{kind=link}

The data supplied on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

Some credit score information it’s essential to know are your credit score rating relies on 5 key elements, FICO credit score scores vary from 300 to 850, checking your personal credit score received’t harm your rating, and twelve extra information outlined under.

With the entire deceptive and incorrect details about credit score floating round, it’s no surprise a few of us really feel misplaced in relation to our credit score stories and credit score scores. Thankfully, we’re right here to assist set every thing straight with these easy and clear explanations.

We’ve taken the time to compile crucial credit score information it’s essential to know to grasp your credit score and every thing that impacts it. Simply as importantly, we’re setting the file straight in relation to credit score myths which have been lingering for too lengthy. Learn on to be taught every thing you’ve all the time needed to find out about credit score.

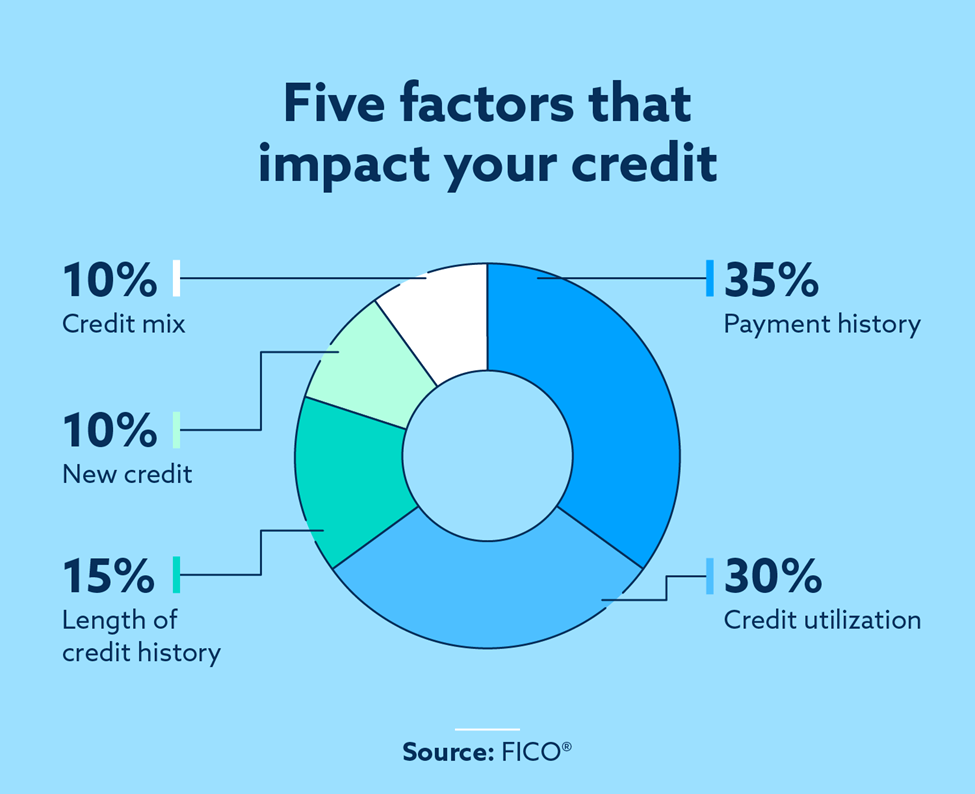

1. Your credit score rating relies on 5 key elements

Most lenders make their choices utilizing FICO credit score scores, that are primarily based on 5 key elements. That signifies that if you apply for a brand new bank card or mortgage, these are the first influences on whether or not you’ll find yourself getting permitted. Listed below are the 5 elements, so as of significance: fee historical past, credit score utilization, size of credit score historical past, credit score combine and new credit score inquiries.

- 35% – Fee historical past. Your capability to persistently make funds has the largest impression in your rating. Having late and missed funds is detrimental to your credit score rating, whereas a streak of on-time funds has a optimistic impact.

- 30% – Credit score utilization. Your utilization measures how a lot of your out there credit score you’re utilizing throughout all your playing cards. Through the use of one-third or much less of your whole credit score restrict, you could possibly assist enhance your credit score.

