{kind=link}

The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

In sure circumstances, an unapproved inquiry will be eliminated out of your credit score report by sending a credit score inquiry removing letter to the credit score reporting company or by disputing it on-line.

Credit score scores naturally fluctuate from month to month relying in your utilization, funds and transactions. For essentially the most half, your credit score rating is immediately tied to your actions, however there could often be errors in your report. If you happen to discover a sudden decline in your credit score rating, even when solely by a number of factors, chances are you’ll be affected by the impact of an unwarranted credit score inquiry.

Credit score inquiries happen when a lender requests your full credit score historical past from one of many credit score reporting companies. These inquiries into your credit score historical past can have an effect on your credit score negatively and can usually keep in your report for as much as two years. Inquiries mirror what number of instances you could have utilized for credit score, which helps lenders choose whether or not you ought to be accepted for an extension of credit score.

In sure circumstances, an unapproved inquiry will be eliminated out of your credit score report by sending a credit score inquiry removing letter to the credit score reporting company or by disputing it on-line.

The distinction between laborious and comfortable inquiries

Though there isn’t any distinction between the information offered in a tough and comfortable inquiry, they don’t have an effect on your credit score the identical method. A standard false impression is that checking your personal credit score will negatively have an effect on your rating, however this isn’t true. While you verify your personal credit score, it’s thought of a comfortable inquiry and won’t present in your credit score report or have an effect on your rating.

Laborious inquiries, in contrast, happen when a lender pulls your credit score report. A lender could pull your credit score historical past whereas going via an utility for a brand new mortgage, a brand new bank card or any line of credit score. Moreover, banks and property managers could pull your credit score whereas establishing accounts or figuring out approval for an condominium.

Sometimes, a tough credit score inquiry can generally be pulled with out your data, approval or full understanding. Laborious inquiries that have been pulled with out your request will be eliminated out of your credit score report underneath the Truthful Credit score Reporting Act.

How do credit score inquiries have an effect on your credit score rating?

Laborious inquiries account for 10 p.c of your FICO credit score rating. Though the precise impact in your credit score rating will differ relying in your credit score historical past and present standing, you possibly can usually count on to see a brief one to 5 level drop in your general credit score rating.

Though the precise hit to your credit score rating will differ, you possibly can count on to see drops in your rating when these inquiries begin to add up. Sometimes lenders will both pull your credit score by mistake, pull your credit score a number of instances or pull your credit score with out your data by any means.

5 the reason why there are laborious inquiries in your credit score report

Laborious inquiries are the byproduct of making use of for a mortgage, bank card or housing. Understanding how one can take away inquiries from a credit score report is essential to your monetary well being, however figuring out the causes of those inquiries will be simply as essential. Listed below are the most typical sources of laborious inquiries.

1. Bank card utility

Making use of for a brand new bank card will typically be met with a tough inquiry to your credit score report. Monetary establishments want to find out if you happen to’re financially accountable sufficient for a bank card, and your credit score historical past can even affect the credit score restrict you might be awarded.

One exception, nonetheless, is if you happen to’re making use of for one more bank card inside the identical monetary establishment. On this case, they might solely run a comfortable inquiry in case you are in good standing together with your different account.

2. Residence or auto mortgage

Simply as with bank cards, lending establishments want to find out monetary well being earlier than issuing a house or auto mortgage to a shopper—and so they typically accomplish that within the type of a tough inquiry.

It’s essential to notice that you’ll not be penalized for procuring round for favorable charges. Usually, any variety of laborious inquiries on account of house or auto mortgage functions are counted as just one entry in the event that they happen inside 45 days of one another.

3. Housing utility

In case you are making use of to hire a house or an condominium, the owner or rental company could carry out a tough inquiry as a part of their approval course of.

That being stated, laborious inquiries on this occasion are uncommon, as most rental companies verify credit score with comfortable inquiries. In case you are involved a couple of laborious inquiry when making use of for housing, it’s finest to succeed in out to administration earlier than submitting an utility.

4. Different loans

There are extra varieties of loans than simply the house and auto loans outlined above—people can apply for private loans, debt consolidation loans and a number of different choices. Except you might be instructed in a different way, assume that any mortgage utility will end in a tough inquiry sooner or later within the course of.

