{kind=link}

The knowledge supplied on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra data.

Inadequate credit score historical past means you haven’t any confirmed monitor file with collectors that lend cash or different belongings. This prevents lenders from assessing your credit score threat.

Inadequate credit score historical past means you haven’t any confirmed monitor file with collectors with regard to borrowing cash or different belongings. Whether or not you’re making use of for rental property, a private mortgage, a pupil mortgage, a line of credit score or one thing comparable, collectors have to know that you’ll seemingly repay your debt on time. They decide this primarily based in your credit score historical past, which may be present in your credit score report.

A number of the events that may entry your credit score report embrace:

- Insurance coverage firms

- Banks and monetary establishments

- Landlords and employers

- Mortgage lenders, auto mortgage lenders and different lenders

Sadly, most lenders wish to see proof of fine credit score utilization, which implies you usually want credit score historical past to construct credit score historical past—a basic chicken-or-the-egg downside. It could appear inconceivable, however understanding how key elements contribute to your credit score historical past can assist you navigate this example.

Under, we demystify inadequate credit score historical past and present you repair it in 4 steps.

How credit score historical past contributes to credit score scores

Lenders usually depend on an individual’s credit score historical past and rating to judge their creditworthiness and calculate their rates of interest. Though over 90 % of shoppers start to build up credit score historical past of their mid-to-late twenties, greater than 8 million adults are “credit score invisible,” which implies they don’t simply have an inadequate credit score historical past—they’ve zero credit score historical past.

The three main credit score bureaus—TransUnion®, Experian® and Equifax®—accumulate details about the creditworthiness of people from lenders and different events. When somebody applies for credit score, their potential creditor could make an inquiry into their credit score rating. These scores can usually vary from 300, which is extraordinarily poor credit score, to 850, which is exceptionally good credit score.

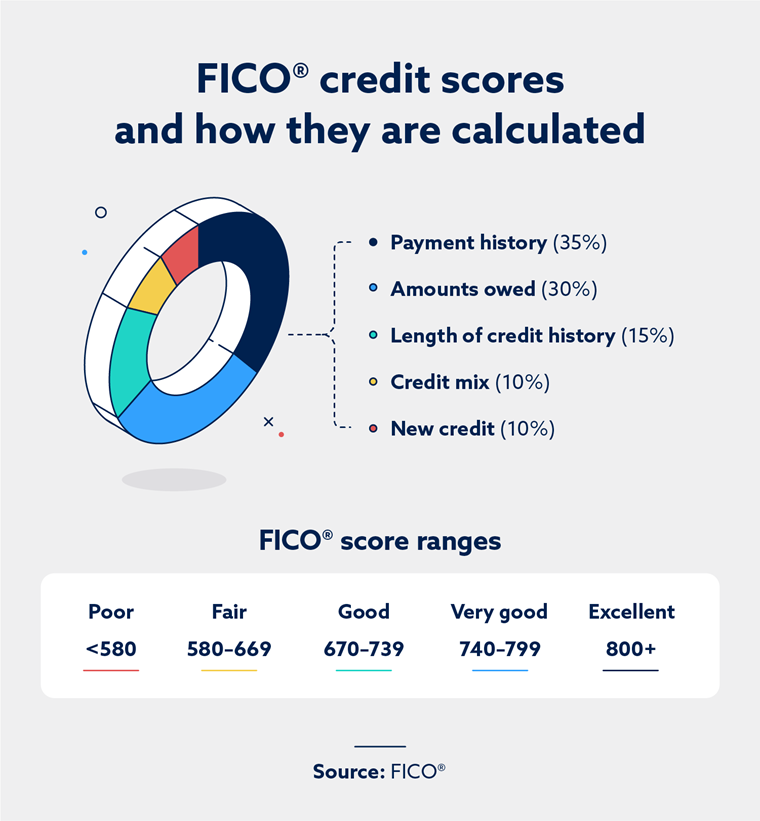

In response to FICO, the algorithm for calculating a credit score rating incorporates 5 elements which can be assigned the next weights:

