{kind=link}

In the event you’ve been researching mortgages, or are within the strategy of taking out a house mortgage, you’ll have come throughout the time period “impounds” or “escrows.”

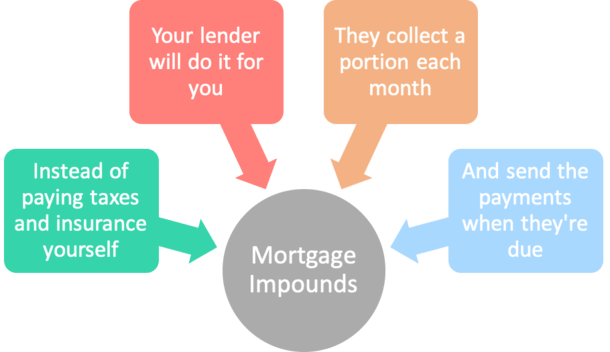

While you hear these seemingly advanced phrases, the mortgage officer or mortgage dealer is just referring to an impound account, also referred to as an escrow account.

Right here’s the way it works. Every month, a portion of property taxes and owners insurance coverage are collected alongside together with your common mortgage cost, then disbursed to the suitable events when due.

This association ensures the lender that taxes and insurance coverage are paid on time, as a substitute of counting on the house owner to make the funds themselves.

It protects the lender’s curiosity within the property since taxes are obligatory and insurance coverage shields the collateral from hurt.

What Are Mortgage Impounds?

- A housing cost features a mortgage, owners insurance coverage, and property taxes

- Impounds (or escrows as they’re additionally recognized) refers back to the automated assortment of taxes and insurance coverage

- It ensures the house owner has funds obtainable to make these necessary funds when due

- A portion of those prices is taken out of your housing cost every month and put aside till disbursement

Many mortgages as of late require an escrow account to make sure the well timed disbursement of property taxes and owners insurance coverage premiums.

This account is managed by a third-party middleman, usually a mortgage servicer, who collects and disperses funds on behalf of the house owner.

Householders pay cash into the escrow account at mortgage closing, and every month after that with their mortgage cost.

Over time, the stability grows and when property taxes and owners insurance coverage are due, the cash is distributed on to the tax collector or insurance coverage firm, respectively.

As a substitute of paying property taxes twice a yr, or owners insurance coverage as soon as yearly, you pay a significantly smaller installment quantity every month as a substitute.

Together with every mortgage cost you additionally pay roughly 1/12 of the annual property tax invoice and 1/12 of the annual owners insurance coverage premium.

That is the place the acronym “PITI” originates from – Principal, Curiosity, Taxes, and Insurance coverage.

The taxes and insurance coverage are paid upfront and the cash is “impounded,” aka seized till being distributed. That’s the place the identify impound comes from.

And escrow merely refers to a third-party who holds the funds and directs them to the place they should go.

As famous, it’s essential to additionally pay an “preliminary escrow deposit” at mortgage closing, which can fluctuate significantly primarily based on the month you shut, and the place the property is positioned.

Lenders might also acquire one or two additional months of funds to behave as a cushion for future will increase in taxes and insurance coverage, however this quantity is strictly regulated.

Why Mortgage Impounds?

- They mainly exist to guard the lender from borrower default

- Assuming the house owner falls behind on taxes or fails to make insurance coverage funds

- The month-to-month assortment of funds ensures the cash might be obtainable when funds are due

- And removes a scenario the place the borrower is unable to make what are sometimes very massive funds

An impound account significantly advantages the lender as a result of they know your property taxes might be paid on time, and that your owners insurance coverage received’t lapse.

In any case, if you must pay it multi function lump sum, there’s an opportunity you received’t have the required money available.

Keep in mind, the typical American has little to no financial savings, so if an enormous cost is due, uh-oh!

Clearly that is necessary as a result of the lender, NOT you, is the one that actually owns your house if you’ve acquired a large mortgage connected to it.

They usually don’t need something to come back in between the curiosity in THEIR property within the occasion you’re unable to make these crucial funds.

Many appear to assume lenders require impounds to allow them to earn curiosity in your cash, nevertheless it’s actually to guard their curiosity within the property.

*Additionally, some states require lenders to pay owners curiosity on their impound account balances anyway.

In California for instance, it’s customary for mortgage escrow accounts to earn curiosity. Annually it’s best to obtain a tax type that exhibits what you have been paid and what you OWE in consequence.

Make sure to verify your personal state legislation to find out should you’ll earn curiosity. In any case, it possible received’t be very a lot cash, and it’s taxable…

Impound accounts may profit debtors as a result of the cash is collected steadily over time, so there isn’t that massive sudden hit when taxes or insurance coverage are due.

For that reason, some debtors really desire impound accounts, particularly those who are inclined to do a poor job managing their very own funds.

And also you shouldn’t miss a cost or pay late as a result of it’s all accomplished for you routinely. It’s really fairly handy.

[Homeowners insurance vs. mortgage insurance]

Paying Property Taxes and Householders Insurance coverage Your self

- You could have the choice to pay these payments your self as nicely

- However solely on sure kinds of mortgage loans

- Comparable to typical loans (conforming and jumbo mortgage quantities)

- Or on loans with a down cost of 20% or extra

- However it might value you .125% of the mortgage quantity to waive them!

In the event you’re the sort that likes full management over your cash, you’ll be able to all the time pay your property taxes and owners insurance coverage your self if the underlying mortgage permits for it.

On this case, you “waive impounds,” which often entails paying a payment to the lender, resembling .125% or .25% of the mortgage quantity at closing.

For instance, in case your mortgage quantity is $200,000, you may be taking a look at a price of $250 to $500 to take away impounds. It’s not insignificant.

