{kind=link}

The knowledge supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

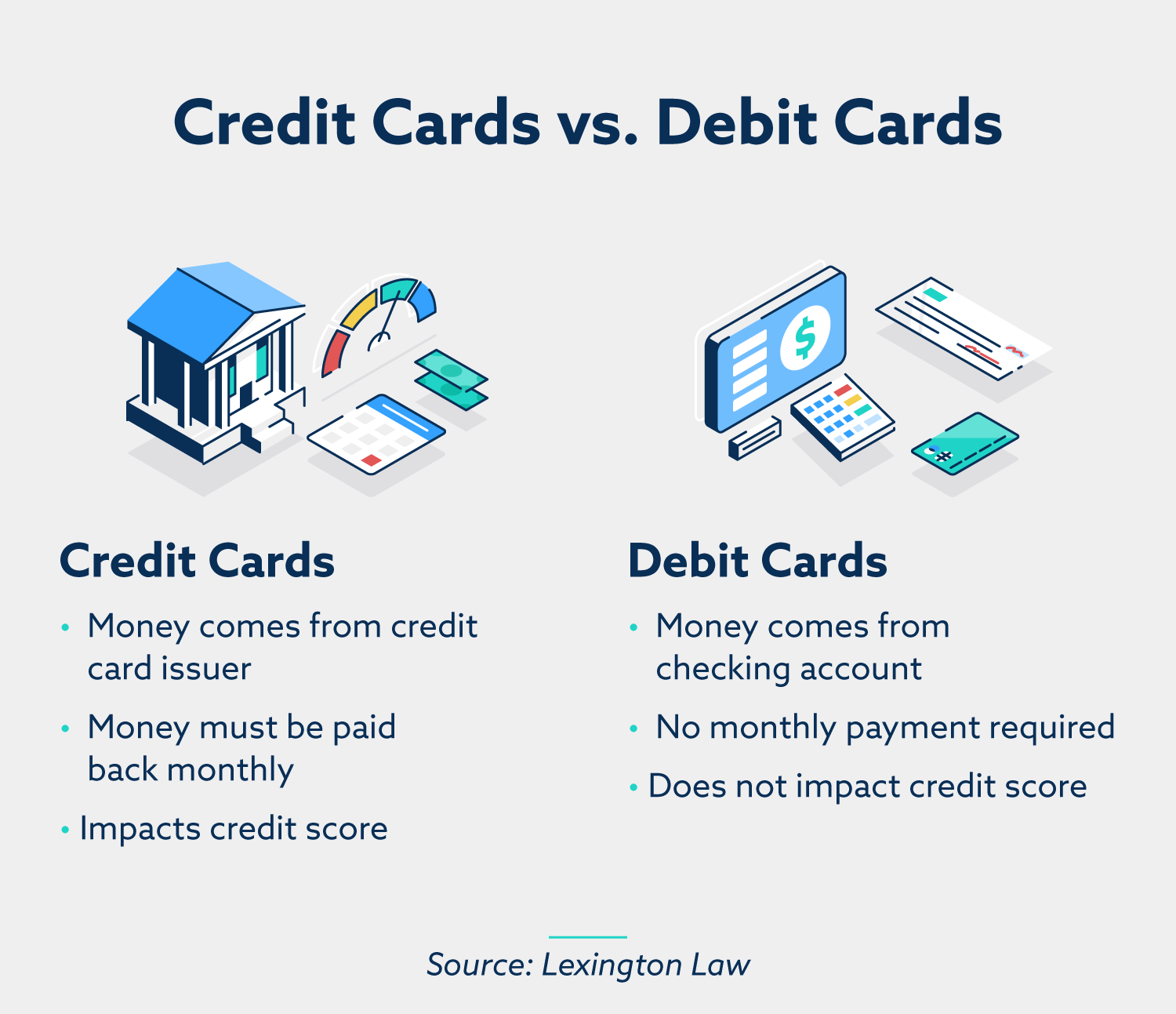

Debit playing cards use cash out of your checking account and haven’t any month-to-month fee or affect in your credit score rating. Bank cards use cash from a bank card issuer that have to be paid again month-to-month and can affect your credit score rating.

