{kind=link}

Full the 2 fields in our HELOC calculator under to see how a lot you’ll be able to borrow towards your own home. Estimates are primarily based on the house’s present market worth, your excellent mortgage stability, and the loan-to-value ratio, or LTV.

Who Ought to Use This Calculator

Use this calculator if you need to see how a lot you’ll be able to borrow with a House Fairness Line of Credit score (HELOC).

This isn’t the identical as a House Fairness Mortgage. See: HELOC Vs HELOAN.

This is not going to calculate your month-to-month fee, or the ultimate price of the mortgage.

Right here’s a better take a look at how a HELOC calculator estimates how a lot you’re allowed to borrow towards your own home fairness.

4 Numbers to Know for Calculating Your HELOC Quantity

There are just a few numbers and ideas you need to perceive to have a full image of what this calculator considers when predicting how a lot cash you will get with a HELOC. These embrace your house worth, mortgage stability, credit score rating, and extra. Let’s dive into the 4 numbers it’s good to perceive when calculating your HELOC quantity.

1. House Fairness

Your property’s fairness is the distinction between the worth of your own home and your mortgage stability. As an example, let’s say your own home is value $300,000 and also you owe $140,000 in your mortgage. Meaning you could have $60,000 in house fairness. It’s the portion of the house’s present worth that you just–the home-owner–personal outright. The much less you owe in your mortgage, the extra fairness you’ll have.

Your property fairness additionally modifications as market values fluctuate. As your own home worth will increase, so does your fairness. If your own home worth decreases, your fairness might also – if the worth is dropping sooner than you’re paying down your mortgage stability.

2. Mortgage Stability

As a house owner, you probably already know that your mortgage stability is the total quantity owed at any time all through the period of your mortgage. As we talked about above, your own home fairness is decided by deducting your mortgage stability from your own home’s present market worth.

Paying down your mortgage is finished by month-to-month funds. The month-to-month fee pays down the principal stability and curiosity. In different phrases, with every mortgage fee, you’re decreasing the quantity you owe on the principal, which helps you construct fairness.

Your mortgage, or the cash you owe on your own home, performs a lead position in figuring out your own home fairness and your estimated HELOC line quantity and charges.

3. Mortgage-to-Worth Ratio

Your Mortgage-to-Worth Ratio, or LTV, describes the quantity you’ll be able to borrow in comparison with the worth of the property securing the mortgage. To search out this quantity, expressed as a share, you’ll divide your mortgage mortgage stability (i.e. what you continue to owe in your mortgage) by your property’s present market worth. This offers lenders an concept of the danger concerned in lending to you. As an example, a house bought for $400,000 with a $300,000 mortgage ends in a LTV ratio of 75%.

Lenders wish to see decrease LTVs, because it signifies a decrease threat in lending. When utilizing a HELOC calculator, the LTV ratio provides lenders an concept of the utmost quantity you’ll be able to borrow primarily based on your own home’s worth.

4. Credit score Rating

Your credit score rating is likely one of the most vital numbers in your monetary life. A credit score rating is a 3-digit quantity, falling on a scale from 300 to 850, which summarizes your credit score historical past and represents your monetary monitor document. It’s mainly a report card for a way you’ve dealt with funds up to now – and it’ll inform potential lenders on the dangers of lending to you sooner or later.

There are lots of components that go into figuring out your credit score rating. Your fee historical past, credit score inquiries, and the share of credit score restrict used all play a job. Usually, a credit score rating at or above 740 is taken into account superb or distinctive, whereas a rating under 670 is taken into account poor. Scores at or above 670 are typically thought-about good. Your credit score rating is a significant factor in figuring out your eligibility for any kind of mortgage or credit score line, particularly a HELOC.

A wholesome credit score rating is a key side of a wholesome monetary life – and can play an influential position in your skill to safe a HELOC.

Utilizing a HELOC Calculator to Estimate Your Line of Credit score

When you’ve bought these numbers found out, you can begin calculating your estimated HELOC quantity. This HELOC calculator helps decide the quantity you’ll be able to borrow with a House Fairness Line of Credit score, which usually ranges wherever from $50,000 to $500,000.

Needless to say lenders usually received’t allow you to faucet into your own home fairness in the event you owe greater than 90% of what your own home is value.

How a lot can I borrow with a HELOC?

You’ll probably be capable of entry as much as 90% of your own home’s worth minus your present mortgage stability, so preserve this in thoughts in the course of the calculation course of.

