{kind=link}

The data supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra data.

For those who’re contemplating taking out a mortgage or bank card, you’ve in all probability checked your credit score rating to weigh your odds of getting accredited. However what if it’s totally different relying on which scoring mannequin you examine?

Since you might have a number of varieties of credit score scores, the quantity can fluctuate primarily based on the scoring mannequin. Proceed studying to be taught extra concerning the totally different credit score scores, together with FICO® and VantageScore®.

Desk of contents:

What’s a credit score rating?

A credit score rating is a three-digit quantity that predicts your credit score threat primarily based on information out of your credit score report. Lenders use credit score scores to find out who to approve for loans and at what rates of interest. Credit score scores sometimes vary from 300 to 800 factors. A excessive credit score rating signifies that you simply’re extra prone to pay again your loans, whereas a decrease credit score rating indicators that you could be be a dangerous borrower.

What are the totally different credit score scoring fashions?

FICO and VantageScore are the 2 hottest scoring fashions utilized in the US. Each fashions calculate your rating primarily based on a set of things that assess a person’s credit score threat. Nevertheless, the 2 fashions use totally different algorithms and assign totally different weights to every issue.

Let’s have a look at the various kinds of credit score scores and the way they stack up.

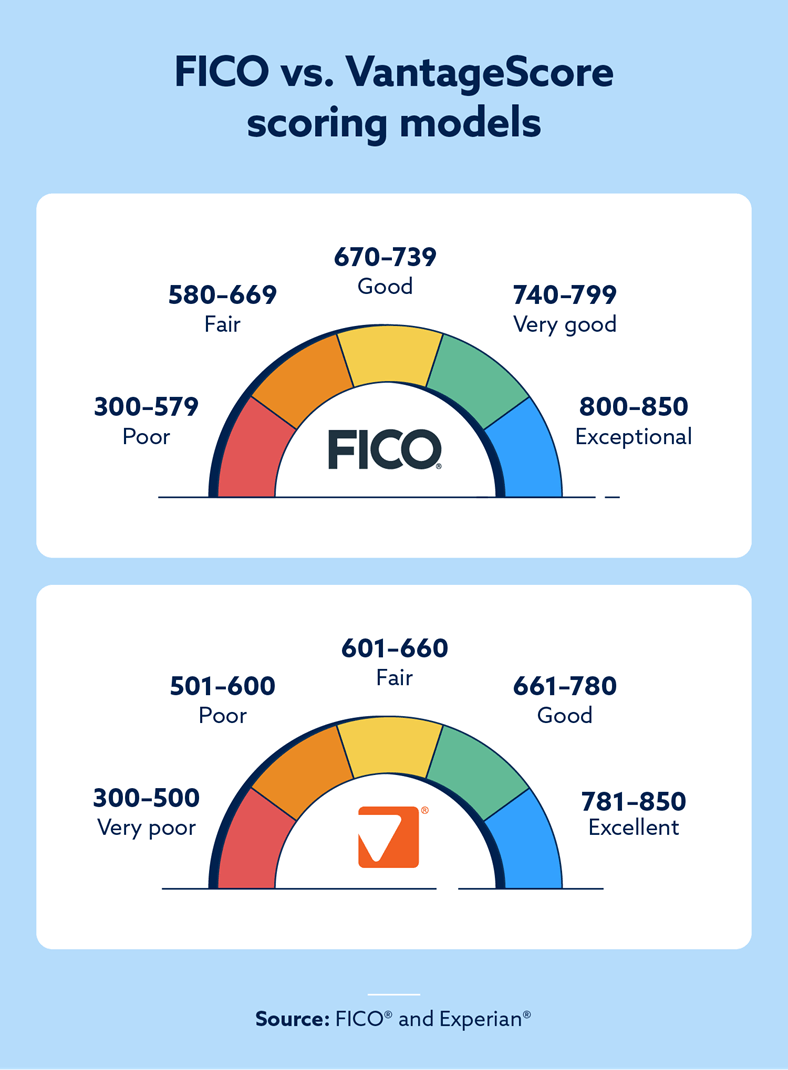

FICO scoring mannequin

The FICO rating was the primary shopper credit score rating developed by the Honest Isaac Company (FICO) in 1989. In keeping with myFICO, 90 p.c of prime lenders use FICO scores to find out mortgage approvals, rates of interest and credit score limits.

