{kind=link}

You’ve placed in ten years of civil service. You’re close to mercy — perhaps simply a couple of months short — and after that you learn that a stretch of deferment or forbearance doesn’t count. PSLF Buyback exists to deal with that. It allows you pay a round figure equivalent to what your income-driven repayment would certainly have been throughout those missing out on months, and they count towards your 120. Done right, it can open mercy you’ve currently made. Done incorrect or disregarded, it can cost you months or years of extra repayments. This overview strolls you with precisely just how PSLF Buyback functions, exactly how to use, and what to look out for in 2026.

What Is PSLF Buyback?

PSLF Buyback allows consumers retroactively transform months invested in qualified deferment or forbearance right into certifying PSLF repayments. As long as you held a certifying civil service task throughout those months, you can make a lump-sum repayment equivalent to what your income-driven payment (IDR) prepare repayment would certainly have been — and those months count towards the 120-payment overall needed for mercy.

New to PSLF? Prior to diving right into buyback, obtain the complete photo at PSLF Fundamentals and Small Print.

That This Aids

Buyback is created for consumers that:

- Have 120 months of qualified certifying work yet lack 120 certifying repayments

- Shed months to deferment or forbearance — consisting of the COVID-19 repayment time out (March 2020–September 2023) or the SAVE strategy management forbearance

- Required instant mercy: You can just utilize buyback if the extra months will certainly cause mercy of your finances.

conserve strategy consumers: If you’re one of the 7+ million consumers presently embeded the SAVE repayment time out, those months are not immediately certifying. Buyback is the only method to transform them — yet just when you’ve gotten to 120 months of certifying work.

If you’re still years far from 120 repayments, buyback isn’t readily available yet. However track your deferment/forbearance months very carefully so you’re ready when the moment comes.

Why It Issues

PSLF mercy is completely tax-free at the government degree — there’s no expiry on that particular advantage. For many consumers, the mathematics is definitive: a consumer with 8 months of forbearance and a $75 IDR repayment can redeem those months for $600 and leave with their whole staying equilibrium forgiven. The only caution: buyback just makes good sense if it straight leads to your mercy. If you still require a lot more certifying repayments, maintain making them and review this when you’re close.

That Is Qualified for PSLF Buyback

Quick Qualification Recommendation

| Standards | Qualified? | Notes |

| Straight Financing with impressive equilibrium | ✅ | Need to still owe cash on your finances |

| FFEL or Perkins Finance | ❌ | Need to settle right into a Straight Financing initially. Combination makes use of a heavy standard for PSLF matters and does not reset to no, yet you cannot buy back months from prior to the loan consolidation financing’s very first dispensation day. |

| Enough qualified certifying work | ✅ | You have to have adequate qualified work to ensure that redeeming the months would certainly bring you to a minimum of 120 certifying repayments. |

| Deferment/forbearance months with certifying work | ✅ | You have to have helped a certifying company throughout those months. |

| Finances currently settled, forgiven, or released | ❌ | Not qualified. |

| Months prior to a combination financing’s very first dispensation | ❌ | Not qualified for PSLF buyback. |

Complete Qualification List

You have to fulfill every one of the following:

- You have a Straight Financing with an exceptional equilibrium (not settled, released, or forgiven).

- You have actually accredited certifying civil service work.

- The months you wish to redeem remained in qualified deferment or forbearance (in-school deferment and moratorium do not certify).

- Redeeming those months would certainly bring you to a minimum of 120 certifying repayments.

You are NOT qualified if:

- You have FFEL or Perkins Loans not yet settled right into a Straight Debt Consolidation Finance

- The months you wish to redeem are from prior to your loan consolidation financing’s very first dispensation day

- Your finances are currently settled, forgiven, or released

Debt Consolidation Caution

Since September 2024, loan consolidation makes use of a heavy standard of your certifying repayment matters as opposed to resetting to no. The formula is based upon each financing’s equilibrium and repayment background, implying bigger finances lug even more weight.

If your biggest financing has less certifying repayments, loan consolidation can lower your general matter.

Crucial for PSLF Buyback: Months that happened prior to your loan consolidation financing’s very first dispensation day are not qualified for buyback.