On the floor, debit and bank cards are an identical. Each have 16-digit card numbers, expiration dates and magnetic stripes. Each are handy methods to make purchases on-line and in shops. However past these similarities, debit and bank cards are two very various things.

Understanding the distinction between debit and credit score is a vital a part of monetary decision-making. With this data, you’ll be effectively outfitted to make the appropriate selections to your spending wants. Right here’s a fast information to the variations between debit and credit score.

What’s a debit card?

A debit card is a sort of fee card that’s linked to your checking account. If you make a purchase order, cash is deducted from the account in actual time. Debit playing cards are a handy solution to make use of cash out of your checking account with out having to hold money.

Most debit playing cards include low or no charges, however this is dependent upon your financial institution’s coverage. Sometimes, banks will cost a payment if the cardboard is used sometimes, if the checking account is under the minimal stability or in case your account has overdraft safety.

Debit playing cards additionally include various levels of fraud safety. In case your card is misplaced or stolen, most banks will cancel your card as quickly as they’re notified. If cash is stolen out of your account, making a declare will immediate your financial institution to research the matter, however this course of may be prolonged.

Easy methods to get a debit card

Debit playing cards are distributed instantly via your financial institution. To acquire one, you’ll first want to enroll in a checking account. This normally requires you to share some private info with the financial institution and deposit an preliminary stability.

After organising your checking account, your debit card ought to arrive within the mail. When you’ve activated it, you need to use it to make purchases in shops and on-line.

Debit card execs and cons

Debit playing cards are interesting to customers in some ways—above all, their practicality. They don’t include excessive rates of interest or annual membership charges. And since they use the funds already saved in your checking account, there’s no have to open a line of credit score. Plus, there’s the additional advantage of accessing the funds in your account with out withdrawing money from an ATM.

Nevertheless, relying by yourself checking account may also be a hindrance. If you have to make a purchase order however don’t have the funds prepared and ready, it’s possible you’ll not have the ability to full the transaction. And whereas many debit playing cards are outfitted with some type of fraud safety, it’s usually your duty to alert the financial institution of any suspicious exercise. In any other case, you will have hassle restoring stolen funds.

What’s a bank card?

A bank card is one other type of fee card issued by a monetary establishment, most frequently a financial institution. It provides the consumer entry to a line of credit score they will borrow from. As a cardholder, you conform to pay the borrowed funds again plus curiosity, however the actual phrases will fluctuate based on the financial institution’s phrases.

Bank cards typically include charges hooked up, each to make sure the establishment earnings from the deal and to cost the borrower for the cardboard’s advantages. These charges are measured via your annual share fee (APR), which clarifies the worth you pay every year to borrow cash.

For instance this, let’s say you might have an APR of 17.99 % and an excellent stability of $500. APR is calculated utilizing a every day periodic fee, which may be discovered by dividing the speed by 365—on this case, 0.00049. Multiplying this quantity by your present stability brings your every day periodic fee to $0.25, which might add as much as fairly a bit in the event you constantly have an excellent stability.

Bank cards additionally include built-in card safety. Uncommon exercise might trigger your card to freeze till you manually approve the transactions, a helpful security internet towards theft. As with debit playing cards, it’s as much as you to alert the corporate if unfamiliar exercise seems in your account.