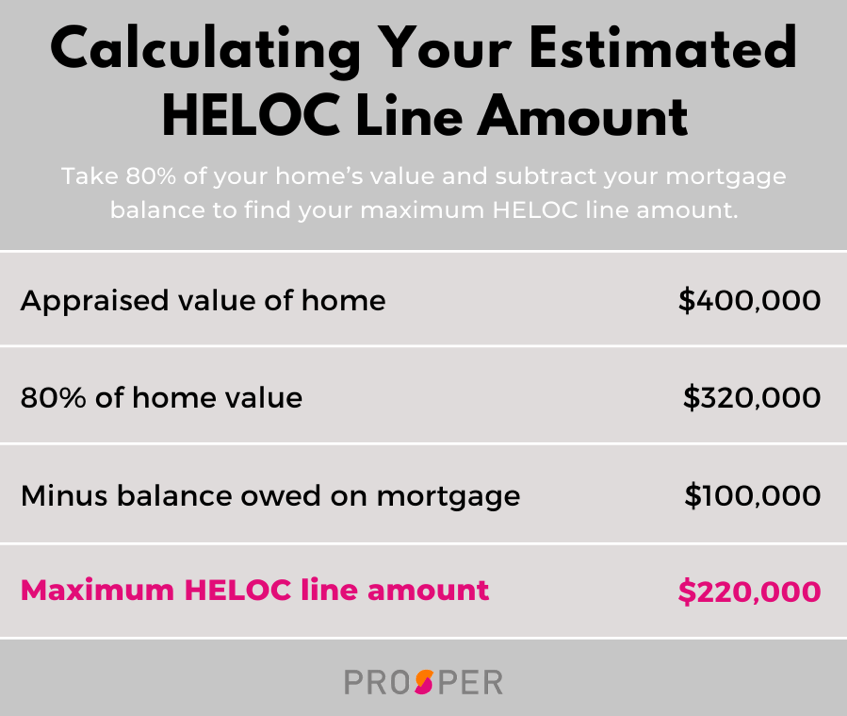

Right here’s an instance:

Let’s say your own home is value $400,000, and also you owe $100,000 in your mortgage stability. Your lender says you’ll be able to borrow as much as 90% of your own home’s worth – which on this case is $320,000 Subtract that $100k you owe in your mortgage, and also you’ve bought your estimated most HELOC line quantity. Right here’s a visible chart to assist break it down.

Paying Off Your HELOC

As soon as the lender approves your HELOC, you’ll be able to faucet into your complete credit score line quantity by borrowing as wanted. Very similar to a bank card, you should use the HELOC whenever you want it and repay the stability month-to-month (with curiosity). HELOC rates of interest are often variable, however you may as well discuss to your lender concerning the possibility of a fixed-rate. HELOCs are usually cut up into two phrases – the draw interval and the reimbursement interval – for month-to-month funds.

In the course of the draw interval, which usually lasts as much as 10 years, you’ll be able to entry your line of credit score as wanted whereas making versatile month-to-month funds. When you may need the choice to solely pay again the curiosity on what you’ve borrowed in the course of the draw interval, in the event you make principal and curiosity funds throughout this time, your fee quantity in the course of the reimbursement interval will probably be smaller.

In the course of the reimbursement interval, which usually lasts wherever from 10 to twenty years, you’ll need to pay again each curiosity and the principal stability and also you’ll now not be capable of borrow out of your HELOC. Meaning your common month-to-month fee could also be bigger than your typical funds in the course of the draw interval since you must embrace the principal stability. That’s why many lenders suggest paying greater than the minimal quantity in the course of the draw interval to keep away from fee shock in a while.

You’re off to a superb begin.

When speaking to a lender a few HELOC, it’s good to go in with a baseline information of the place you stand by way of your own home worth, mortgage stability, LTV, and credit score rating. Whereas lenders can information you on which kinds of loans and contours of credit score are greatest in your state of affairs, utilizing a HELOC calculator provides you a head begin in making the most effective choice in your monetary life. Talking of lenders, right here’s the whole lot it’s good to find out about HELOCs with Prosper.

IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT.

To assist the federal government battle the funding of terrorism and cash laundering actions, Federal regulation requires all monetary establishments to acquire, confirm, and document info that identifies every one who opens an account.

What this implies for you: While you open an account, we’ll ask in your title, handle, date of beginning, and different info that can permit us to determine you. We might also ask to see your driver’s license or different figuring out paperwork.

Eligibility for a house fairness mortgage or HELOC as much as $500,000 depends upon the knowledge offered within the house fairness utility. Loans above $250,000 require an in-home appraisal and title insurance coverage. For HELOCs debtors should take an preliminary draw of $50,000 at closing. Subsequent HELOC attracts are prohibited in the course of the first 90 days following closing. After the primary 90 days following closing, subsequent HELOC attracts have to be $1,000 or extra (not relevant in Texas).

