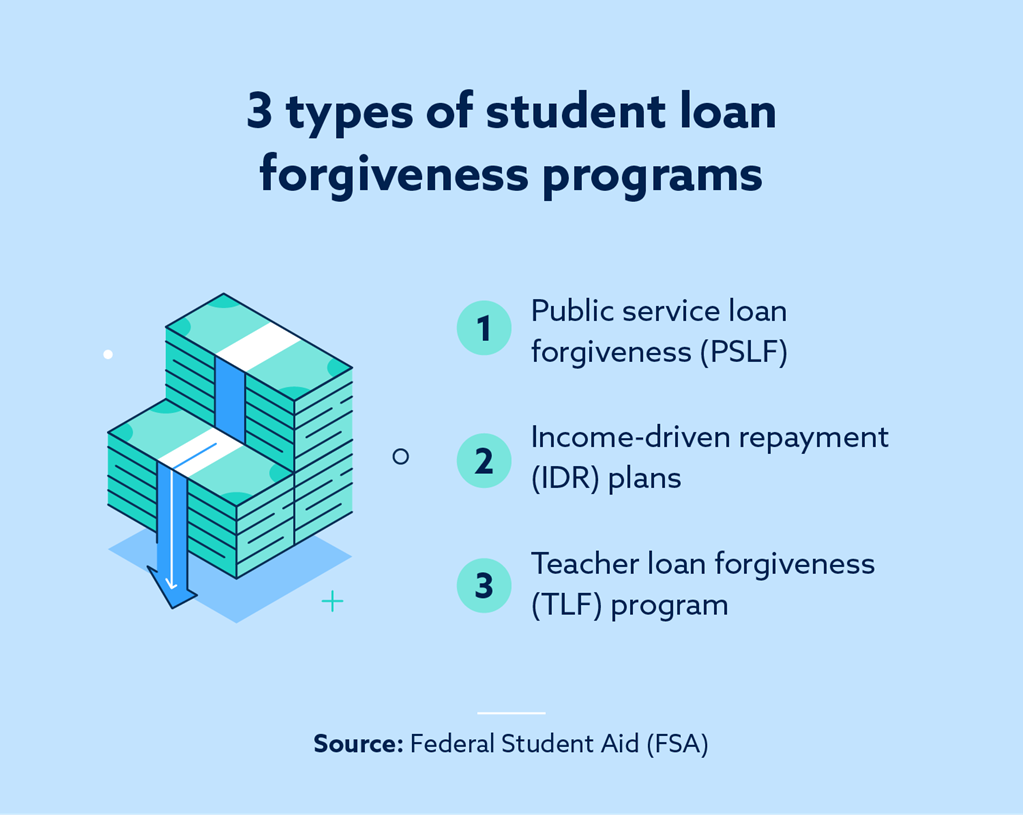

- Scholar mortgage forgiveness: In mid-2023, pupil loans totaled $1.7 trillion. To assist alleviate this, the Public Service Mortgage Forgiveness (PSLF) program gives Direct Mortgage forgiveness for full-time employees of U.S.-based or non-profit organizations who’ve made 120 certified month-to-month funds. One other sort of pupil mortgage forgiveness is income-driven compensation plans, which forgive the remaining mortgage steadiness on the finish of a compensation interval. Thirdly, when you’re a trainer, you might be eligible for a Trainer Mortgage Forgiveness program.

- Mortgage debt forgiveness: The Mortgage Forgiveness and Debt Reduction Act, enacted in 2007, lets eligible debtors exclude as much as two million {dollars} in forgiven mortgage debt from their taxable earnings. This permits forgiven mortgage debt and foreclosures balances to be really penalty-free.

You might be eligible for different federal packages to assist handle debt. To discover your choices additional, the Federal Commerce Fee has tips for getting out of debt.

Settlement

Settlement is by far the commonest type of debt forgiveness. It’s the method of negotiating your debt to solely repay a portion of your excellent steadiness. The remaining is forgiven, that means compensation is just not obligatory.

Debtors have a tendency to decide on debt settlement if they’ll’t afford costly and chronic debt funds. They could additionally select this route as a substitute for declaring chapter, since debt settlement ought to solely keep in your credit score report for seven years.