If you are close to 120 certifying repayments and thinking about PSLF buyback, evaluate your repayment background very carefully prior to settling.

July 1, 2026 Debt Consolidation Due Date: If you settle your finances on or after July 1, 2026, you will certainly shed accessibility to all heritage income-driven payment strategies (IBR, PAYE, ICR, and CONSERVE). Your only income-driven alternative will certainly be the brand-new Settlement Support Strategy (RAP), which might cause greater month-to-month repayments for lots of consumers. If you’re thinking about loan consolidation for PSLF functions, doing so prior to July 1, 2026 maintains substantially even more payment strategy choices. This limitation relates to any kind of loan consolidation or brand-new Straight Financing loaning on or afterwards day.

Which Months Can You Redeem?

Among one of the most typical inquiries regarding PSLF Buyback is: “Can I redeem COVID-19 forbearance months?” COVID-19 repayment time out months currently count as $0 certifying PSLF repayments if you license work. Buyback is just appropriate if your tracker improperly notes them as ineligible.

✅ Qualified Deferment and Forbearance Kinds

These months receive buyback, given you had certifying work throughout every one:

- COVID-19 repayment time out (March 2020 – September 2023)

- conserve strategy management forbearance

- Economic challenge deferment

- Clinical or oral internship/residency deferment

- Cancer cells therapy deferment

- Energetic armed forces task deferment

- AmeriCorps solution deferment

- Educator Financing Mercy forbearance

- Regional or nationwide emergency situation forbearance

- PSLF application handling forbearance

- Pending consumer protection forbearance

- Management forbearance as a result of payment strategy modifications

Pro-Tip on the COVID Time Out: While practically qualified, the COVID-19 repayment time out currently counts towards PSLF as $0 certifying repayments. You just require to send a PSLF Kind accrediting your work for those years to obtain credit scores free of charge. Do not spend for a buyback on these months unless your StudentAid.gov tracker especially notes them as “disqualified.”

❌ Months That Are Never Ever Qualified

No matter your work, these standings cannot be redeemed:

- In-school deferment (One of the most typical factor for rejection—see note listed below)

- Moratorium

- Default

- Personal Bankruptcy

- Complete and Irreversible Special needs tracking duration

⚠️ The “In-School” Catch: Several public slaves function permanent while going after an academic degree. If your finances were positioned in In-School Deferment throughout that time, those months are purely disqualified for buyback. You can just obtain credit scores for those months if you clearly asked for to forgo the deferment at the time you remained in college. If you didn’t forgo it after that, you cannot “purchase it back” currently in 2026.