The time it takes to get money is measured from the time the Lending Accomplice receives all paperwork requested from the applicant and assumes the applicant’s said revenue, property and title info offered within the mortgage utility matches the requested paperwork and any supporting info. Spring EQ debtors get their money on common in 26 days. The time interval calculation to get money is predicated on the primary 6 months of 2022 mortgage fundings, assumes the funds are wired, excludes weekends, and excludes the government-mandated disclosure ready interval. The period of time it takes to get money will fluctuate relying on the applicant’s respective monetary circumstances and the Lending Accomplice’s present quantity of purposes.

Spring EQ can’t use a borrower’s house fairness funds to pay (partly or in full) Spring EQ non-homestead debt at account opening. For HELOCs in Texas, the minimal draw quantity is $4,000. To entry HELOC funds, borrower should request comfort checks.

Rates of interest could also be adjusted primarily based on components associated to the applicant’s credit score profile, revenue and debt ratios, the presence of current liens towards and the placement of the topic property, the occupancy standing of the topic property, in addition to the preliminary draw quantity taken on the time of closing. Communicate to a Prosper Agent for particulars.

Certified candidates could borrow as much as 95% of their major house’s worth (not relevant in Texas) and as much as 90% of the worth of a second house. House fairness mortgage candidates could borrow as much as 85% of the worth of an funding property (not relevant for HELOCs).

All house fairness merchandise are underwritten and issued by Spring EQ, LLC, an Equal Housing Lender. NMLS #1464945.

Prosper Market NMLS Prosper Market, Inc. NMLS# 111473

Licensing & Disclosures | NMLS Client Entry

Prosper Funding LLC

221 Principal Road, Suite 300 | San Francisco, CA 94105

6860 North Dallas Parkway, Suite 200 | Plano, TX 75024

© 2005-2022 Prosper Funding LLC. All rights reserved.

Learn extra

IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT.

To assist the federal government battle the funding of terrorism and cash laundering actions, Federal regulation requires all monetary establishments to acquire, confirm, and document info that identifies every one who opens an account.

What this implies for you: While you open an account, we’ll ask in your title, handle, date of beginning, and different info that can permit us to determine you. We might also ask to see your driver’s license or different figuring out paperwork.

Eligibility for a house fairness mortgage or HELOC as much as $500,000 depends upon the knowledge offered within the house fairness utility. Loans above $250,000 require an in-home appraisal and title insurance coverage. For HELOCs debtors should take an preliminary draw of $50,000 at closing. Subsequent HELOC attracts are prohibited in the course of the first 90 days following closing. After the primary 90 days following closing, subsequent HELOC attracts have to be $1,000 or extra (not relevant in Texas).

The time it takes to get money is measured from the time the Lending Accomplice receives all paperwork requested from the applicant and assumes the applicant’s said revenue, property and title info offered within the mortgage utility matches the requested paperwork and any supporting info. Spring EQ debtors get their money on common in 26 days. The time interval calculation to get money is predicated on the primary 6 months of 2022 mortgage fundings, assumes the funds are wired, excludes weekends, and excludes the government-mandated disclosure ready interval. The period of time it takes to get money will fluctuate relying on the applicant’s respective monetary circumstances and the Lending Accomplice’s present quantity of purposes.

Spring EQ can’t use a borrower’s house fairness funds to pay (partly or in full) Spring EQ non-homestead debt at account opening. For HELOCs in Texas, the minimal draw quantity is $4,000. To entry HELOC funds, borrower should request comfort checks.

Rates of interest could also be adjusted primarily based on components associated to the applicant’s credit score profile, revenue and debt ratios, the presence of current liens towards and the placement of the topic property, the occupancy standing of the topic property, in addition to the preliminary draw quantity taken on the time of closing. Communicate to a Prosper Agent for particulars.

Certified candidates could borrow as much as 95% of their major house’s worth (not relevant in Texas) and as much as 90% of the worth of a second house. House fairness mortgage candidates could borrow as much as 85% of the worth of an funding property (not relevant for HELOCs).

All house fairness merchandise are underwritten and issued by Spring EQ, LLC, an Equal Housing Lender. NMLS #1464945.

Prosper Market NMLS Prosper Market, Inc. NMLS# 111473

Licensing & Disclosures | NMLS Client Entry

Prosper Funding LLC

221 Principal Road, Suite 300 | San Francisco, CA 94105

6860 North Dallas Parkway, Suite 200 | Plano, TX 75024

© 2005-2022 Prosper Funding LLC. All rights reserved.