{kind=link}

It’s time for an additional home mortgage match, the most up to date installation “ home mortgage prices vs. economic crises“

This is a prompt blog post seeing that home mortgage prices have actually gone definitely bonkers recently as well as broach an additional economic crisis are warming up.

The Fed produced an extremely accommodative financial plan over the previous years using Measurable Easing (QE), which pressed home mortgage prices to videotape lows.

However that (integrated with COVID-19 as well as war-related supply chain problems) at some point activated unpleasant rising cost of living, requiring the Fed to act boldy the various other method, which might lead to an economic downturn at some time quickly.

The inquiry is does an economic downturn hint reduced home mortgage prices, greater home mortgage prices, or absolutely nothing whatsoever?

Home Mortgage Prices Usually Autumn Throughout Economic Crises

First Of All, an economic downturn is specified as “a considerable decrease in financial task that is spread out throughout the economic climate which lasts greater than a couple of months,” per the National Bureau of Economic Research Study (NBER).

In easy terms, this suggests a declining economic climate rather than an expanding economic climate for a continual amount of time.

This might be shown by a tightening in the gdp (GDP) over successive quarters.

Primarily, customers suppress investing, firms outcome much less item, discharges occur, and so forth. The vibrant changes from gravy train spenders to thrifty savers.

As kept in mind, the Fed crafted reduced rates of interest using QE. They bought numerous billions in Treasuries as well as firm mortgage-backed safeties (MEGABYTESES) to improve liquidity as well as motivate borrowing.

This ended up being terrific for the home mortgage market, as rates of interest was up to the most affordable degrees on document.

The 30-year set hit a mouthwatering low of 2.65% in very early 2021, while the 15-year repaired went down to 2.10% later on that year.

We understand good ideas never ever last as well as need to at some point concern an end. As well as currently we could be paying the cost for all those excellent years.

[Does the Fed Control Mortgage Rates?]

The Fed Is Raising Fees to Battle Rising Cost Of Living, However Might Need To Lower Them Right After

All the gravy train over the last numerous years brought about significant rising cost of living as well as the Fed is currently on the offensive, despite the fact that it could be far too late to prevent a significant decline.

They have actually been hard at the workplace dealing with rising cost of living by increasing the target government funds price as well as lowering their inflamed annual report.

Rather than acquiring Treasuries as well as MBS, they’re currently allowing them escape. As well as they might at some point offer MBS outright, which might flooding the currently weak market.

Put simply, with the Fed not a customer, as well as even worse a vendor, supply rises.

Unless need increases in some way, the cost of the bonds drops as well as the return needs to turn up.

This converts to greater rates of interest for customers on points like mortgage, car car loans, etc.

This is made worse when rising cost of living assumptions are high, providing a one-two strike to home mortgage prices.

Currently if the Fed maintains increasing prices as well as discharging its annual report, there’s a possibility of an economic downturn.

It’s unclear when this would certainly occur, though 2023 might be the year.

If it takes place, the Fed might be required to reduce its target fed funds price to promote development as well as obtain the economic climate downing once again.

Could that ultimately be the respite the home mortgage market would certainly be awaiting?

A Consider Home Mortgage Fees Throughout Past Economic Crises

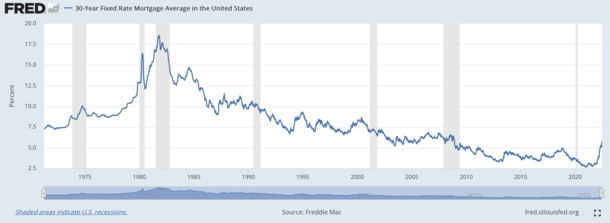

The graph above reveals the typical 30-year fixed-rate home mortgage based upon Freddie Mac information, obtained from FRED, Reserve Bank of St. Louis The shaded parts are united state economic crises.

One of the most current economic crisis was the COVID-19 economic crisis that lasted from February to April of 2020.

It was really short-term, however throughout that time the 30-year set home mortgage still dropped from 3.45% to 3.23%, per Freddie Mac’s regular study.

Prices remained to drop afterwards as well as at some point struck document lows in January 2021.

Throughout the Great Economic downturn, which extended from December 2007 to June 2009, 30-year set home mortgage prices began around 6.10% as well as was up to about 5.42%.

That economic crisis was brought on by the home mortgage situation, where loosened mortgage borrowing broke down the worldwide monetary system.

In the very early 2000s economic crisis, from March 2001 to November 2001, home mortgage prices started at 6.95% as well as was up to 6.66%.

In the very early 1990s economic crisis, from July 1990 to March 1991, home mortgage prices dropped from around 10% to 9.5%.

The previous economic crisis, from July 1981 to November 1982, saw prices plunge from 16.83% to 13.82%.

As well as the 1980 economic crisis from January 1980 to July 1980 saw prices relocate lower from 12.88% to 12.19%.

In all circumstances, home mortgage prices decreased throughout an economic downturn Obviously, the decrease varied from just 0.22% to as big as regarding 3%.

The only exemption was the 1973-1975 economic crisis, activated by the 1973 oil situation, in which prices climbed up from 8.58% to 8.89%.

That was a duration of supposed stagflation, which some experts think is taking place once again. That stays to be seen.

Clearly, house owners, possible house customers, as well as the home mortgage market will certainly all be expecting that last, huge decrease.

When you take a look at those amount of time, numerous financial experts contrast the 1980s to today, so it’s feasible we might see huge alleviation, at some point.

The trouble is just how much a lot more do home mortgage prices rise in the meanwhile, prior to an economic downturn takes place, if it also takes place whatsoever?

Will the 30-year set maintain increasing as well as struck 7 or 8% by late 2022 as well as very early 2023, after that be up to 6%?

If that holds true, any type of decrease pertaining to an economic downturn would certainly simply obtain us back to the enhanced degree where prices rest currently.

To put it simply, plan for even worse as the Fed attempts its darndest to stem rising cost of living as well as really hope points kick back down swiftly after that.

In either case, you might intend to kiss the 3-4% home mortgage prices bye-bye, at the very least for the direct future.

See additionally: Residence Rates vs. Economic Crises