Or, waiving impounds/escrows might come within the type of a barely larger mortgage charge should you don’t wish to pay the escrow waiver payment out-of-pocket.

Both approach, there may be usually a value, although you’ll be able to all the time attempt to negotiate your mortgage charge with the lender to get them waived and nonetheless safe a low charge.

Simply remember that you’ll be able to’t all the time waive impounds relying on mortgage kind.

Impounds are required on FHA loans, VA loans, and USDA loans.

For typical loans, impounds are typically required should you put lower than 20% down, which is the case for many debtors.

And even then, many lenders cost debtors in the event that they wish to waive impounds, regardless of their loan-to-value ratio being tremendous low.

In California, impounds are technically solely required if the loan-to-value ratio (LTV) is 90% or larger. However you should still must pay to waive them both approach.

It’s seemingly unfair, however like all different companies, they acquired inventive and got here up with one more factor to cost you for. Sadly, try to be used to this by now.

Find out how to Take away Mortgage Impounds

- You’ll be able to request the elimination of impounds as soon as your LTV is at/beneath 80%

- Both by paying down your mortgage over time or through lump sum cost

- However there’s no assure the lender will agree to take action

- It’s nonetheless a voluntary determination on their half to take away them at your request

In the event you initially arrange an escrow account, you could possibly get it eliminated later down the road.

Merely contact your mortgage servicer and ask them to assessment your escrow account.

As a rule of thumb, your request is extra prone to get authorized in case your LTV is at or beneath 80%. That approach they know you’ve acquired pores and skin within the recreation.

That 20% in house fairness provides the lender enough safety from potential default should you fail to pay property taxes or house insurance coverage in a well timed style.

But it surely’s not a assure for elimination. Generally they’ll merely balk at your request, even if in case you have a ton of fairness.

Additionally be aware that if in case you have an escrow account and refinance your mortgage, the cash ought to be refunded to you inside 30 days of paying off your previous mortgage.

The Annual Escrow Evaluation

- Mortgage servicers are required by legislation to assessment your escrow account yearly

- This occurs every year in your origination date to make sure it’s balanced

- In the event you paid an excessive amount of it’s possible you’ll obtain an escrow surplus refund verify

- In the event you didn’t pay sufficient it’s possible you’ll have to pay an escrow scarcity

Annually on the anniversary date of your mortgage closing, your lender is required by federal legislation to audit your impound account and refund any extra over the allowable cushion.

Additionally, you will obtain an escrow evaluation assertion that may be helpful to look over.

Usually, the minimal stability required for an escrow account is 2 months of escrow funds, which covers any will increase in taxes and insurance coverage.

When your mortgage servicer tasks the numbers for the yr forward, any surplus, which is your estimated lowest account stability minus the minimal required stability, might be refunded to you.

In case your account stability is larger than this minimal quantity, it’s possible you’ll be refunded the distinction through verify. It’s a pleasant shock when it comes within the mail!

Assuming you aren’t simply despatched a verify that may be cashed, it’s possible you’ll get the choice to use any overage to principal discount or to a future mortgage cost.

You may as well be proactive if it seems as in case your impound account is a little bit too full. Merely name and ask them to have a look through an escrow account overage evaluation.

Conversely, it’s doable that you could be expertise an escrow scarcity, by which case you’ll be billed for the quantity wanted to fulfill the shortfall.

Whereas not as good as a verify, it signifies that you simply haven’t been overpaying all year long.

The mortgage servicer might also provide the choice to simply accept a better month-to-month cost going ahead to make amends for any scarcity.

Be aware that each an escrow account surplus and lack can lead to a special month-to-month mortgage cost, since they’ll acquire roughly from you sooner or later.

For instance, should you have been paying an excessive amount of final yr, you may be advised that your new month-to-month cost is X {dollars} much less. Your mortgage cost went down. One other sudden shock!

In the event you have been paying too little, the reverse may be true – your mortgage cost might go up!

Nevertheless, the distinction will usually be fairly small relative to the general cost.

It’s At all times Your Accountability to Pay on Time

- No matter the way you pay taxes and insurance coverage

- It’s all the time your sole duty to make sure they’re paid on time

- You’ll be able to’t essentially blame the mortgage lender/servicer in the event that they slip up

- So all the time comply with up to ensure the funds are made on time

No matter whether or not you go along with impounds or resolve to waive them, it’s your duty to make sure that your property taxes and insurance coverage are paid on time, every yr.

Certain, your mortgage servicer will in all probability pay on time, however this will not all the time be the case. Errors occur.

Additionally, should you’re topic to paying supplemental property taxes, your mortgage servicer might inform you that it’s your duty to care for them by yourself.

In the event you obtain a supplemental property tax invoice within the mail, it’s possible you’ll wish to name your servicer instantly to find out if it is going to be paid through your escrow account. If not, you’ll have to ship cost your self.

Conditions like these are reminder to all the time regulate your escrow account, and to maintain strong data of your taxes and insurance coverage.

In abstract, it may be good for another person to deal with these funds in your behalf, however you continue to have to ensure they’re doing their job!

Professionals and Cons of an Impound Account

The Professionals

- No shock tax/insurance coverage invoice each six or 12 months

- Taxes and insurance coverage are paid steadily all year long

- Simpler to create a price range and handle different bills

- Higher thought of how a lot home you’ll be able to actually afford

- Don’t must bodily make the tax/insurance coverage funds your self

- No payment (or mortgage charge improve) for the elimination of impounds

The Cons

- Your mortgage cost might be larger every month

- Much less liquidity as a result of cash is being held in escrow

- Could possibly be utilizing that cash in different methods and doubtlessly incomes a better return

- Mortgage servicer might make a mistake whereas making funds in your behalf

- Should take care of your mortgage cost altering yearly

(photograph: Constantine Agustin)