{kind=link}

The data supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

The debt snowball methodology is a reimbursement plan that entails paying off money owed so as of lowest to highest principal sums. As you repay small loans, you acquire the boldness and cash wanted to repay bigger ones.

Paying a number of money owed is a juggling act. On one hand, paying all money owed without delay is tempting however costly. However, paying separately is extra inexpensive, however that takes long-term monetary administration. Fortunately, you should use the debt snowball methodology to simplify your debt payoff plan..

The debt snowball methodology is a debt reimbursement plan wherein you rapidly repay small money owed to concentrate on bigger ones. Regardless that it’s easy in idea, you could have questions concerning the execution. That can assist you out, we’ll clarify the strategy intimately, stroll you thru its steps and share a number of greatest practices.

Desk of contents:

- What’s the debt snowball methodology?

- The best way to snowball debt in 4 steps

- Snowball methodology instance

- Finest practices for the snowball methodology of paying off debt

- The snowball methodology vs. avalanche methodology of debt consolidation

- Repay debt and enhance your credit score with Lexington Legislation Agency

What’s the debt snowball methodology?

The snowball methodology is a debt reimbursement strategy the place you repay money owed so as of smallest to largest principal sums. After making the minimal fee on all money owed, spenders make investments all they’ll into money owed with the smallest principal. When you repay these small money owed, you’ll be able to roll funds over to the following highest.

In contrast to different debt consolidation and payoff methods, the snowball methodology doesn’t think about rates of interest. As an alternative, this strategy focuses on principal funds. With every debt repaid, it is best to really feel higher outfitted to sort out the following in line.

Who ought to use the snowball methodology?

Anybody juggling a number of money owed ought to think about the snowball methodology. It gives a easy technique for organizing your money owed. As you knock out small money owed, the snowball impact presents the momentum and confidence that you must get out of debt.

Professionals of the snowball methodology

The snowball methodology of debt reimbursement presents distinct advantages over different approaches. The primary benefits embody:

- Actionability: Small adjustments to your budgeting make this strategy actionable. It doesn’t include any prerequisite or extra prices. In consequence, leaping in is quick and simple.

- Empowerment: In case you can’t pay your payments or sustain with debt, the snowball methodology mentally and financially empowers you. With each small debt cleared, you see progress and keep motivated as you repay better money owed.

- Simplicity: The snowball methodology is straightforward to wrap your head round. It additionally breaks massive chunks of debt into smaller, approachable items.

Cons of the snowball methodology

Regardless of its strengths, the snowball methodology comes with a number of downsides, together with:

- Curiosity accrual: In case your bigger loans have the next rate of interest, the snowball methodology could not work as nicely. In accordance with these credit score details, if you happen to observe the technique, greater rates of interest could price you extra over time.

- Emphasis on small money owed: This strategy works greatest when knocking out small money owed again to again. You received’t see the identical fast outcomes if you happen to’re juggling a number of massive loans.

- Inflexibility: The snowball methodology doesn’t depart a lot room for personalisation. Chances are you’ll wish to think about an alternative choice if you would like a malleable technique you’ll be able to modify.

The best way to snowball debt in 4 steps

Because of its simplicity, you’ll be able to implement the snowball methodology in solely 4 steps. That is the method intimately:

Step 1: Take a debt stock

Step one of the debt snowball methodology is to record all of your money owed from smallest to largest. Whilst you can preserve curiosity in thoughts, concentrate on the principal steadiness. If two money owed share the same principal, you’ll be able to place the one with the next rate of interest first.

Step 2: Make minimal funds on all money owed

Make the minimal fee on every of your money owed each month. This step is essential since you don’t wish to incur any charges or penalties for not making funds on different money owed whilst you concentrate on one particularly.

Step 3: Pay down your smallest debt

On prime of the minimal fee, make investments as a lot as you’ll be able to into your lowest principal steadiness. Whilst you wish to pay it off rapidly, don’t overlook to set cash apart for:

- Financial savings

- Groceries, laundry and different family prices

- Day-to-day bills like consuming out or investing in your hobbies

Step 4: Repeat till debt-free

As you repay every debt, you’ll be able to roll more cash into bigger ones. While you aren’t juggling as many money owed, you’ll have the sources to concentrate on paying down the very best sums. Finally, most or all your money owed ought to receives a commission off.

Snowball methodology instance

To assist clarify the snowball methodology, right here is an instance of the way you funds for it. Assume you make $2,500 a month and need to handle these bills:

- Lease: $700/month

- Utilities: $150/month

- Scholar debt: Minimal fee of $120/month (whole principal: $21,000)

- Medical debt: Minimal fee of $60/month (whole principal: $4,500)

- Auto debt: Minimal fee of $40/month (whole principal: $1,800)

- Bank card debt: Minimal fee of $15/month (whole principal: $900)

You’ll implement the snowball methodology of paying off debt like this:

- Pay essential bills like lease and utilities. This brings you all the way down to $1,650.

- Pay the minimal steadiness on all money owed. Your spending cash drops to $1,415.

