{kind=link}

Whatever has actually been turning up roses for home mortgage prices in 2026, however that can quickly alter if the Greenland circumstance spirals out of hand.

Presently, 30-year set home mortgage prices are floating around 6%, which is essentially a three-year reduced.

That brought about a rise in mortgage applications recently, with both existing home owners wanting to refi and possible home customers entering.

Paradoxically, Head of state Trump’s newest proposition to get $200 billion in mortgage-backed safeties (MEGABYTESES) obtained us there.

However his newest danger to enforce brand-new tolls on various European nations can send out home mortgage prices greater once more.

New 10% Tariffs Threatened If Greenland Can’t Be Acquired by the U.S.

You’ve most likely come across the hazards to take Greenland from Denmark, with Trump drifting a brand-new round of tolls if they don’t consent to a sale.

In a Fact Social message, he claimed, “Beginning on February 1st, 2026, every one of the above stated Nations (Denmark, Norway, Sweden, France, Germany, The UK, The Netherlands, and Finland), will certainly be billed a 10% Toll on any type of and all items sent out to the USA of America.”

“On June 1st, 2026, the Toll will certainly be enhanced to 25%.”

This remains in recommendation to the abovementioned nations checking out Greenland “for objectives unidentified” and hampering a sale to the USA.

Trump has actually suggested that the acquisition of Greenland is critical for “Safety and security, Protection, and Survival of our Earth.”

Which nations like “China and Russia desire Greenland, and there is nothing that Denmark can do concerning it.”

Lengthy tale short, Trump intends to get Greenland and if Denmark and its evident European allies stand in the means, a brand-new round of tolls will certainly be released.

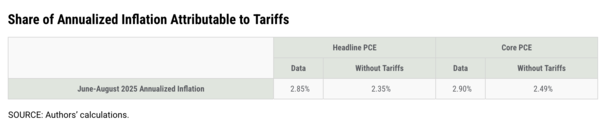

While we can say whether tolls trigger rising cost of living till the cows get back, the St. Louis Fed set out a respectable instance.

Per the St. Louis Fed, “Over the June-August 2025 duration, tolls describe approximately 0.5 percent factors of heading PCE annualized rising cost of living and around 0.4 percent factors of core PCE annualized rising cost of living.”

As well as Fed chair Powell claimed last summer season that they weren’t able to reduce prices as openly as feasible as a result of the unidentified influences of the tolls.

So whether you think tolls trigger rising cost of living or otherwise, there’s a respectable disagreement they maintain rate of interest more than they may or else be (CPI vs. home mortgage prices).

Home Mortgage Prices Don’t Exist in a Vacuum Cleaner

Concerning a year earlier, we saw home mortgage prices take place a rollercoaster adventure many thanks to the on-again, off-again tolls.

However they were perhaps stuck at greater degrees as a result of tolls or the danger of brand-new tolls.

We saw the 30-year set climb over 7% on numerous celebrations in 2015, resulting in one more depressing year for home sales.

When a great deal of that talk started to subside, and rising cost of living information remained to cool down, home mortgage prices started relocating reduced.

Today, they’re about one complete percent factor listed below those year-ago degrees, however that’s in component as a result of getting worse labor (tasks records) and probably a lot of Trump’s plans currently baked in.

And as stated, the most recent proposition for Fannie and Freddie to get billions in megabytes to reduced home mortgage price spreads.

Nevertheless, home mortgage prices don’t exist in a vacuum cleaner and the MBS offer can be totally eclipsed by this brand-new toll danger.

As the St. Louis Fed kept in mind, tolls accounted “for a purposeful share of current rising cost of living.”

The danger of brand-new tolls (and bigger ones) suggests rising cost of living quotes can obtain dirty and the Fed may draw back on extra price cuts.

In the meanwhile, 10-year bond returns can relocate higher on the unpredictability, pressing the 30-year repaired greater at the same time.

The valuable results of the MBS purchasing can be totally soaked up and we can see home mortgage prices climbing up back right into the sixes as opposed to dropping much deeper right into the fives.

As I’ve claimed often times, this would certainly be yet one more gut-punch for possible home customers (and vendors) and the real estate market at big.

So with any luck we obtain some clearness on this circumstance ASAP to prevent wrecking yet one more springtime real estate market.

(picture: David Stanley)

Prior to producing this website, I functioned as an account exec for a wholesale home mortgage lending institution in Los Angeles. My hands-on experience in the very early 2000s influenced me to start covering home mortgages 19 years ago to aid possible (and existing) home customers much better browse the mortgage procedure. Follow me on X for warm takes.