- 35 %: Fee historical past

- 30 %: Quantities owed

- 15 %: Size of credit score historical past

- 10 %: Credit score combine

- 10 %: New credit score

Taking a look at this breakdown, it’s clear that an important side of your credit score rating is making common, on-time funds for a minimum of the minimal quantity due. It’s additionally vital to take care of a low credit score utilization ratio, which means the balances you keep it up a month-to-month foundation must be comparatively low in comparison with your whole borrowing restrict.

Is one 12 months of credit score historical past sufficient?

Sometimes, you want six months of credit score historical past for a credit score rating to be calculated and reported by the key credit score bureaus. Chances are you’ll have to preserve working past this level to have ok credit score to get accepted at an inexpensive rate of interest, although.

The rate of interest and payback interval for a mortgage often rely in your credit score rating, which in flip is dependent upon the data in your credit score report. For instance, it’s unlikely that somebody with lower than one 12 months of credit score historical past would qualify for a 30-year mortgage.

Remember that your credit score rating doesn’t final without end. You could proceed to show your creditworthiness by paying your money owed on time and making a minimum of the minimal cost due. Which means even with years of credit score historical past, in the event you shut all strains of credit score and repay all money owed, you may return to an inadequate credit score historical past standing, though many gadgets can keep in your report for as much as 10 years.

No credit score vs. below-average credit: Which is healthier?

Having no credit score means having restricted or no credit score historical past, which may disqualify you from bank cards or loans. Nevertheless, it additionally means a clear slate with none damaging marks or delinquencies—a chance to begin constructing a optimistic credit score historical past from scratch.

Very bad credit is brought on by missed funds, defaults or excessive ranges of debt, which might result in increased rates of interest and unfavorable mortgage phrases.

Constructing credit score is feasible with secured bank cards or small loans. Enhancing below-average credit includes addressing money owed and demonstrating accountable monetary habits. No credit score could also be useful for having a contemporary begin, however each conditions require lively efforts to enhance creditworthiness.

