{kind=link}

The data offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

VantageScore® and FICO® use considerably various factors to find out credit score scores. In addition they have separate necessities for credit score historical past and distinct credit score rating ranges.

VantageScore® and FICO® are each correct credit score scoring fashions with distinctive nuances. For instance, FICO treats credit score combine and age of credit score as two separate classes, whereas VantageScore lumps them into one class (combine and age of credit score).

Lenders can use your FICO rating and VantageScore when deciding to approve or decline your mortgage functions. Studying how each fashions work might help you may have a constructive impression in your credit score. We’ll examine and distinction FICO and VantageScore to assist reply questions like “Why are my credit score scores completely different?”

Key takeaways

- VantageScore and FICO are each correct scoring fashions that use various factors to calculate your credit score rating.

- FICO was established in 1981, whereas VantageScore was based in 2006.

- Fee historical past impacts VantageScores and FICO scores probably the most

Desk of contents:

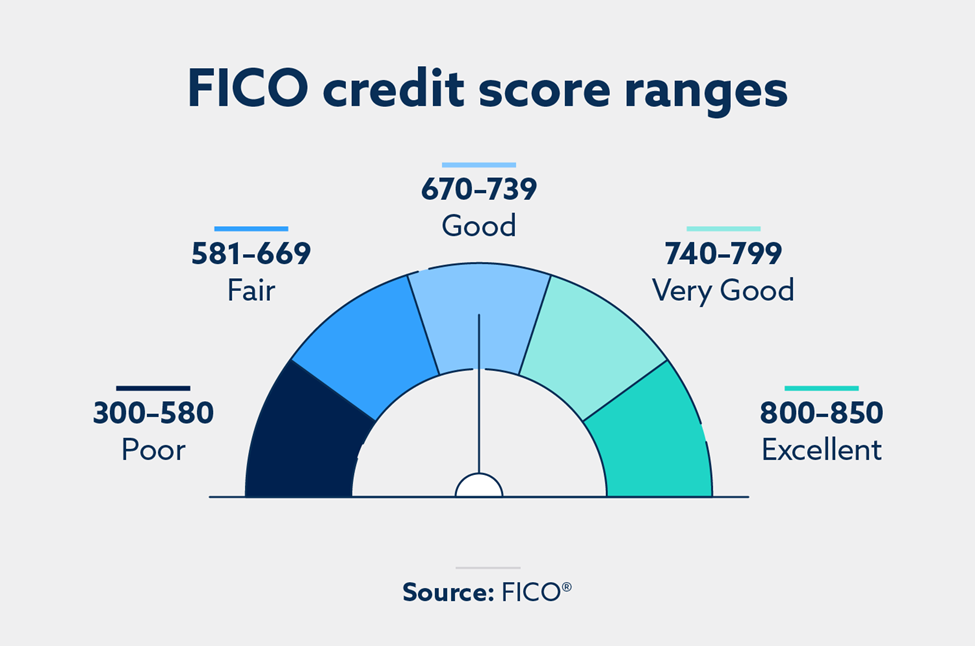

What’s a FICO rating?

Your FICO credit score rating is a credit score scoring mannequin created by the Truthful Isaac Company (FICO) that’s based mostly on info in your credit score reviews with the three main credit score bureaus—Equifax®, Experian® and TransUnion®. FICO rating 8 is the most well-liked model of this mannequin, and different variations can particularly weigh your habits with auto loans and bank cards.

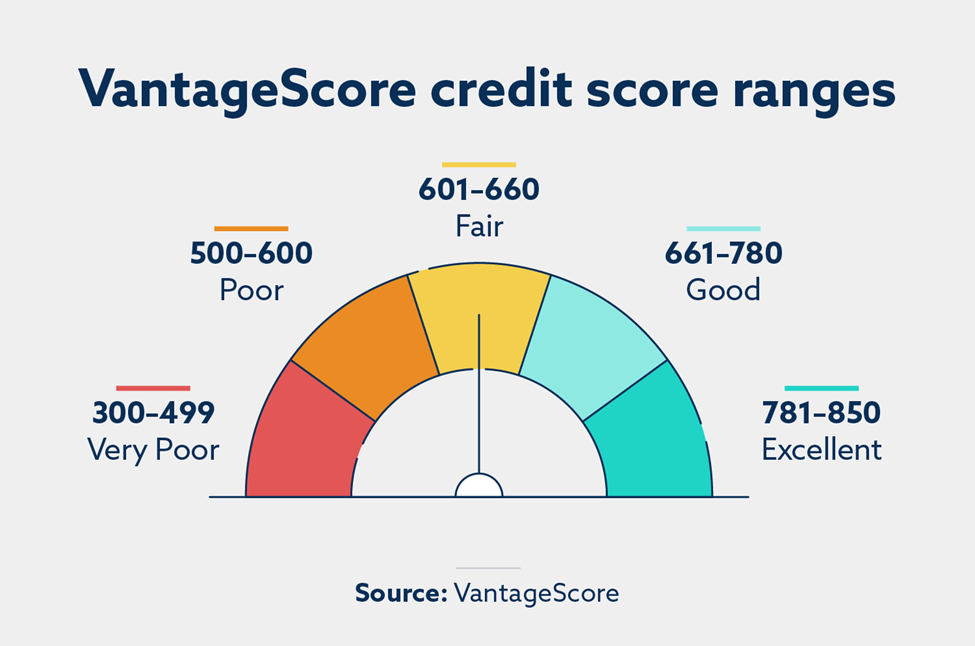

What’s a VantageScore?