A superb FICO rating will aid you safe higher mortgage phrases and charges. The newest FICO mannequin categorizes your rating primarily based on these ranges:

- 800+: Distinctive

- 740 – 799: Superb

- 670 – 739: Good

- 580 – 669: Honest

- <580: Poor

VantageScore mannequin

The VantageScore mannequin was developed in 2006 by the three credit score bureaus—Experian®, TransUnion® and Equifax®—in its place scoring mannequin.

Just like the FICO scoring mannequin, VantageScore ranges from 300 to 850. In keeping with Experian, right here’s how the latest VantageScore mannequin teams scores:

- 781+: Glorious

- 661 – 780: Good

- 601 – 660: Honest

- 500 – 600: Poor

- <500: Very poor

Different credit score scoring fashions

Whereas FICO and VantageScore are probably the most extensively used, they aren’t the one scoring fashions on the market. Listed below are some lesser-known credit score scoring fashions you could encounter:

- TruVision Credit score Threat: Developed by TransUnion, TruVision goals to broaden credit score alternatives with insights past conventional credit score data. The mannequin combines “conventional, trended, blended and various information.”

- OneScore: Unveiled in 2023 by Equifax, OneScore is a brand new scoring mannequin aimed to color a extra complete image of mortgage candidates. In keeping with a current press launch, OneScore is a “strong, multi-data rating that leverages conventional credit score historical past and differentiated various information.”

- CE Credit score Rating: Created by CE Analytics, CE is an impartial credit score scoring mannequin that makes use of superior analytics and behavioral traits.

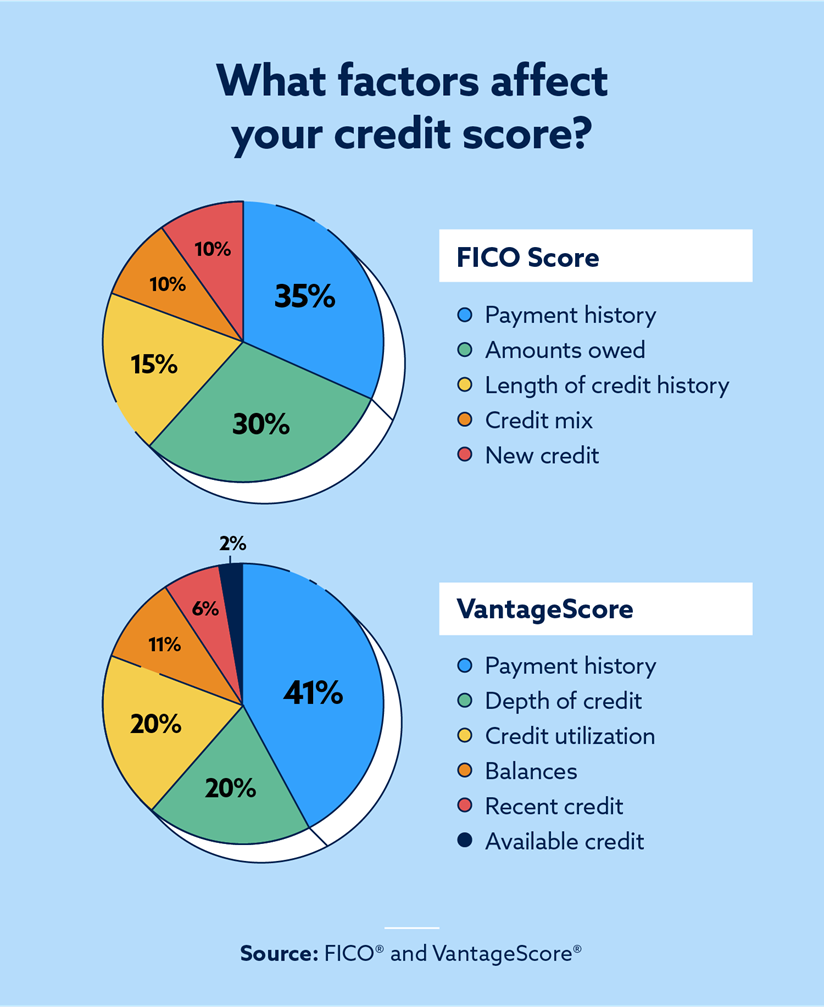

How are credit score scores calculated?