- Pay down your lowest debt. On this case, it’s the bank card debt. Let’s say you pay $500 and produce that principal all the way down to $400. Your remaining steadiness comes out to $915.

- Spend the rest of your cash on day-to-day bills. Bear in mind to avoid wasting as a lot as you’ll be able to. It by no means hurts to have an emergency fund prepared.

- When you repay the bank card debt, transfer on to the following lowest principal sum. So, you’d repay auto, medical and scholar loans in that order.

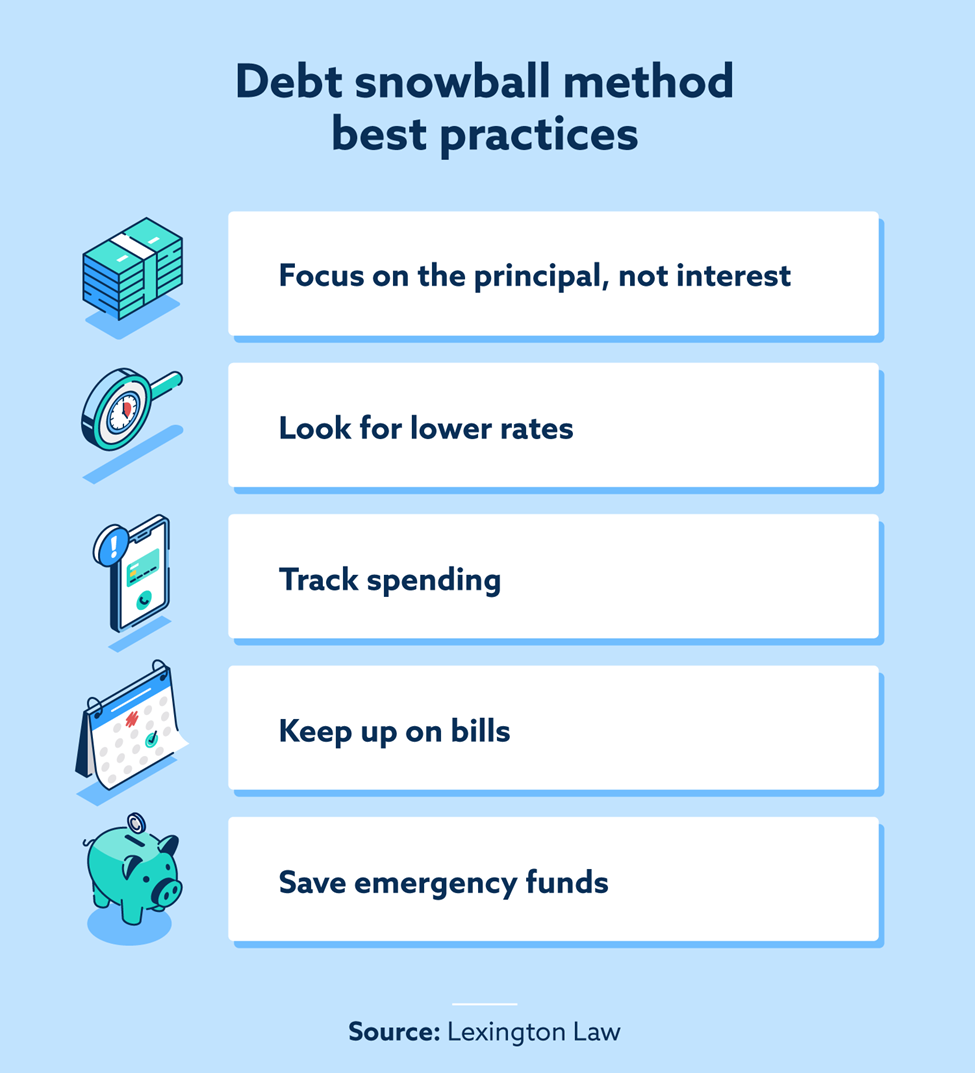

Finest practices for the snowball methodology of paying off debt

To see the very best returns on the snowball methodology, observe the following tips:

- Don’t base reimbursement order on curiosity: Anybody attempting the snowball methodology ought to concentrate on principal balances. This strategy depends on small wins to construct as much as larger money owed. Massive, high-interest loans get in the best way of that.

- Mitigate excessive curiosity with decrease charges: Whereas specializing in small loans, attempt to cut back curiosity on bigger ones. Negotiating a decrease rate of interest will assist lower your expenses in the long term.

- Monitor spending over time: You must keep away from losing cash that would go towards paying off debt. Moreover, observe the quantity you spend on debt reimbursement. That manner, you’ll be able to keep on observe as weeks or months go.

- Don’t fall behind on payments: Falling behind on payments or loans can result in charges or the next rate of interest. In the long term, this can decelerate your reimbursement.

- Put aside emergency funds: You shouldn’t make investments each cent in settling your money owed. An emergency fund will help you keep away from extra money owed after house repairs or well being points.