- 15% – Size of credit score historical past. Generally, having an extended credit score historical past is useful, although it will depend on how responsibly you’ve used credit score over time. Utilizing credit score nicely over time indicators to lenders that you may be trusted to handle your funds.

- 10% – New credit score. Making use of for brand spanking new credit score results in laborious inquiries, which may negatively impression your credit score rating. Spacing out your new credit score functions—and solely making use of for credit score if you want it—helps your rating.

- 10% – Credit score combine. Having a wide range of various kinds of credit score—like bank cards, an auto mortgage or a mortgage—can affect your rating as nicely. A various credit score portfolio demonstrates your capability to efficiently handle various kinds of credit score.

With the information of precisely how your rating will get calculated, you can also make smarter choices with credit score.

Backside line: Credit score scores aren’t as mysterious as they first seem, and you’ve got management over the entire elements that decide your rating.

2. Credit score stories are completely different than credit score scores

Though they’re associated, a credit score report and a credit score rating are completely different. Additionally, it’s a bit deceptive to speak a few single credit score report or a single credit score rating, as a result of the truth is that you’ve got a number of completely different credit score stories, and your credit score rating could be calculated in many various methods.

- A credit score report is a set of details about your credit score behaviors, just like the accounts you’ve got and if you make funds. Three predominant bureaus—Experian, Equifax and TransUnion—every publish a separate credit score report about you.

- A credit score rating makes use of the knowledge in your credit score report back to create a numerical illustration of your creditworthiness. In different phrases, the entire info in your report is simplified right into a single quantity that provides lenders an concept of how possible you’re to repay a debt.

Surprisingly, your credit score report doesn’t embody a credit score rating. As a substitute, lenders who entry your report use formulation to find out a rating if you apply for credit score. The commonest scoring fashions are FICO and VantageScore, however lenders could make modifications to the calculations to offer extra weight to areas which are extra necessary to them.

Backside line: You’ll wish to be acquainted with each your credit score stories and your credit score scores, as they every play a job in serving to you receive new credit score.

3. Adverse credit score objects will ultimately come off your credit score report

Adverse objects in your credit score report could cause harm to your credit score rating. Adverse objects embody late funds, assortment accounts, foreclosures and repossessions.

Though these things can result in vital drops in your credit score rating, their impact just isn’t everlasting. Over time, unfavorable objects have a smaller and smaller impression in your rating, so long as your credit score behaviors enhance in order that more moderen objects are extra favorable.

Moreover, most unfavorable objects ought to stay in your report for seven years on the most because of the rules set by the Honest Credit score Reporting Act. A chapter, alternatively, can last as long as 10 years in some circumstances.

Backside line: Adverse objects could cause a lower in your credit score rating, however they aren’t everlasting. Begin constructing new credit score behaviors and your rating can get well over time.