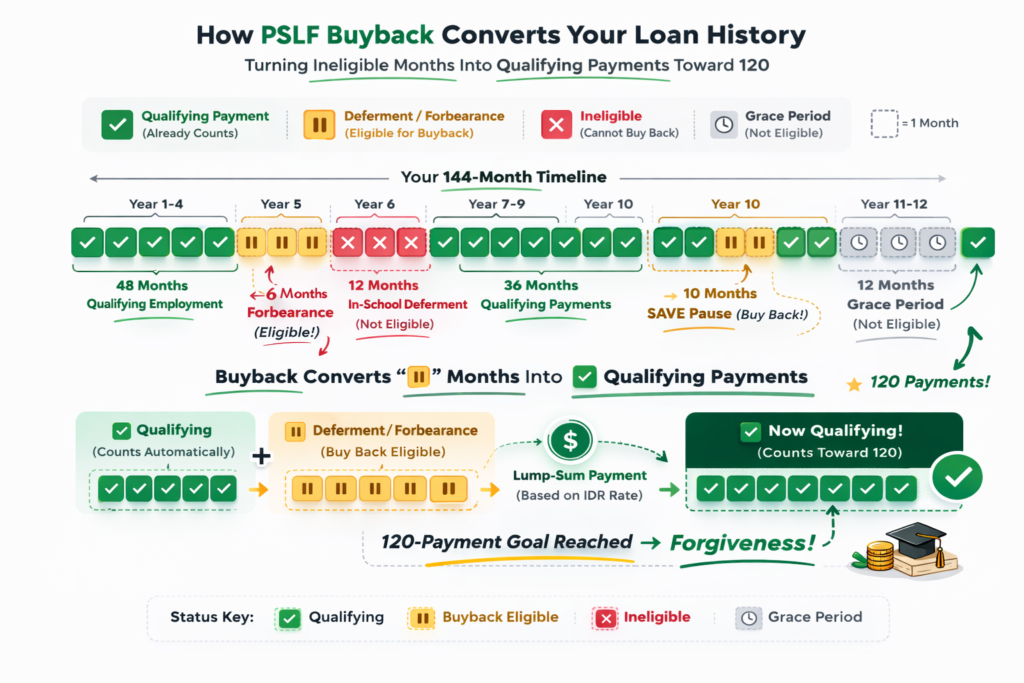

Timeline Visual

Consider your financing background as a row of months. Buyback converts ⏸ months right into ✅ months:

Just How Is PSLF Buyback Computed?

Your buyback expense is based upon what your month-to-month repayment would certainly have been throughout the months you’re transforming. The Division of Education and learning identifies this based upon readily available payment and earnings information — out how much time the duration lasted.

Situation A: You Got on an IDR Strategy at the Time

For forbearances/deferments under twelve month:

Your month-to-month buyback quantity is the minimal of:

- The IDR repayment instantly prior to the deferment/forbearance duration, or

- The IDR repayment instantly after the duration

Instance: If your repayment was $50 prior to a 6-month forbearance and $70 after, your buyback price is $50/month.

For constant forbearances/deferments twelve month or longer:

The Division of Education and learning will certainly need income tax return and family members dimension documents for every afflicted year to by hand determine what your IDR repayment would certainly have been. If you do not give documents within the called for duration (generally 1 month), the computation defaults to the 10-year Conventional Settlement Strategy quantity — which is generally a lot greater.

⚠️ Crucial for SAVE forbearance consumers: The SAVE lawsuits time out that started in July 2024 has actually currently gone beyond twelve month. If you’re redeeming conserve forbearance months, anticipate to give tax obligation documents for hands-on computation as opposed to counting on the “minimal of 2 repayments” guideline.

Situation B: You Were Out an IDR Strategy (or Earnings Need To Be Rebuilt)

If you were out an IDR strategy throughout those months — or if the Division requires to rebuild your earnings — your repayment will certainly be determined by hand.

You might be asked to give:

- The determined IDR quantity (based upon your earnings at the time), or

- The 10-year Conventional Settlement Strategy quantity

You’ll be provided a restricted home window (typically around 1 month) to send this documents. If you do not give it, the computation might skip to the 10-year Conventional Settlement Strategy quantity — which is generally greater.

The Repayment “Flooring”

Your last buyback quantity will certainly be the reduced of:

- Income tax return

- Family members dimension details

- Earnings documents for every appropriate fiscal year

Grandfather Clause: $0 Repayment → Automatic Mercy

If your earnings at the time would certainly have led to a $0 IDR repayment, your buyback arrangement will certainly mirror $0 owed. No repayment is called for.

Nonetheless, you have to still send a PSLF Buyback demand and finish the procedure. Mercy is not set off up until your demand is evaluated and authorized.

Estimation Instances

| Situation | IDR Repayment | Months | Complete |

| 6 months clinical deferment | $50 | 6 | $300 |

| 10 months conserve lawsuits time out | $150 | 10 | $1,500 |

| Out IDR | $0 | 8 | $0 |

⏱ 90-day target date: Once you get your buyback arrangement, you have 90 days to pay. Miss it and you’ll require to reboot the whole procedure.

Just How to Look For PSLF Buyback: Action-by-Step

Step 1: License All Qualifying Work

Utilize the PSLF Aid Device on StudentAid.gov to license every duration of certifying work — consisting of the months you remained in deferment or forbearance. If your company throughout those months isn’t accredited yet, do that initially. Your demand will certainly stagnate ahead without it.

Action 2: Recognize the Months You Intend To Redeem

Log right into StudentAid.gov and evaluate your PSLF repayment tracker. Search for months tape-recorded as deferment or forbearance throughout durations when you were used at a certifying company. Keep in mind precisely which months you require to transform to get to 120.