The right way to repair inadequate credit score historical past

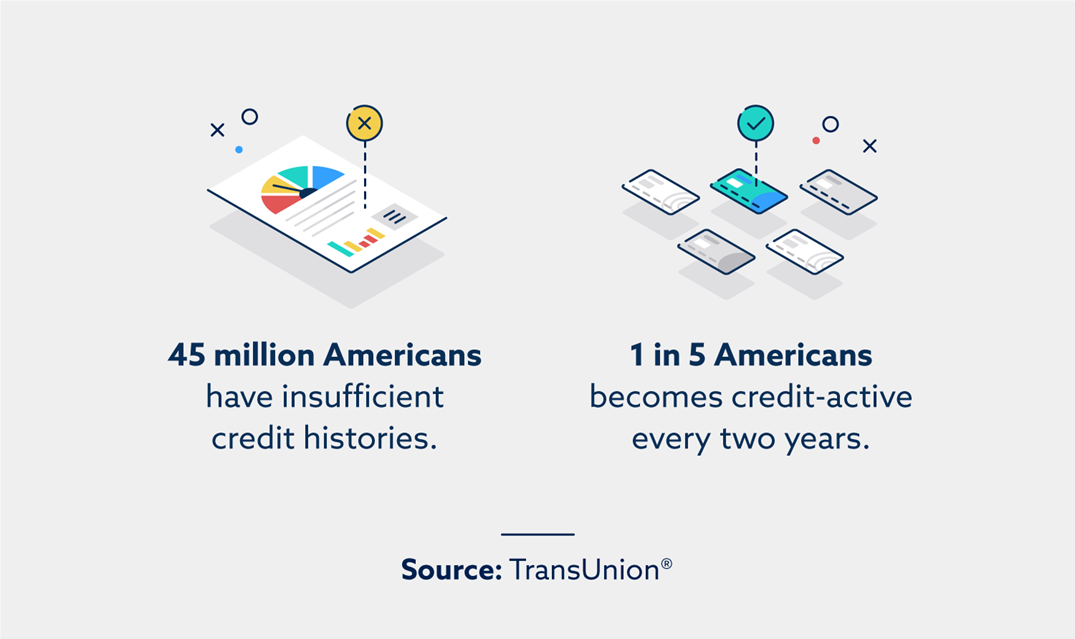

In case you have an inadequate credit score historical past, you’re removed from alone. TransUnion® experiences that 45 million adults are primarily credit score invisible, which means they don’t have sufficient credit score historical past to generate an correct credit score rating. Solely 20 % of those adults change into credit-active each two years.

Sadly, there aren’t any fast fixes for inadequate credit score historical past. The one method to construct belief with lenders is to make constant funds over time.

In case you have inadequate credit score historical past, it’s finest to begin constructing your credit score now. A secured bank card, for instance, permits you to construct credit score with out taking any of the danger related to borrowing cash. You could keep accountable buying habits and make common funds to show your creditworthiness.

When your credit score historical past is inadequate, there are some methods you need to use to proactively construct credit score. Though there isn’t a method to pace up the method of accumulating credit score historical past, observe these steps to construct a greater historical past of creditworthiness.

1. Assessment your credit score report for errors

A research by Client Experiences found that 34 % of individuals have had a minimum of one error on their credit score report. In case you have a lower-than-anticipated credit score rating or none in any respect, evaluation your credit score report and dispute any errors with the credit score bureaus. That is the place a credit score restore firm can doubtlessly make it easier to.

For those who’re deemed to have inadequate credit score historical past, however you imagine you may have established credit score, first contemplate whether or not it’s been greater than six months because you final paid a debt in case your credit score historical past has lapsed. In any other case, verify that every one personally identifiable data (equivalent to your authorized identify, Social Safety quantity and driver’s license quantity) is correct in your mortgage software.

In case your authorized identify is even barely misspelled or is lacking a suffix (Jr., Sr., I, II, III, and so on.), your credit score report may very well be incorrect.

2. Get a safe bank card

In case you have inadequate credit score expertise and, due to this fact, no credit score historical past, you can see it troublesome to get accepted for a mortgage. As an alternative, you need to contemplate safe bank cards as a stepping stone to getting extra credit score.

Safe bank cards are backed by a money deposit as a substitute of your promise to repay the lender (i.e., credit score). Upon getting made good in your guarantees to pay again all purchases and curiosity prices in your secured bank card, you may transition to an unsecured bank card. The unsecured bank card is often when your credit score historical past begins; six months later, you’ll seemingly have a credit score rating.

3. Pay your payments on time

Since between 35 % and 40 % of your credit score rating is calculated primarily based in your cost historical past, you need to pay your payments on time and in full. Anybody who extends credit score to you expects reimbursement at common intervals and for a minimum of the minimal quantity due. Late or incomplete funds could negatively have an effect on your future credit score.

4. Preserve or cut back credit score utilization ratio

With 30 % of your credit score rating relying on the balances you owe to lenders, sustaining a wholesome credit score utilization ratio is really useful. If potential, repay balances in full each month as a substitute of increase debt ranges that change into unsustainable.

As you now know, establishing credit score and credit score historical past is vital, however the work doesn’t finish there. It’s important to watch, keep and, if wanted, proactively work to enhance your credit score. Late funds, collections, defaults and bankruptcies can negatively influence your credit score.

For those who really feel your credit score well being doesn’t precisely replicate your credit score historical past, Lexington Regulation Agency may make it easier to tackle inaccurate damaging gadgets in your report. Get your free evaluation right this moment.

Word: Articles have solely been reviewed by the indicated lawyer, not written by them. The knowledge supplied on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for common informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the website don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.