Easy methods to get a bank card

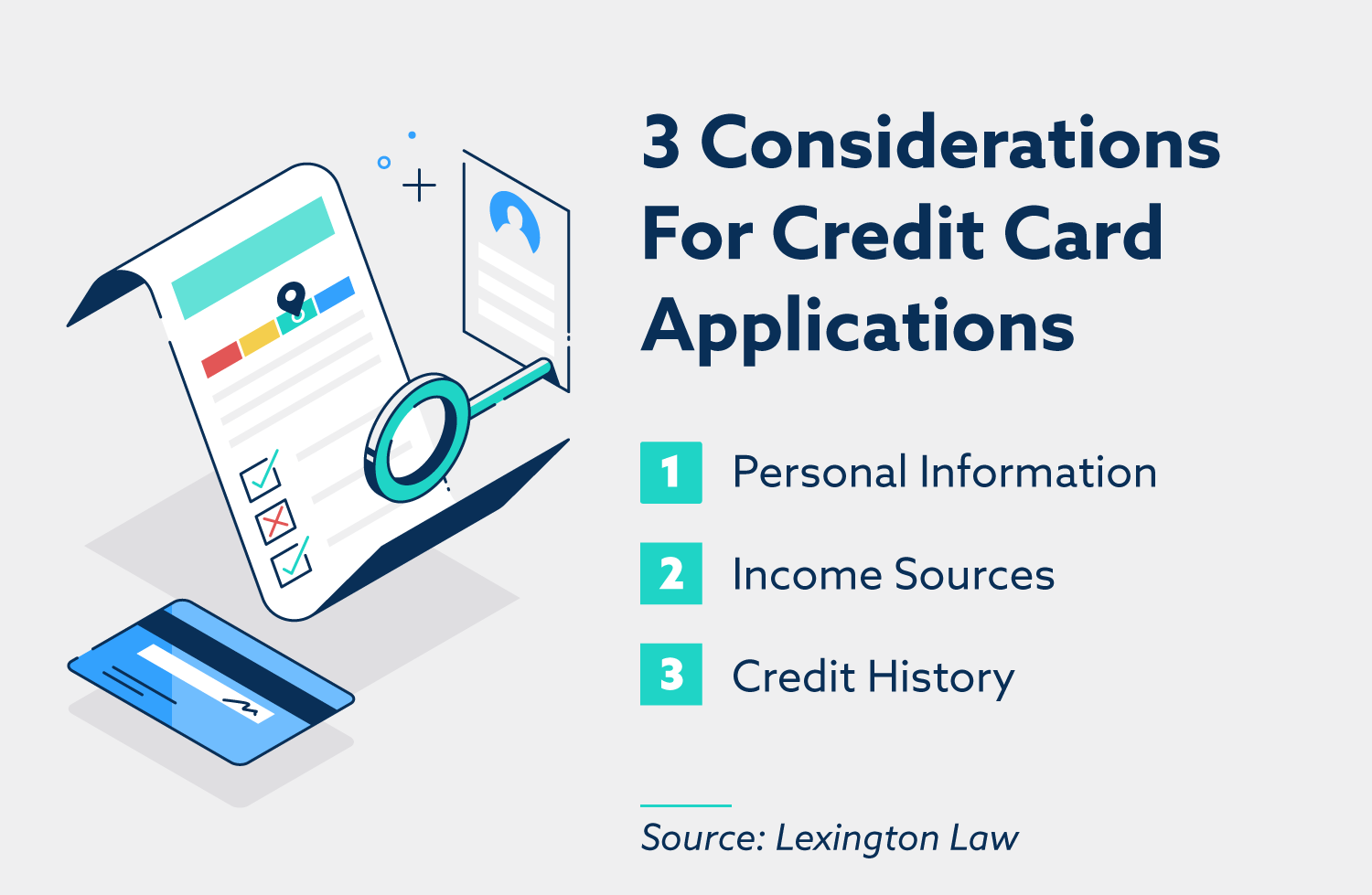

Bank cards aren’t hooked up to your checking account and have to be utilized for. If you apply for a bank card, you’ll be requested to offer some private info, together with particulars about your revenue and credit score historical past. Lenders use this data to foretell what sort of borrower you’ll be and assess the chance they’ll assume by lending to you.