5. Requesting a credit score restrict improve

There’s a risk that requesting a credit score restrict improve will end in a tough inquiry to your credit score report. That is uncommon, as most monetary establishments will carry out a comfortable inquiry and take a look at earlier utilization historical past, however it’s best to verify together with your establishment earlier than making use of for extra credit score.

Are you able to take away inquiries out of your credit score report?

Laborious inquiries will be eliminated out of your credit score historical past in the event that they occurred with out your approval. If you happen to didn’t have data of the laborious inquiries pulled in your credit score profile, you could have the best to ask for the inquiry to be eliminated.

You possibly can request a tough inquiry be eliminated if:

- The inquiry occurred with out your data

- The inquiry occurred with out your approval

- The variety of inquiries exceeded what you anticipated

Will eradicating an inquiry enhance your credit score rating?

Eradicating an inquiry may enhance your credit score rating, nevertheless it depends upon the kind of inquiry and the way previous it’s.

Mushy inquiries haven’t any impact in your credit score rating, so there isn’t any have to take away them—in truth, chances are you’ll not even see them in your credit score report. Laborious inquiries, however, may end up in a credit score rating drop of as much as 5 factors per inquiry. Efficiently eradicating these entries may enhance your rating relying on the general well being and utilization of your credit score.

Moreover, the age of the inquiry ought to be taken into consideration. Laborious inquiries can keep in your credit score report for as much as two years, however they usually solely influence your rating for six months to 1 12 months. Subsequently, if you happen to’re trying to take away a tough inquiry that’s multiple 12 months previous, it could not enhance your credit score rating.

Learn how to ship a credit score inquiry removing letter

To ship a credit score inquiry removing letter, it’s best to contact any credit score reporting company that’s reporting the inquiry. Credit score inquiry removing letters will be despatched to each the credit score reporting companies and the lender who issued the credit score inquiry.

1. Notify the lender first

Notifying the lender earlier than you ship a removing discover is important if you happen to plan to take the dispute additional to courtroom. That is the right first step for eradicating laborious inquiries.

Make certain to ship the credit score inquiry removing letter through licensed mail. This type of mail offers you proof that the credit score issuer or lender acquired the suitable first notification to take away the laborious inquiry.

2. Embrace a replica of your credit score report

Together with a replica of your credit score report with the highlighted unapproved laborious inquiries could assist others reference your case. Though the credit score reporting companies may have quick access to your report, a tough copy will assist investigators when processing your request.

3. Ship to the suitable credit score bureau

It is very important ship your letter to the credit score bureau with a document of the laborious inquiry you need eliminated. Under are the addresses for every bureau:

Equifax

P.O. Field 740256

Atlanta, GA 30374-0256

Equifax Dispute Info Heart

Experian

P.O. Field 4500

Allen, TX 75013

Experian Dispute Info Heart

TransUnion LLC

Client Dispute Heart

P.O. Field 2000

Chester, PA 19016

TransUnion Dispute Info Heart

What Kind of Gadgets May be Eliminated From My Credit score Report? [Answered] by Lexington Legislation