Action 3: Send Your Demand through PSLF Reconsideration

Most Likely To the PSLF Reconsideration web page on StudentAid.gov. Pick “Civil Service Finance Mercy (PSLF) Reconsideration” and choose “PSLF Buyback” as your demand type.Include this specific language in your demand:

“I contend the very least 120 months of authorized certifying work, and I am looking for PSLF or TEPSLF discharge with PSLF Buyback. Please analyze my qualification for PSLF Buyback.”

Replicate it very carefully — this details language is needed for proper handling.

Action 4: Obtain Your Buyback Contract

See your e-mail. As soon as evaluated, you’ll get a buyback arrangement laying out precisely just how much you owe and which months are being transformed. Testimonial it very carefully — if the quantity looks incorrect, see the denial/miscalculation area listed below prior to paying.

You have 90 days from the day of this e-mail to pay. The clock begins when it’s sent out, not when you open it.

Tip 5: Make the Lump-Sum Repayment

The deal e-mail will certainly have a certain web link or directions (typically through Pay.gov) to make your repayment. Do not merely pay your servicer (like MOHELA) with your typical month-to-month site, as it might not be coded properly as a “Buyback” repayment. You have to pay the sum total in a solitary deal within the 90-day home window.

Action 6: Verification and Mercy Handling

Once the repayment is refined, your PSLF Repayment Tracker will certainly upgrade. Last discharge can take an added 60–90 days after the repayment is made. Any kind of routine repayments you made throughout this waiting duration will certainly be immediately reimbursed after your equilibrium strikes no.

Tips for a Smooth Refine

- Screenshot whatever — types sent, verification displays, e-mails got. The procedure extends several websites and documents secures you if anything obtains shed.

- Look For the 90-day clock — it begins with the day the arrangement e-mail is sent out, closed.

- Don’t stop repayments — proceed your routine month-to-month repayments up until mercy is refined.

- License work very first — missing out on work accreditation is one of the most typical factor demands delay or obtain rejected.

- Inspect your “Spam” folder — The buyback deal originates from the Division of Education and learning, not your servicer. Several consumers reported missing their 90-day home window since the main e-mail was flagged as scrap.

What Takes Place After You Send: Realistic Expectations

⚠️ Stockpile alert: Since February 2026, greater than 86,520 PSLF Buyback demands are pending. Some consumers that sent in late 2024 are still waiting — over a year later on. This is not a factor to postpone; sending faster places you previously in the line. However don’t rely on a certain mercy day up until you have actually a verified arrangement in hand.

Right Here’s what the procedure resembles after entry:

- No online standing control panel — updates come over e-mail just. Inspect your spam folder and maintain your StudentAid.gov e-mail address present.

- Continue paying throughout the whole waiting duration. Quiting early can complicate your account standing.

- Overpayment reimbursements — if you proceed making routine month-to-month repayments while awaiting your buyback to be refined (which is suggested), you will likely spend for months 121, 122, and past. As soon as your buyback is completed and your account strikes no, any kind of routine repayments made after your 120th month will certainly be immediately reimbursed by the Division of Education and learning.

⚠️ Program security note: PSLF Buyback was produced in 2023 by policy, not regulations — implying its policies can alter without an act of Congress. Since very early 2026, pending lawful difficulties to PSLF-related policies can present brand-new constraints. The core PSLF program was developed by law, yet regulative analyses — consisting of buyback — can alter.

Suppose Your Buyback Demand Is Refuted or Overlooked?

Rejections occur — usually as a result of work accreditation voids, disqualified financing kinds, or servicer mistakes. If your demand is rejected or your arrangement quantity looks incorrect, you can send for reconsideration. Prior to resubmitting, collect your work accreditation documents, financing repayment background, and all document as sustaining documents.

For a complete walkthrough of your choices:

Practical Situations

Situation 1: On IDR, 6 Months in Forbearance

Maria is a public college instructor with 114 certifying repayments. She had 6 months of monetary challenge forbearance with an IDR repayment of $50/month prior to the time out.