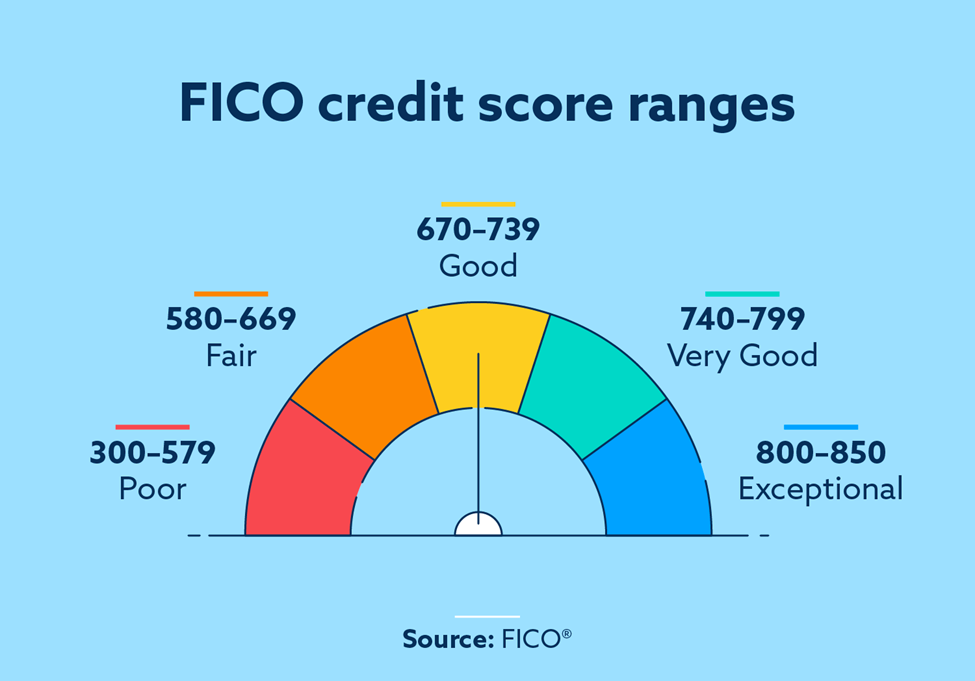

4. FICO credit score scores vary from 300 to 850

Some of the widespread credit score scoring fashions is produced by the Honest Isaac Company, also called FICO. When you could hear “FICO rating” and “credit score rating” used interchangeably, there are in reality a number of completely different scoring fashions, so you could possibly have a distinct credit score rating relying on which lender or monetary establishment you’re working with. The rating you’re assigned by FICO will normally all the time be in a variety from 300 to 850.

Accessing your FICO rating offers you the prospect to have a high-level overview of your credit score well being. Scores which are thought-about good, excellent or distinctive typically make it a lot simpler to get new bank cards or loans if you want them. Alternatively, scores which are honest or poor could make getting new credit score tougher.

Right here’s an summary of the FICO scoring ranges:

- 800 – 850: Distinctive

- 740 – 799: Very Good

- 670 – 739: Good

- 580 – 669: Honest

- 300 – 579: Poor

Keep in mind, although: credit score scores will not be fastened and everlasting. Your rating responds to elements like funds, utilization and credit score historical past, so optimistic choices now will profit your rating in the long run.

Backside line: The FICO scoring ranges lay out broad classes to offer you a way of the way you’re doing with credit score—and can even provide help to set a aim for the place you wish to be.

5. The vast majority of lenders use FICO scores when making choices

Whereas there are a number of credit score scoring fashions, nearly all of lenders test FICO scores when making choices. That signifies that if you apply for brand spanking new credit score—whether or not it’s a bank card, a mortgage or a mortgage—the rating that’s extra more likely to matter is your FICO rating.

That’s necessary to know, as a result of many free credit score monitoring companies will present you rating estimates or your VantageScore. Some bank card corporations present a FICO rating, nevertheless, and you can too request to see the credit score rating that lenders used to make their determination through the utility course of.

Thankfully, credit score scoring fashions are inclined to reference the identical information and weight elements pretty equally. Meaning in case you make on-time funds, preserve your utilization low, keep away from opening up too many new accounts and have a constant credit score historical past with a wide range of accounts, you’ll in all probability be in good condition regardless.

Backside line: Realizing your FICO rating will help you’ve got an concept of how lenders will view your utility for brand spanking new credit score.

6. You’ve got many various kinds of credit score scores

Credit score scores fluctuate primarily based on the credit score bureau reporting them and the credit score scoring mannequin used. The key credit score bureaus all have barely completely different info concerning your credit score historical past. Which means these three, together with different credit score reporting businesses, report a number of FICO credit score scores to lenders to account for various info they’ve collected.

There are additionally completely different scores particular to specific industries. For instance, auto lenders assessment completely different threat elements than mortgage lenders, so the scores every lender receives would possibly differ. Though it will possibly get complicated, crucial issues to recollect are the 5 core elements that have an effect on your credit score rating.

Backside line: Though many individuals reference their credit score rating within the singular, the reality is that there are lots of various kinds of credit score scores that bear in mind various factors.

7. Checking your personal credit score received’t harm your rating

Many individuals imagine that checking their credit score rating or credit score report hurts their credit score, however fortuitously, this isn’t true. Getting a replica of your credit score report or checking your rating doesn’t have an effect on your credit score rating. These actions are known as “gentle” inquiries into your credit score, and whereas they’re famous in your credit score report, they shouldn’t have any impact in your rating.

