{kind=link}

The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra data.

There are a number of doable the explanation why your credit score rating gained’t go up, such because the lender hasn’t reported to the credit score bureaus but, you will have fallen behind on funds, you will have excessive credit score utilization or you will have a brief credit score historical past.

A good credit score rating might help you get accepted for loans, safe low rates of interest, and obtain the perfect phrases. Nonetheless, bettering your credit score may be difficult, particularly should you really feel caught at a sure quantity.

For those who ceaselessly test your credit score rating and don’t see the quantity change, it’s possible you’ll marvel, “Why gained’t my credit score rating go up?” On this submit, we’re going to dive into 10 potential the explanation why your credit score rating is stagnant and what to do about it. Learn on to study extra.

Desk of contents:

1. Your credit score rating hasn’t been up to date but

Lenders usually report back to the three credit score bureaus each 30 to 45 days. Due to this fact, it may well take as much as a month in your credit score rating to replicate new adjustments. For those who lately paid off an account and haven’t seen a change in your rating but, there’s no want to fret.

What to do about it: For those who don’t see the replace mirrored in your credit score report after a month or two, think about contacting your lender.

2. You’ve fallen behind on funds

Fee historical past is a elementary issue that impacts your credit score—accounting for 35 % of your FICO® rating. If a cost is over 30 days overdue, your lender will report it to the credit score bureaus. Even one late cost can harm your credit score considerably. Late funds additionally keep in your credit score report for as much as seven years, though their affect in your credit score report declines over time.

What to do about it: Get within the behavior of constructing constant on-time funds.

3. You could have excessive credit score utilization

Your credit score utilization, or the sum of money you owe in comparison with your credit score restrict, is one other issue that influences your credit score. For instance, in case your credit score restrict is $12,000 and also you owe $3,000, your credit score utilization charge is 40 %.

Whereas utilizing your obtainable credit score isn’t essentially unhealthy, a excessive credit score utilization charge can sign to lenders that you simply’re reliant on credit score and, subsequently, are a high-risk borrower.

What to do about it: Goal to maintain your credit score utilization beneath 30 % by decreasing your spending or growing your credit score restrict.

4. You could have a brief credit score historical past

Your size of credit score historical past, or the period of time your accounts have been established, accounts for 15 % of your FICO rating. A protracted credit score historical past is useful to your credit score as a result of it supplies lenders with sufficient knowledge to precisely decide your credit score threat. Keep in mind that whereas a protracted credit score historical past is useful, FICO assures that it’s “not required for a superb credit score rating.”

What to do about it: Be affected person and maintain previous credit score accounts open.