She accredits work for those 6 months, sends a buyback demand, and obtains a contract for $300 ($50 × 6). She pays within 90 days. Those 6 months transform to certifying repayments, bringing her overall to 120. Mercy procedures.

Situation 2: Out IDR, Deferment Spanning 2 Tax Obligation Years

James took clinical deferment for 10 months straddling 2 fiscal year. He wasn’t on an IDR strategy, so the Division of Education and learning demands his income tax return for both years.

His determined IDR repayment based upon earnings: $120/month. Complete buyback: $1,200 ($120 × 10). His staying financing equilibrium is $80,000 — redeeming those months for $1,200 is plainly beneficial.

Situation 3: Pre-Consolidation Months Are Off the Table

Sarah settled her FFEL finances right into a Straight Debt Consolidation Finance in 2015. She has 115 certifying repayments because loan consolidation and intends to redeem months from 2013–2014 — prior to the loan consolidation.

Those months are not qualified. Just months after her Straight Combination Financing’s very first dispensation day can be taken into consideration. She requires 5 even more certifying repayments the typical method. This is among one of the most typical factors of complication regarding PSLF Buyback — pre-consolidation months cannot be redeemed.

Note: While Sarah can’t ‘purchase’ these months back, they might have currently been included in her matter free of charge if they satisfied the requirements for the single IDR Account Change that happened with 2025. If they weren’t included after that, they are not qualified for PSLF buyback after loan consolidation.

Secret Takeaways: Your PSLF Buyback List

Go Through this prior to sending:

- ✅ You have Straight Finances with an exceptional equilibrium

- ✅ You have actually sufficient accredited certifying work to ensure that redeeming the months will certainly bring you to a minimum of 120 repayments

- ✅ You’ve recognized the details deferment/forbearance months you require

- ✅ Those months drop under qualified deferment/forbearance kinds

- ✅ You’ve approximated your buyback quantity (IDR repayment × variety of months)

- ✅ You’re prepared to make a lump-sum repayment within 90 days of your arrangement making use of the details web link (typically Pay.gov) in your deal e-mail.

- ✅ You’ve sent through PSLF Reconsideration picking “PSLF Buyback” with the called for buyback language

- ✅ You’re viewing your e-mail and proceeding routine repayments up until mercy is verified

Extra Resources

Frequently Asked Questions Concerning PSLF Buyback

No. The buyback quantity have to be paid as a solitary round figure within 90 days of getting your arrangement through the details web link given in your deal e-mail (generally Pay.gov).

Since very early 2026, reasonably anticipate to wait lots of months after entry prior to getting your buyback arrangement. The stockpile goes beyond 86,520 demands. After you pay, forgiveness handling includes extra weeks. Deal with the timeline as flexible up until you have actually a verified arrangement.

PSLF mercy is completely tax-free at the government degree — not a short-lived arrangement, not ending in 2026. The majority of states comply with the government exception, yet Mississippi presently tax obligations PSLF mercy at the state degree. Inspect your state’s policies or seek advice from a tax obligation expert.

You don’t require to be presently used at a certifying company. The demand is that you had 120 months of certifying work in the past, which you held certifying work throughout the details months you wish to redeem.

Moms and dad and also finances have an extra complex PSLF course — they generally require to be settled right into a Straight Combination Financing initially and are just qualified for sure IDR strategies. The TEPSLF vs. Limited Waiver post covers qualification subtleties, and Moms And Dad And Also Finance Options goes much deeper on the loan consolidation course.

Pedro Gomez is the brand-new Pupil Financing Sherpa and a Licensed Economic Coordinator™ with over a years of experience aiding customers browse intricate monetary choices. He is the creator of Global Financial Strategy, where he discusses global living, geoarbitrage, and techniques for retiring young, and likewise leads Brickell Financial Team, an authorized financial investment consultatory company concentrated on speeding up monetary flexibility.

Pedro is the engineer behind the “12 Degrees of Financial Liberty” structure and mixes pupil financing technique with lasting preparation, tax obligation performance, and investing. His job is particularly tailored towards upwardly mobile specialists, business owners, and those aiming to create a life past the default course.

Pedro is readily available for technique sessions and press questions.