{kind=link}

Home Loan Q&A: “Does Having A Home Loan Aid Your Credit Rating?”

If you have actually ever before drawn your credit history record and/or seen your ratings, you might have discovered that the absence of a home mortgage might really be holding you back from credit history excellence.

Also if you currently have an apparently excellent credit history, the credit history record “notes” might indicate that an installation account like a home mortgage would certainly better boost your ratings.

However prior to you go out and also obtain a home mortgage, it is very important to explain that the effect might not be considerable, and also you absolutely should not secure of a home mortgage for your credit report.

That would certainly appear silly.

You Can Increase Your Credit Rating By Improving Your Credit Report Mix

So, why would certainly the visibility of a home mortgage assist your credit rating anyhow? You’re handling all that brand-new financial debt. Does not that make you riskier? What provides?

Well, besides the huge heap of brand-new financial debt, when you secure a home mortgage you basically inform potential lenders that you have actually made an extremely severe monetary and also way of living dedication. Yep, you’re a grownup currently.

And also most home loans have finance terms of three decades, so you’re not going anywhere quick.

[30-year vs. 15-year mortgages]

With a home mortgage, you instantly include security to your credit report account, which is absolutely a good idea.

In addition to that, home loans likewise have a tendency to find in really high dollar-amounts, unlike bank card or car loans/leases.

Rather than obtaining a $10,000 credit limit, you’re possibly considering a six-figure buck quantity, which recommends that you were creditworthy to start with to get the mortgage.

This indicates you have a constant work, some properties in the financial institution, excellent FICO ratings, etc.

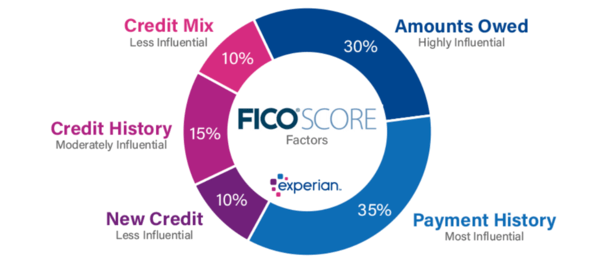

FICO, the designer of the FICO rating, really takes into consideration “ credit report mix” as component of their racking up formula, and also it represents 10% of your general rating.

So if your credit report contains bank card just, your FICO rating will certainly experience, or at the very least not flourish as it should.

Once again, it might still be excellent or perhaps “outstanding” theoretically, yet without a home mortgage behind it, you are viewed as rather one-dimensional.

Your Credit Report Record Is Your Résumé

Think about your credit history record like an individual résumé. Yeah, I made use of the accents. Rather than work background, it’s your credit report.

You desire it to be excellent? You wish to reveal feasible lenders you have actually obtained some severe experience, not simply an entry-level work.

Hell, any person can handle a couple of bank card throughout the years, yet those that can take care of a high-dollar home mortgage show a whole lot even more duty.

Why? Since the month-to-month settlements are commonly a lot greater than any type of various other credit line. And also homeownership alone is a signal of reliability.

If you can round up the settlement monthly for many years after year, it reveals you have actually finished past taking care of a meager bank card or 2.

As kept in mind, the finance regard to three decades (in many cases) indicates you raise the size of your credit report gradually.

As Well As if you’re likewise paying for various other financial debts and also bank card monthly, you’re basically a credit rating super star.

For these factors, a home mortgage might really boost your credit history, though there’s no quick and also difficult number.

Exactly How a Home Mortgage Can Pain Your Credit Rating

Prior to we obtain also thrilled concerning the credit report score-boosting possibility of a home mortgage, make note that it’s not simply a one-way road. The visibility of such a huge finance might really decrease your credit history originally if you consider the credit report questions

and also the brand-new financial debt. And also the reality that you have not yet revealed the capacity to handle it. Put simply, you’re even more of a credit history threat than you were previously since you currently owe a financial institution or finance servicer

thousands upon hundreds of bucks, and also might have exhausted on your own to some extent.

If you incorporate this brand-new credit line with, probably, a brand-new bank card or 2 (to purchase furnishings or devices), your ratings might experience.

Furthermore, if you miss out on a home mortgage settlement, anticipate it to be substantially even worse than missing out on a charge card settlement. If you want to obtain one more home mortgage or re-finance your residence finance in the future, And also possibly destructive. A while back, FICO did some

study

to identify exactly how brand-new home loans influenced customers’ credit rating.

They recognized concerning 2.8 million customers with a newly-opened home mortgage in between May 2017 and also July 2017.

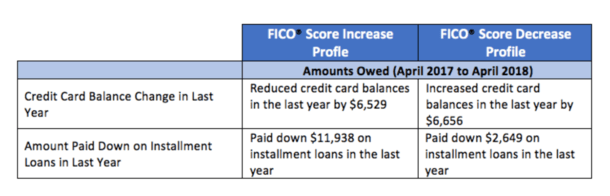

Of those, 12% experienced a considerable boost in their FICO rating in between April 2017 and also April 2018, while 11% of customers had a considerable reduction.

They specified “substantial” as a 40+ factor modification in rating. Relocating up from 700 to 740, or going down from 700 to 660. The staying 77% of customers “had a reasonably secure rating modification,” specified as much less than 40 factors in between both amount of time. Regarding why there was a lot aberration, it resulted from

general credit report actions

Your home mortgage does not exist in a vacuum cleaner, and also thus your gas mileage might differ.

Simply put, those that saw ratings rise lowered bank card equilibriums, paid for installment fundings, and also stayed clear of late settlements.

Alternatively, those that saw their ratings decline did the contrary. And also it might have had absolutely nothing to do with the home mortgage, at the very least straight. FICO’s guidance for those that open up brand-new home loans coincides as it is for any person else: pay costs promptly, lower impressive equilibriums, and also obtain brand-new credit report just when needed. If you’re a

newbie residence purchaser

, be particularly cautious not to exhaust on your own. Obtain made use of to the lots of brand-new costs you’ll need to pay monthly!

Those that saw their ratings go down substantially after obtaining a brand-new home mortgage possibly attacked off greater than they might eat.

Home Mortgages Can Strengthen Your Credit Rating In Time Currently fortunately. Gradually, the visibility of a home mortgage need to strengthen your credit rating and also make you exceptionally eye-catching to brand-new lenders. If you make on-time

home mortgage settlements monthly, your ratings will certainly increase and also you’ll likewise confirm that you can handle the biggest quantities of financial debt tossed your method. This indicates you’ll have a a lot easier time acquiring succeeding home loans in the future, or

re-financing your existing mortgage

, at the very least when it come to your credit report.

And also smaller sized fundings, like car fundings and also bank card, will certainly be simpler to get since lenders will certainly have recorded proof that you can take care of the biggest fundings around.

With a home mortgage in the mix and also paid as concurred, your FICO rating need to tick greater and also greater as even more on-time settlements are made.

At the end of the day, a home mortgage isn’t mosting likely to totally make or damage your credit history, yet it can absolutely offer you a little added press.

Alternatively, if you take place to miss out on a home mortgage settlement, plan for a massive decrease in your credit history and also a lot more difficulty if you maintain missing out on settlements.(*) Keep in mind, a home mortgage is an advantage, and also you have to be liable, or birth some rather severe effects.(*)