Your credit score scores are calculated primarily based on a set of things out of your credit score report. Nevertheless, every scoring mannequin assigns a sure weight to every issue to calculate your rating.

Let’s have a look at how the FICO and VantageScore fashions calculate credit score scores.

How is your FICO rating calculated?

With the newest FICO scoring mannequin, your historical past of paying previous accounts on time is crucial issue when figuring out your credit score rating. Different components embody how a lot of your accessible credit score you’re utilizing, how lengthy you’ve had your accounts, the various kinds of loans you might have and what number of new accounts you might have.

Right here’s precisely how FICO calculates your rating:

- Fee historical past: 35 p.c

- Quantities owed: 30 p.c

- Size of credit score historical past: 15 p.c

- Credit score combine: 10 p.c

- New credit score: 10 p.c

How is your VantageScore calculated?

Just like the FICO mannequin, cost historical past is probably the most vital issue when calculating your VantageScore. Extra components embody the age of your accounts, how a lot credit score you utilize, whole balances in your accounts, new accounts you’ve opened and the way a lot credit score you might have accessible.

Right here’s a have a look at the components that decide your VantageScore:

- Fee historical past: 41 p.c

- Depth of credit score: 20 p.c

- Credit score utilization: 20 p.c

- Balances: 6 p.c

- Latest credit score: 11 p.c

- Out there credit score: 2 p.c

Why are my credit score scores totally different?

It’s regular to your credit score scores to be totally different. Listed below are a number of of the primary causes credit score scores fluctuate:

- Your rating is calculated utilizing totally different scoring fashions: Your credit score scores might fluctuate as a result of there are a number of various kinds of credit score scoring fashions. Since scoring fashions weigh sure components otherwise, your rating might fluctuate barely relying on which credit score rating you examine.

- There are totally different variations of credit score scoring fashions: Every scoring mannequin has a number of variations that periodically replace. For instance, FICO 8 and FICO 9 have key variations, such because the influence of third-party collections and hire funds.

- Not all lenders report back to all three credit score bureaus: One more reason your credit score rating might fluctuate is as a result of some lenders don’t report back to all three credit score bureaus. Consequently, one of many credit score bureaus could possibly be lacking data that both will increase or decreases your rating.

- Credit score scores replace incessantly: While you examine your credit score rating can play a job in what quantity you see. Credit score scores usually replace not less than as soon as a month and generally even a number of instances per 30 days. So even for those who’re utilizing the identical scoring mode, it’s regular to your credit score rating to fluctuate over time.

Tips on how to examine your credit score rating

Accessing your credit score rating doesn’t should be a problem. Listed below are the best methods to examine your credit score rating free of charge:

- Credit score bureaus: You’ll be able to examine your credit score rating by way of any of the three main credit score bureaus—Experian, TransUnion and Equifax.

- Your financial institution or bank card issuer: Most banks and bank card issuers present prospects with complimentary entry to their credit score rating.

- Third-party platform: Some third-party platforms present free credit score scores. For instance, Lexington Legislation Agency gives a free credit score snapshot, which incorporates your credit score rating and credit score report abstract.

Often checking your credit score rating and credit score report can assist notify you of inaccurate data which may be hurting your credit score. For those who discover errors in your credit score report, it’s necessary to analyze and handle them with the credit score bureaus.

Find out how Lexington Legislation Agency’s companies may aid you successfully handle and monitor your credit score right now.

Observe: Articles have solely been reviewed by the indicated legal professional, not written by them. The data supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained throughout the web site don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.