{kind=link}

The data supplied on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation Agency’s editorial disclosure for extra data.

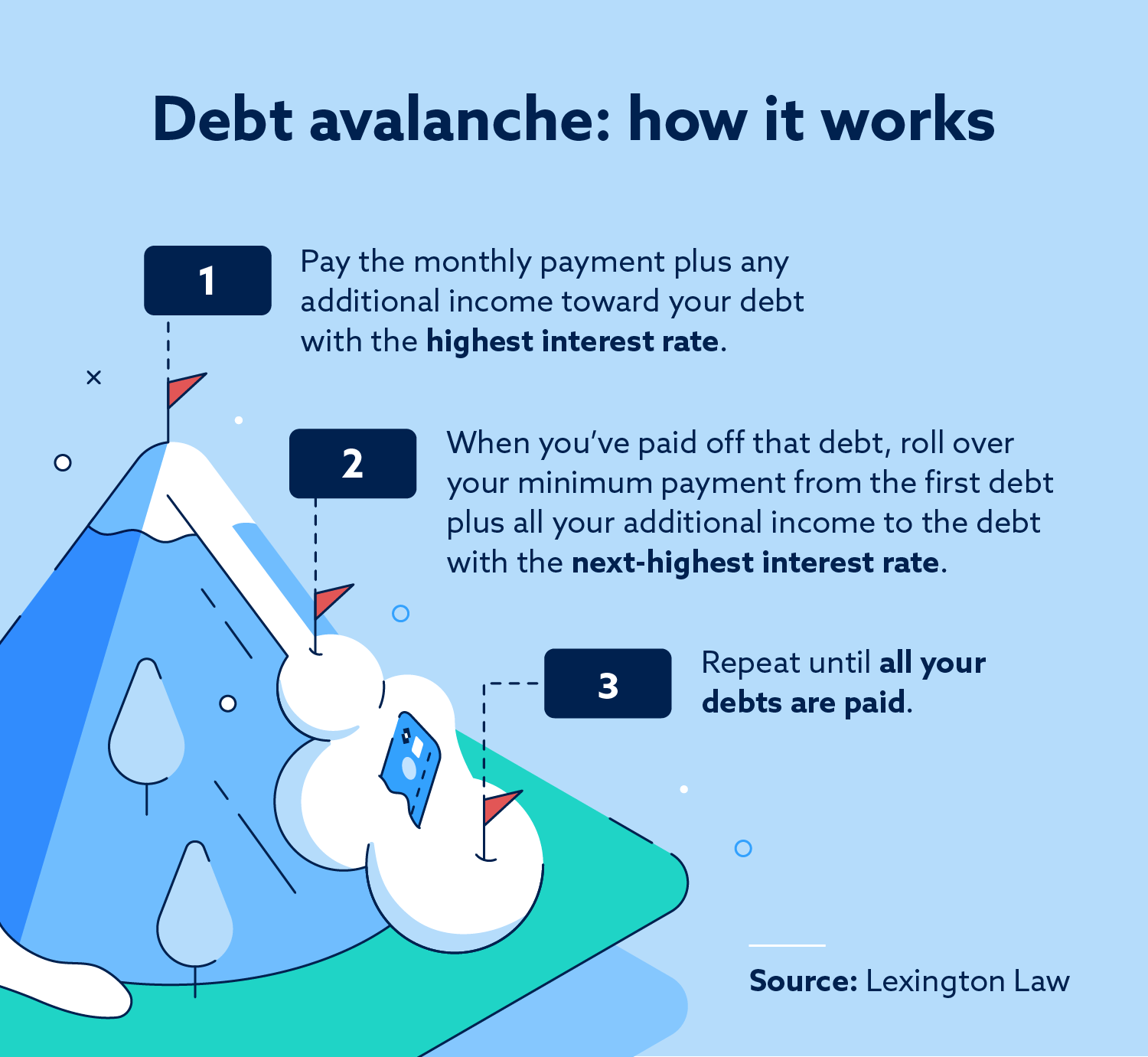

The debt avalanche methodology is an accelerated debt reimbursement technique that includes paying off the debt with the best curiosity first, then rolling these funds to your subsequent highest-interest debt till all of your debt is paid off.

Getting out of debt can appear overwhelming once you’re sitting at your kitchen desk making an attempt to pay payments every month or if debt collectors are harassing you. It’s even worse when all you possibly can take into consideration is every thing else you could possibly spend cash on: a household trip, a brand new automotive. However with a little bit of dedication and a plan, it’s potential to regain your monetary freedom with an accelerated debt reimbursement technique just like the debt avalanche methodology.

Learn on to discover ways to use the debt avalanche methodology to repay your debt quicker than you might have thought potential.

What’s the debt avalanche methodology?

The debt avalanche methodology is an accelerated debt reimbursement methodology. When utilizing this technique, you make minimal month-to-month funds on all of your money owed and put any further funds towards paying down the debt with the best rate of interest.

When you’ve repaid that debt, roll that minimal cost and extra funds over into the debt with the following highest rate of interest. Repeat the method till you’ve paid off all of your money owed.