Nonetheless, it’s vital to be careful for hefty charges from these corporations. If hiring a debt settlement agent is past your means, take into account that negotiating by yourself is an choice. First, you’ll want to find out your excellent steadiness and what month-to-month cost you may afford. Subsequent, contact your creditor. You’ll want to elucidate why you may now not afford the mortgage after which negotiate a lump sum. In the event that they agree, ask for a written letter so you’ve got authorized proof of the settlement.

Statute of limitations

When you’re in search of debt forgiveness for bank card debt, you could possibly leverage the statute of limitations (SOL) in your state. The SOL is relevant as soon as a sure period of time has handed (usually three to fifteen years relying on what state you reside in) and your debt collector hasn’t pursued debt assortment in court docket. After this time-frame, they haven’t any authorized declare to your cash, and they need to now not be capable of efficiently sue you to gather the debt. Nonetheless, this method is dangerous for various causes.

SOL begin to accrue after the date of final exercise, which incorporates funds and expenses. After your SOL expires, a lawsuit can nonetheless be filed towards you—however you need to use the SOL as a protection in court docket.

Chapter

Submitting for chapter is an choice and that call will stay in your credit score report from seven to 10 years. That stated, it might assist forgive a few of your debt.

When you file for Chapter 7 chapter, your debt is forgiven and a few of your belongings stay with you topic to sure state and federal exemptions.

When you file for Chapter 13 chapter, you’re nonetheless required to repay your money owed. Nonetheless, the court docket will assign you a cost plan spanning wherever from three to 5 years, and so they might cut back your excellent steadiness to minimize the monetary burden.

What are the implications of debt forgiveness?

After you’ve got a portion of your debt forgiven, you might really feel such as you’re out of the woods—and for essentially the most half, that’s true. Nonetheless, there are a number of circumstances you’ll want to pay attention to so that you simply’re ready for the consequences debt forgiveness might have in your funds.

Taxes

Regardless of which debt forgiveness route you’re taking (except for chapter), you’ll probably find yourself with the next taxable earnings. If the quantity of forgiven debt exceeds $600, you’ll obtain a 1099-C type titled “Cancellation of Debt” from the creditor.

With this kind, you report the quantity of your forgiven debt to the IRS and pay earnings tax on it. Once you first take out a mortgage or borrow cash, you’re not charged taxes on it as a result of there’s the idea that you simply’ll pay it again. However after debt forgiveness, that assumption now not applies, which is why this basically “free cash” is now thought-about taxable earnings.

The upside is that the earnings tax you owe on the forgiven debt quantity is lower than what you would need to pay when you nonetheless owed the debt. Ensure to plan for this expense in order that it doesn’t shock you, particularly if the forgiven quantity is sizable.

Contemplate contacting a professional tax skilled for assist precisely submitting your taxes. Then, when you correctly report your debt forgiveness to the IRS, you’ll wish to test your credit score report.

Credit score rating

The unlucky actuality is that debt forgiveness might negatively have an effect on your credit score rating. After all, there is no such thing as a strategy to say for certain. What is going to enhance is your debt to earnings ratio. The impact to which debt forgiveness impacts your credit score largely will depend on the way you select to hunt debt forgiveness.

Chapter might be essentially the most devastating choice to your credit score rating. In line with Debt.org, a FICO rating of 780 might take a 240-point dip, and a rating of 680 might take successful of 130 – 150 factors. In case your credit score rating is way decrease than 680, you might not see as giant of a dip. Nonetheless, in case you have no late funds or cost off in your credit score report previous to submitting chapter, your rating dip is much much less.

Debt forgiveness gives a much-needed resolution for debtors struggling to make funds. Nonetheless, it additionally comes with circumstances. When contemplating which debt administration plan is best for you, slightly cautious planning can go a great distance.

If overwhelming debt has induced your credit score to dip under the place you’d prefer it to be, see if we might assist. We will check out your credit score report and help you with shifting ahead.

Word: Articles have solely been reviewed by the indicated lawyer, not written by them. The knowledge offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for common informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained inside the website don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.