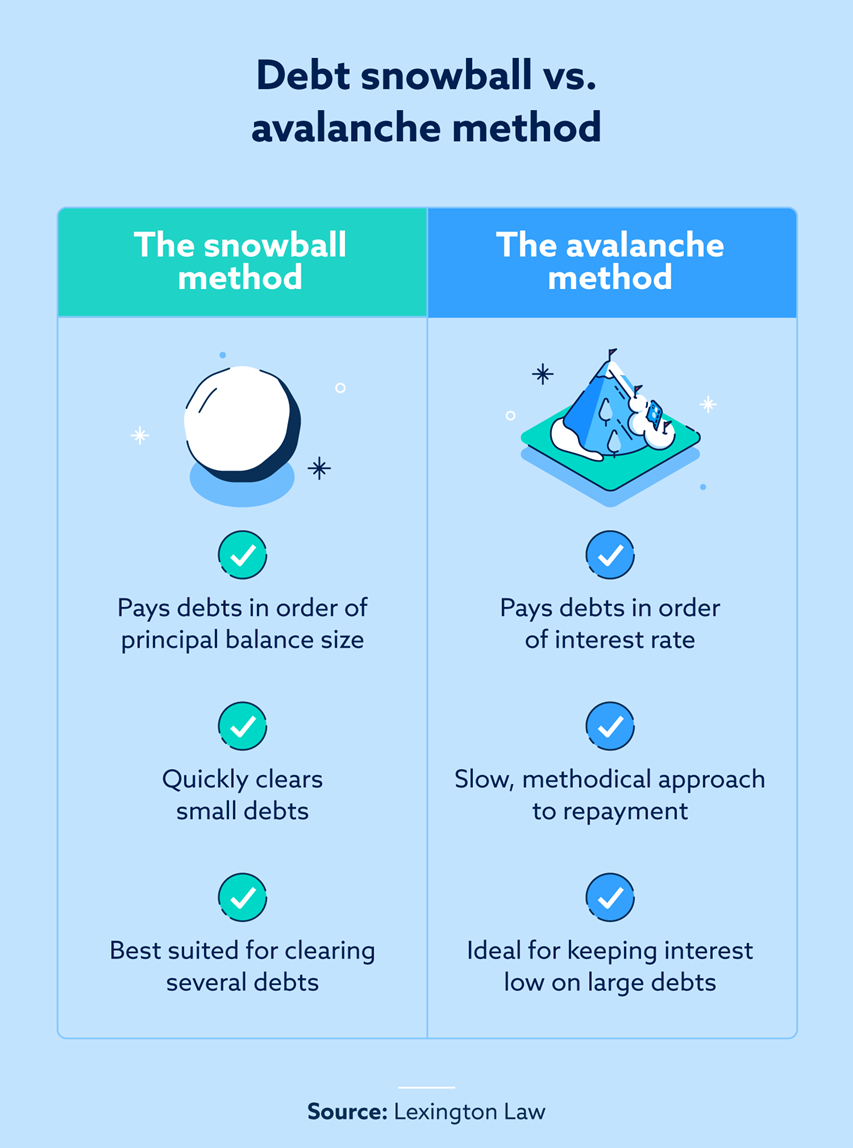

The snowball vs. avalanche methodology

The avalanche methodology is one other manner of paying off debt that determines fee order by rate of interest. In each the avalanche and snowball approaches, you make minimal funds on all debt every month. From right here, they diverge:

- The avalanche methodology has spenders repay the debt with the highest rate of interest first. As soon as prospects repay this mortgage, they transfer to the one with the following highest rate of interest.

- The snowball methodology ignores rates of interest to concentrate on principal funds.

Whereas the snowball methodology rapidly pays off small money owed, the avalanche strategy is sluggish and regular. It might take you longer to repay your money owed, however you’ll accrue much less curiosity. So, relying in your rate of interest and principal sum, you might pay much less total, which may make this feature extra interesting.

Which methodology is best for you?

The avalanche and snowball strategies can each assist with debt reimbursement. The proper strategy for you will depend on private choice and your monetary scenario. To search out the correct technique, ask your self:

- Do you want assist staying motivated to repay money owed? If that’s the case, the snowball methodology presents extra small wins to maintain you going.

- Is your monetary administration type analytical and affected person? Then the avalanche methodology will complement a sluggish and regular strategy.

- Do you have got a number of small loans or a number of high-interest loans? The snowball methodology fits the primary scenario, and the avalanche methodology matches the second.

Work to enhance your funds and your credit score with Lexington Legislation Agency

Whether or not that you must rebuild your credit score or get out of debt rapidly, the debt snowball methodology will help. In contrast to different methods, the snowball strategy is straightforward to leap into. Whereas paying off money owed can take time, this methodology offers you the boldness and course to pay down money owed one after the other. Whereas utilizing any debt reimbursement plan, you don’t wish to overlook about sustaining and even bettering your credit score. Keep present on all of your payments, create a funds and observe your spending. In case you’re engaged on repairing your credit score, Lexington Legislation Agency may enable you in your journey with our credit score restore companies.

Be aware: Articles have solely been reviewed by the indicated legal professional, not written by them. The data supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for normal informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained throughout the website don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.