The debt avalanche methodology is an effective technique for many kinds of debt:

- Pupil debt

- Bank card debt

- Auto loans

- Medical debt

Debt avalanche vs. debt snowball: What’s the distinction?

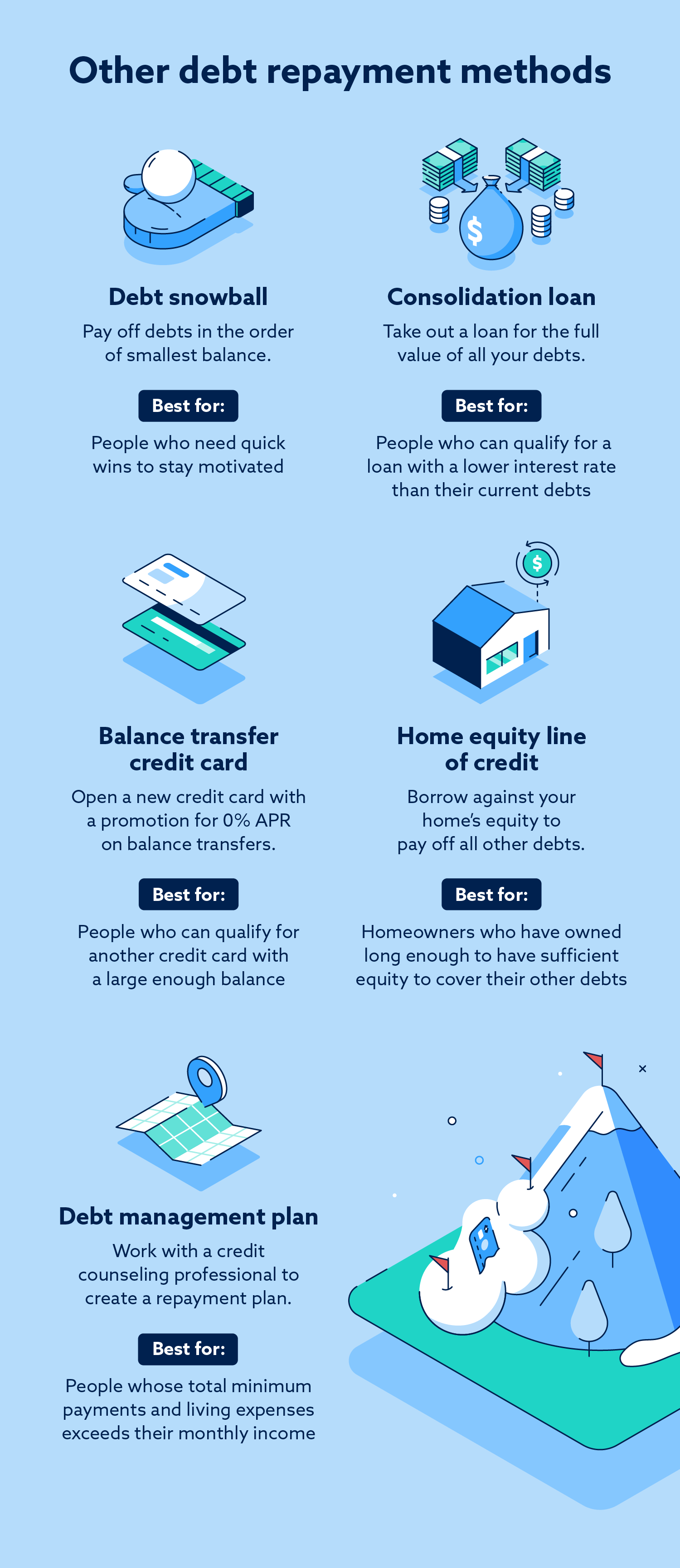

The debt avalanche is commonly in comparison with the debt snowball—one other accelerated debt reimbursement methodology. In a debt snowball, as a substitute of paying off the debt with the best rate of interest, you direct all of your more money towards paying off the debt with the bottom steadiness.

Whereas each strategies will repay debt quicker than should you had no technique, you’ll see extra fast wins should you go for the snowball methodology, making it a very good choice for people who find themselves simply discouraged.

You can even mix the 2 strategies by prioritizing paying off the smallest debt with the best rate of interest to save lots of on curiosity and see fast wins.

The best way to use the debt avalanche methodology to pay down debt

To make use of the debt avalanche methodology, observe these steps:

- Construct up an emergency fund. It will guarantee an surprising invoice doesn’t throw off your cost plan. Specialists advocate having sufficient in your emergency fund to cowl six months of residing bills.

- Make an inventory of all of your money owed. Embody their balances, rates of interest and minimal cost quantities. Set up your checklist from the best rate of interest to the bottom.

- Whole your month-to-month bills and earnings. Add up all the cash you spend on month-to-month residing bills and month-to-month minimal funds on debt. Additionally word your month-to-month earnings.

- Decide how a lot cash you must put towards further debt funds. Tally what you’ve got left over every month after paying month-to-month bills and minimal funds. You’ll put this “more money” towards debt every month.