A wide range of components will affect your possibilities of being accredited for a bank card. These embrace:

- Credit score historical past or lack thereof

- Credit score rating

- Cost historical past

- Earnings

- Excellent mortgage balances

- Employment historical past

As a result of lenders need to make sure you’ll have the ability to repay what you borrow, something that will increase your danger as a cardholder can decrease your probability of approval. This implies a poor credit score rating, historical past of missed funds and low revenue can all affect the choice.

In case your software is rejected, you may at all times apply for a unique card. Nevertheless, it’s a good suggestion to attend a bit earlier than reapplying, as too many exhausting credit score inquiries can injury your credit score rating. Whilst you wait, think about addressing the components that led to the rejection within the first place, both by paying your excellent stability or discovering a credit score restore service.

Bank card execs and cons

Bank cards can turn out to be useful as they remove the necessity to pay up entrance. That is particularly helpful for bigger purchases that may take a good portion of your checking account. Many bank cards additionally accumulate rewards and factors as you spend. These may be redeemed for reductions, money again and even journey perks. And bank cards are one of many best methods to construct good credit score. Making common funds and holding your credit score utilization fee low can assist your credit score over time.

As a result of your bank card makes use of funds borrowed from the financial institution, the financial institution has a better curiosity within the card’s safety than it could for a debit card, which makes use of cash that belongs to you. Authorities laws just like the Honest Credit score Billing Act imply you’ll be responsible for few or no fraudulent transactions that happen within the occasion your card is stolen.

However bank cards may also be a double-edged sword. Simply as they will enhance your credit score, they will additionally decrease it via missed funds and excessive excellent balances. That is very true whenever you’re managing a number of playing cards, as it may be simple to spend an excessive amount of with out with the ability to rapidly pay it again. And with rates of interest and charges to maintain observe of, bank cards may be fairly costly to make use of.

Debit, credit score and your credit score rating

Debit playing cards typically don’t have a lot impact in your credit score rating. As a result of the cash in use already belongs to you, there’s no credit-related exercise going down. Exceptions can happen, corresponding to within the case of unpaid overdraft charges. If these go unpaid for too lengthy, they’ll be reported to credit score bureaus.

Bank cards, then again, can have a big affect in your credit score. Basically, all the things you do along with your bank card can have an effect on it, both positively or negatively.

Some of the widespread influencing components is a historical past of creating late funds—or skipping them altogether. Cost historical past impacts an estimated 35 % of your FICO® credit score rating, that means even a couple of missed funds may cause a shift. This may increasingly additionally scale back your probability of being accredited for any new playing cards, as lenders may even see this historical past as a danger. A excessive credit score utilization ratio can have the same impact. A very good rule of thumb is to maintain this quantity under 30 % of your spending restrict.

It’s widespread for folks to have a mixture of debit and bank cards of their wallets, however the appropriate mix will rely by yourself wants and targets. Should you’re trying to enhance or set up your credit score historical past, making use of for a bank card may be a good suggestion. But when you have already got a handful of playing cards and are having hassle managing all of them, specializing in credit score restore is probably going a greater choice.

The distinction between debit and credit score, defined

Each debit and bank cards are helpful instruments to have in your monetary repertoire. Realizing when to make use of each can assist you make sensible spending choices and construct higher cash administration habits. Listed here are a couple of key takeaways to remember as you navigate your personal debit and credit score use:

- You’ll be able to receive a debit card via any financial institution the place you might have a checking account. Bank cards have to be utilized for, and approval is granted primarily based on an evaluation of your monetary historical past.

- Debit playing cards are linked to your checking account, whereas bank cards make the most of borrowed funds issued by a monetary establishment.

- Debit playing cards normally haven’t any impact in your credit score, whereas bank cards can have an effect on it considerably.

Wish to study extra about managing your credit score? Our staff at Lexington Legislation is right here to assist. Take our free credit score evaluation immediately to test your report and begin attaining your credit score targets.

Notice: Articles have solely been reviewed by the indicated lawyer, not written by them. The knowledge supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained inside the website don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.