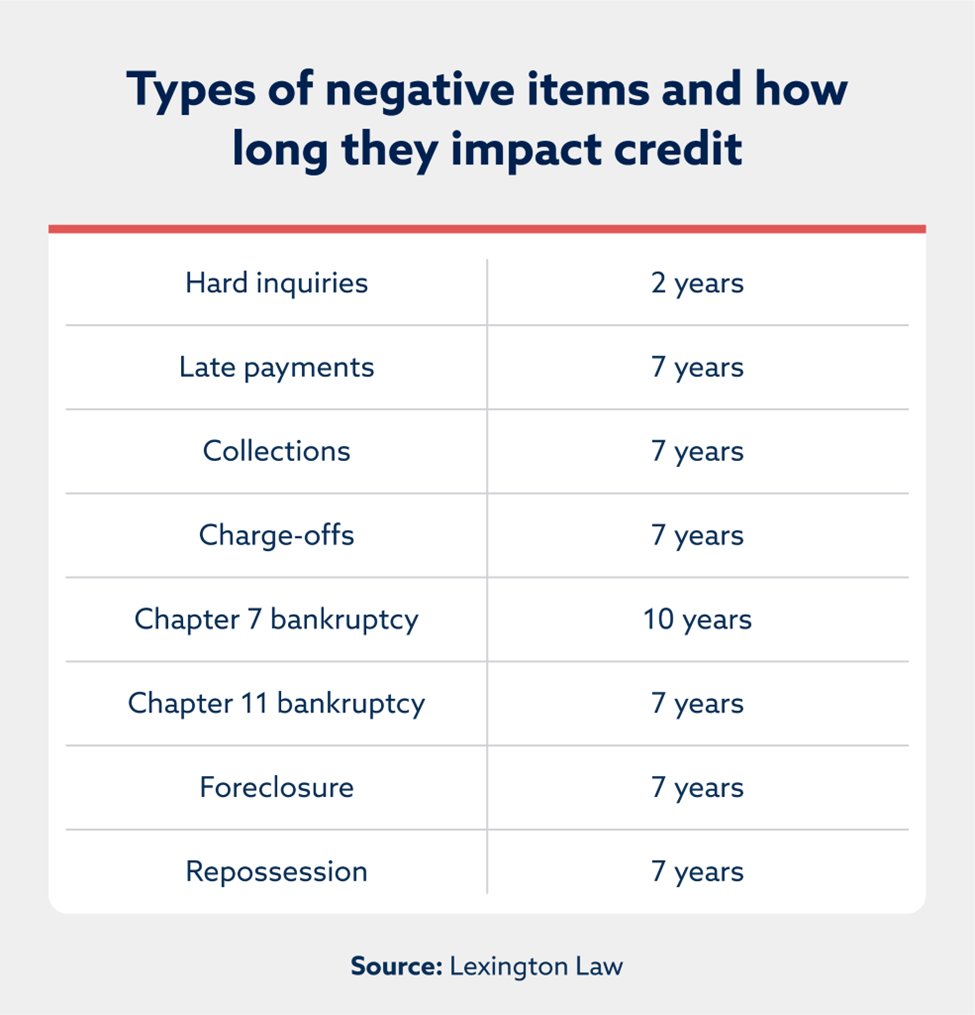

5. You could have adverse objects in your credit score report

Delinquent accounts, bankruptcies, charge-offs, and assortment accounts are all main adverse objects. You probably have any of those in your credit score report, they might be stopping you from bettering your credit score.

Though adverse data will finally fall off your credit score report, the period of time that takes is determined by the kind of adverse merchandise. Most adverse data stays in your credit score report for about seven years.

What to do about it: Whereas not assured, you may strive sending a pay for delete letter or request a goodwill deletion out of your creditor to get the adverse objects eliminated.

6. Your credit score combine isn’t numerous

Credit score combine refers back to the number of credit score accounts you maintain. Examples of credit score accounts embrace bank cards, mortgages, auto loans, bank cards, installment loans, and so forth. Credit score combine determines 10 % of your credit score rating.

What to do about it: Whilst you don’t essentially want considered one of every kind of credit score, think about opening new accounts to diversify your credit score combine.

7. You could have a number of new arduous inquiries

While you submit a brand new credit score software, the creditor will carry out a arduous inquiry in your credit score file, which may briefly decrease your rating. Whereas the influence of a tough inquiry is simply round 5 factors, a number of credit score inquiries can add up and trigger a major drop in your credit score.

For those who ceaselessly apply for brand spanking new credit score, the compounding arduous inquiries could also be stopping you from bettering your rating.

What to do about it: Wait at the very least six months between every new credit score software to restrict the impact of arduous inquiries in your credit score.

8. Your credit score rating is already excessive

These with superb or wonderful credit score scores might wrestle to advance their credit score standing. The higher your credit score rating, the tougher it turns into to boost it as a result of there’s much less room for enchancment. As soon as your rating is within the 700s or 800s, growing it may be difficult.

What to do about it: Sustain along with your good credit score habits, however remember that progress might sluggish as your rating will increase.