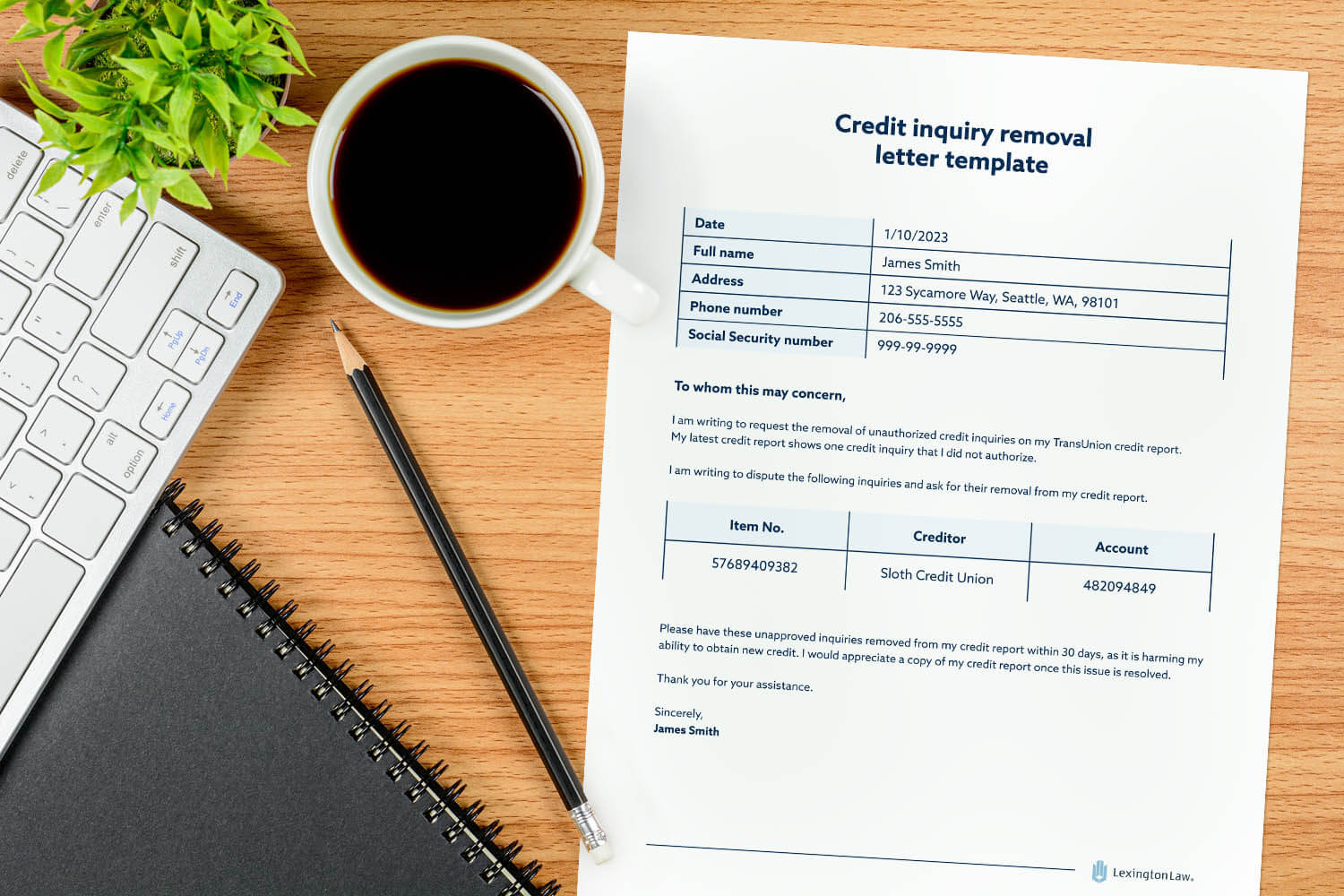

Credit score inquiry removing letter template

Date

Your identify

Your road quantity, road identify

Metropolis, state, ZIP code

Your telephone quantity

Social Safety quantity

Title of credit score bureau

Re: Reporting Unauthorized Credit score Inquiry

To whom this may occasionally concern,

I’m writing to request the removing of unauthorized credit score inquiries on my (identify of the credit score bureau—Equifax, Experian and/or TransUnion) credit score report. My newest credit score report exhibits (variety of laborious inquiries you might be disputing) credit score inquiries that I didn’t authorize.

I’m writing to dispute the next inquiries and ask for his or her removing from my credit score report.

Please have these unapproved inquiries faraway from my credit score report inside 30 days, as it’s harming my capacity to acquire new credit score. I might admire a replica of my credit score report as soon as this subject is resolved.

Thanks in your help.

Sincerely,

(Your Title)

Learn how to keep on prime of unfavorable credit score report gadgets

Eradicating questionable unfavorable gadgets out of your credit score profile could be a lengthy and time-consuming course of that may appear daunting. Though a number of factors’ distinction could not seem to be a big precedence, it is very important keep on prime of those entries earlier than they add up and get uncontrolled.

If holding your credit score rating excessive or enhancing your credit score is a prime precedence, Lexington Legislation Agency could also be possibility for you. Our credit score restore providers may help you with addressing questionable unfavorable gadgets in your credit score report as you’re employed on enhancing your credit score.

Be aware: Articles have solely been reviewed by the indicated lawyer, not written by them. The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for normal informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained inside the web site don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.