Your VantageScore can also be based mostly on info in your credit score reviews with the three main credit score bureaus, and it was created by those self same credit score bureaus as an alternative choice to the FICO scoring mannequin. VantageScore 3.0 is probably the most generally used model of this software, which debuted in 2013. VantageScore 4.0 incorporates machine studying to investigate an individual’s credit score habits over time.

Why are my FICO rating and VantageScore completely different?

There are a number of the reason why your FICO rating and VantageScore could differ, and it comes all the way down to the way in which every mannequin calculates scores. Listed below are a number of ways in which these common scoring fashions differ from one another.

Creation and historical past

The Truthful Isaac Company was based in 1956 (then known as Truthful, Isaac and Firm), they usually created the FICO rating mannequin in 1981. The company’s long-standing historical past is without doubt one of the the reason why so many lenders use its scoring fashions.

VantageScore Options, LLC, created the VantageScore mannequin to gauge your creditworthiness utilizing a distinct formulation than FICO. This mannequin was created in 2006, and plenty of lenders have adopted it since.

Minimal scoring standards

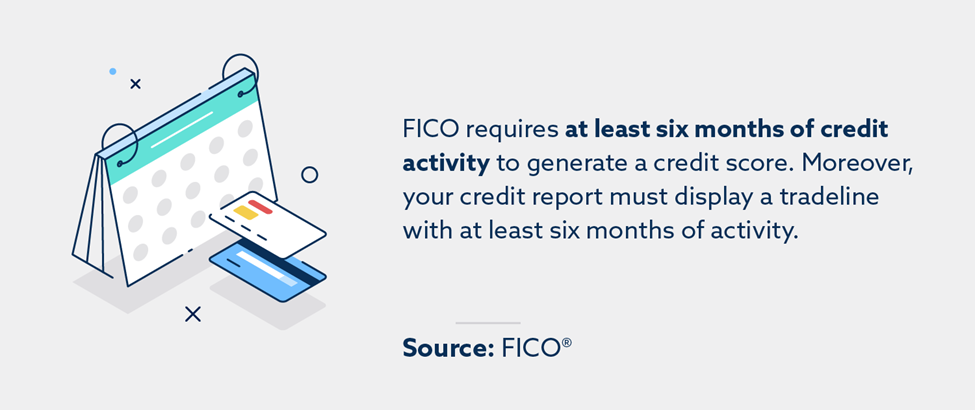

FICO requires at the least six months of credit score exercise to generate a credit score rating. Furthermore, your credit score report should show a tradeline (which refers to an merchandise equivalent to a bank card or line of credit score) with at the least six months of exercise.

VantageScore merely asks that shoppers have at the least one tradeline merchandise on their credit score reviews. There’s additionally no minimal month-to-month requirement for that merchandise.

Credit score rating values

When evaluating your VantageScore vs. FICO rating, understanding which components have an effect on every mannequin is essential.

FICO Rating 8 consists of the next 5 components:

- Fee historical past (35 p.c): Gauges how typically you make funds on time.

- Accounts owed (30 p.c): Weighs how a lot of your obtainable steadiness you’ve used.

- Credit score age (15 p.c): Measures the common age of your open credit score accounts.

- Credit score combine (10 p.c): Signifies how numerous your open credit score accounts are.

- New credit score (10 p.c): Seems at any new credit score accounts you’ve utilized for.

VantageScore 3.0, however, appears at these six metrics:

- Fee historical past (40 p.c): Weighs your on-time funds and your missed funds.

- Depth and age of credit score (21 p.c): Measures your credit score combine and the common age of your credit score.

- Credit score utilization (20 p.c): Is identical as FICO’s “accounts owed” class.

- Whole balances (11 p.c): Seems at your excellent balances throughout all accounts.

- Current credit score (5 p.c): Examines your habits with new credit score.

- Out there credit score (3 p.c): Refers to how a lot credit score you at present have obtainable.

Primarily based on these components, it’s simple to see why your FICO rating and VantageScore can differ. Credit score combine is scrutinized by VantageScore excess of FICO, which is why it will probably assist to responsibly handle completely different credit score accounts. FICO, however, weighs new credit score exercise extra closely—so tempo your self when making use of for brand spanking new credit score.

Is your FICO rating or VantageScore extra essential?

Your FICO rating and VantageScore are each essential as a result of they might help you get a way of your present credit score habits. Nevertheless, auto mortgage lenders, industrial banks and landlords favor FICO. Which means your utility for a brand new rental property will doubtless be authorised or declined based mostly on the energy of your FICO credit score rating.

There’s a variety of overlap between FICO and VantageScore, so most credit-building ideas apply to each fashions. For instance, cost historical past is an important issue for each FICO and VantageScore, so making well timed funds will positively impression each scores.

A number of different methods to extend your credit score scores embody:

- Ceaselessly verify your credit score report back to dispute errors and overview your habits.

- Restrict the variety of bank cards or loans you apply for .

- Learn the way Lexington Legislation Agency’s focus tracks might help you rebuild your credit score after main life occasions.

Monitor your credit score with Lexington Legislation Agency

Accountable credit score habits will construct your credit score regardless of which mannequin is being taken under consideration. Lexington Legislation Agency might help you higher perceive your present credit score habits, enable you to handle account inquiries and handle errors in your credit score reviews.

Be taught extra about our companies and see if they are going to fit your wants.

Notice: Articles have solely been reviewed by the indicated legal professional, not written by them. The data offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for common informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the web site don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.