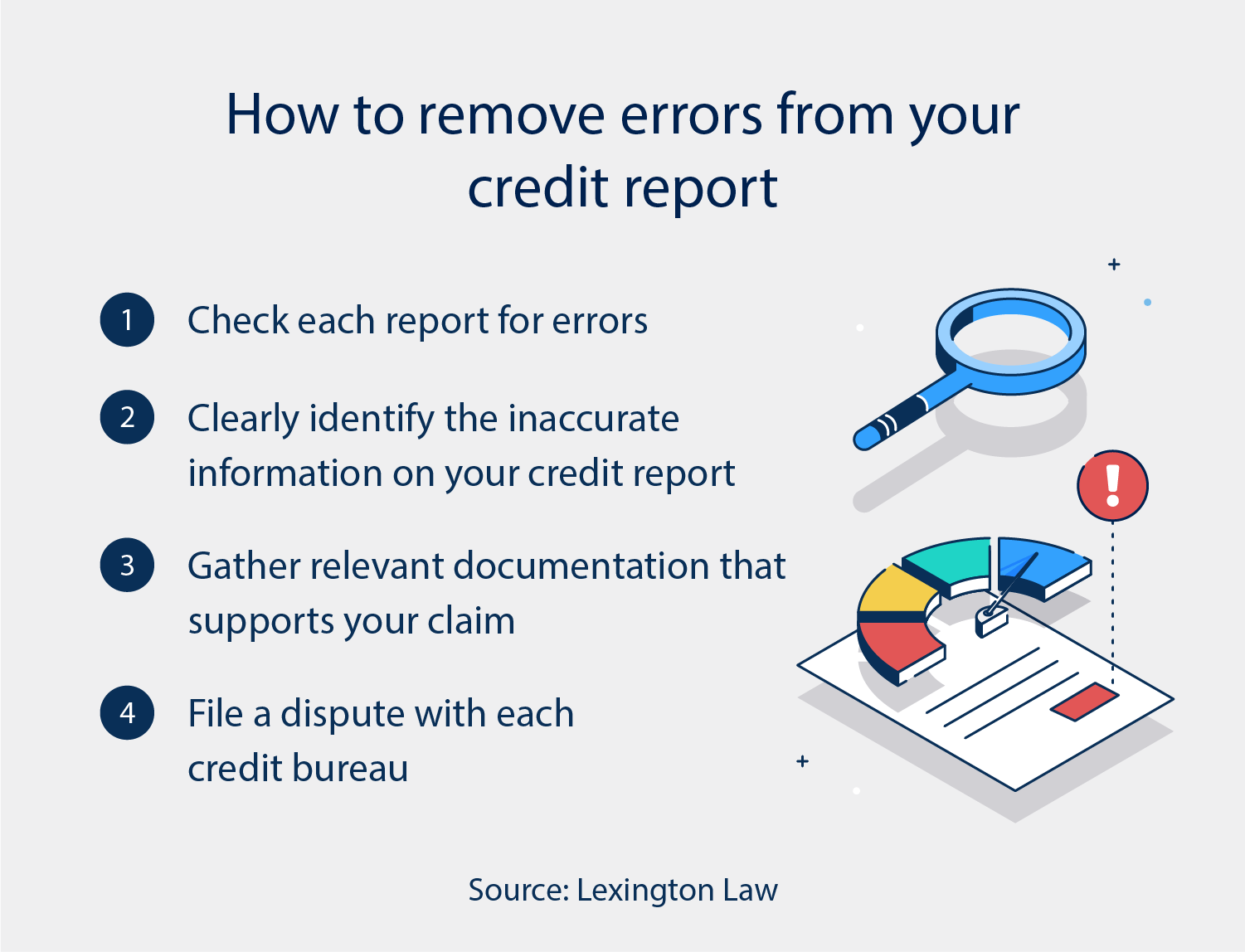

9. You could have errors in your credit score report

Errors in your credit score report can injury your credit score. Evaluation your credit score report at the very least yearly to test for inaccurate data. In keeping with the Client Monetary Safety Bureau, frequent errors embrace:

- Identification errors

- Misreported account standing

- Knowledge administration errors

- Inaccurate balances

What to do about it: For those who discover an error in your credit score report, file a dispute with the credit score bureaus to get it corrected.

10. You’ve been a sufferer of id theft or fraud

Id theft can wreak havoc in your credit score rating. Scammers can open new accounts in your title, buy objects along with your bank card and extra. That’s why it’s necessary to maintain an eye fixed out for the next warning indicators of id theft:

- Prices for purchases you didn’t make

- Calls from debt collectors relating to accounts you didn’t open

- Accounts in your credit score report that you simply didn’t open

- Mortgage purposes getting rejected

- Mail stops being delivered to, or is lacking from, your mailbox

What to do about it: For those who suspect you’ve been a sufferer of id theft, make sure that to arrange fraud alerts and freeze your credit score. Prepared to maneuver the needle in your credit score rating? At Lexington Regulation Agency, we’ll decide what inaccurate adverse objects could be hurting your credit score and deal with them with the credit score bureaus. Amongst our companies, we provide an Id Theft Focus Monitor, created particularly for people financially recovering from id theft. Get began at the moment.

Notice: Articles have solely been reviewed by the indicated legal professional, not written by them. The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for normal informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained inside the web site don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.