- Every month, put the additional cash towards the debt with the best rate of interest. This ought to be along with the common month-to-month minimal funds.

- Put any surprising earnings towards the debt with the best rate of interest. When you get any surprising earnings, equivalent to a tax refund or bonus at work, put that towards your accelerated cost as effectively.

- Whenever you’ve paid that debt off, roll over that debt’s minimal cost and your additional month-to-month earnings towards the debt with the following highest rate of interest. Proceed paying the minimal cost on all different money owed.

- Repeat till you’ve cleared all of your money owed. As you repay money owed, your funds to the opposite money owed will improve.

Debt avalanche instance

Let’s have a look at an instance use of the debt avalanche methodology.

You will have three excellent money owed:

- A pupil mortgage for $10,000 with 5 p.c curiosity and a minimal month-to-month cost of $400

- A bank card debt of $5,000 with 25 p.c curiosity and a minimal month-to-month cost of $100

- A house restore mortgage for $3,000 with 15 p.c curiosity and a minimal month-to-month cost of $275

And after month-to-month residing bills and the three minimal funds, you’ve got $250 leftover in your finances to place towards accelerated funds.

Since your bank card debt has the best rate of interest, begin by paying the additional $250 along with the $100 month-to-month cost. Meaning you’ll pay $350 every month.

When you’ve paid off your bank card debt, your debt with the following highest rate of interest is the house restore mortgage, in order that’s the place you’ll begin sending your additional funds every month. Roll over the $350 you paid month-to-month for the credit score debt to the house restore mortgage. Added to the minimal cost of $275, you’ll pay $625 towards the mortgage every month.

When the house restore mortgage debt is obvious, focus in your pupil mortgage, which has the bottom rate of interest of your three money owed. Roll over the $625 you had been paying to the house restore mortgage to the minimal cost for the scholar mortgage, for a complete month-to-month cost of $1,025.

When you use the debt snowball methodology mentioned earlier, you’d begin by paying off your smallest debt, which on this case is the house restore mortgage.

Execs and cons of the debt avalanche methodology

The debt avalanche methodology is likely one of the most sensible and cost-effective debt reimbursement plans, however it isn’t excellent.

Some great benefits of the debt avalanche methodology are:

- You’ll save on curiosity. This methodology helps you repay your debt early, saving you what you’d have paid in curiosity.

- You’ll pay again your debt quicker. By steadily making funds bigger than the minimal, you possibly can shave months off your reimbursement plan.

The disadvantages of the debt avalanche methodology are:

- Bigger money owed can take longer to pay again. If you want small wins to remain motivated, this could negatively impression your capability to stay along with your accelerated cost plan.

- Sudden payments or unstable earnings can hinder your progress. This methodology solely works if you can also make common funds bigger than your minimal cost.

Different methods to repay bank card debt

Whereas many individuals discover the debt avalanche methodology to be a useful technique for getting out of debt, there are different methods to repay debt which will higher suit your state of affairs.

You can even use any of the next strategies:

- Stability switch bank card: Some bank cards have promotional presents for 0 p.c APR on steadiness transfers to new clients. When you qualify, you possibly can switch your debt on a high-interest bank card to certainly one of these playing cards. Take note of when the promotional 0 p.c APR ends, otherwise you’ll must pay curiosity once more. On this state of affairs, it makes essentially the most sense to commit any additional earnings after month-to-month bills to this debt to clear it quicker.

- Debt consolidation mortgage: Take out a mortgage for the quantity of all of your debt and use the cash to repay these particular person money owed. Then repay your consolidation mortgage every month. This makes reimbursement simpler since you’re solely making one month-to-month cost, however watch out that the rate of interest in your consolidation mortgage is lower than the rates of interest in your different debt. In any other case, you’ll find yourself paying extra in curiosity over time.

- House fairness line of credit score: Borrow in opposition to your own home’s fairness. Typically these strains of credit score have decrease rates of interest than bank cards.

- Debt administration plans: When you can not repay your debt inside 5 years even with a strict finances, or in case your complete month-to-month minimal funds are greater than your month-to-month earnings, take into account getting skilled assist. A debt counselor may help you create a debt administration plan to repay your debt. Nonetheless, secured debt (a debt with collateral, equivalent to your automotive or your own home) received’t qualify for a debt administration plan.

Is the debt avalanche methodology best for you?

The debt avalanche methodology is a superb choice for repaying debt quicker, however it doesn’t match each state of affairs. In case you are intent on saving cash when you repay debt and are motivated sufficient to maintain going with out small wins alongside the way in which, the debt avalanche methodology could also be your path to monetary freedom. Whereas utilizing the debt avalanche—or any accelerated debt reimbursement plan—it’s important to proceed with behaviors that preserve or enhance your credit score. Keep present on all of your payments, create and persist with a finances and monitor your spending. Lexington Regulation Agency could possibly allow you to in your journey to restore your credit score. Take our free credit score evaluation right this moment to study extra.

Notice: Articles have solely been reviewed by the indicated lawyer, not written by them. The data supplied on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for common informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained inside the web site don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.