Arduous inquiries, alternatively, are famous when lenders have a look at your credit score throughout an utility course of—and these can quickly scale back your rating. That is used to discourage you from making use of for brand spanking new credit score too regularly. Nonetheless, the impact is often small, and after a few years the notation of a tough inquiry will depart your report.

Backside line: You’ll be able to test your personal credit score report and credit score rating with none unfavorable impact—and we truly encourage you to take action to remain on high of your credit score well being.

8. You’ll be able to test your credit score rating and credit score stories without cost

There are three predominant methods to test your credit score without cost. You’ll possible need to check out each your credit score stories and your credit score scores. Right here’s how one can come up with each of these:

- You’re entitled to a free credit score report as soon as every year by visiting AnnualCreditReport.com, a government-sponsored web site that provides you entry to your stories from TransUnion, Experian and Equifax.

- You could possibly test your credit score rating free by contacting your financial institution or bank card firm. Moreover, many free companies—like Mint—allow you to observe your rating without cost. Simply make sure that to notice which form of credit score rating you’re seeing, as a result of there are lots of completely different scoring strategies.

The data you discover in your credit score report lays out the elements that decide your credit score rating. By scanning your report carefully, you’ll possible discover out the most effective technique for bettering your rating—for example, by bettering your fee historical past or decreasing your utilization.

Backside line: Details about your credit score is freely out there, so benefit from these sources to remain on high of your credit score report and rating.

9. Your credit score rating can price you cash

In the end, the aim of credit score scores is to assist lenders decide whether or not they need to give you new credit score, like a mortgage or a bank card. A decrease rating signifies that you could be be at higher threat for default—which implies the lender has to fret that you simply received’t pay again your money owed.

To offset this threat, lenders typically deny credit score functions for these with decrease scores, or they prolong credit score with excessive rates of interest. These rates of interest can price you some huge cash over time, so working to enhance your credit score rating can have a measurable impact in your monetary life.

Contemplate, for instance, a $25,000 auto mortgage. With a good credit score rating, you might safe an rate of interest of 5.3 %—so that you’ll pay a complete of $3,513 in curiosity over 5 years. With a superb credit score rating, your charge might drop to three.1 %, and also you’ll save almost $1,500 in curiosity expenses over that very same five-year interval.

Backside line: An excellent credit score rating can have a optimistic impression in your funds, and a nasty rating can price you cash in curiosity expenses.

10. Canceling outdated bank cards can decrease your rating

When you’ve got a bank card that you simply’re not utilizing, you might be tempted to shut the account completely. Earlier than doing that, although, take into account the way it might impression your credit score rating.

Recall that two credit score elements are utilization and size of credit score historical past. Closing an outdated account might have an effect on one or each of these elements in relation to calculating your rating.

- Your credit score utilization might drop after closing an account as a result of your credit score restrict will possible be decrease. Since utilization represents all your balances divided by your whole credit score restrict, your utilization will go up in case your credit score restrict goes down (and in case your balances keep the identical).

- Your size of credit score historical past might be lowered in case you shut an older account that’s elevating the common age of your credit score.

Some folks fear that having a zero steadiness on their bank card can negatively impression their rating. That is only a credit score delusion. A zero steadiness means you aren’t utilizing the cardboard to make any purchases. Holding the bank card open whereas not utilizing it truly works to your profit. You’re capable of contribute to the size of your credit score historical past, whereas not risking the prospect of debt and late funds.

It’s possible you’ll want to make use of the cardboard from time to time to keep away from having it closed. Moreover, if the cardboard has an annual payment, you might want to shut the cardboard or ask to have the cardboard downgraded to a model that doesn’t have a payment. Nonetheless, if there’s a technique to preserve the cardboard open, it’s typically good to take action even in case you don’t plan to commonly use it.

Backside line: An outdated bank card can profit your credit score rating even in case you aren’t utilizing it anymore.

11. You’ll be able to nonetheless get a mortgage with poor credit

It’s true that getting a mortgage could be tougher with poor credit, nevertheless it’s not inconceivable. There are poor credit loans particularly for folks with decrease credit score scores. Observe, nevertheless, that these loans typically include increased rates of interest—or they require some form of collateral that the lender can use to safe the mortgage. Meaning in case you don’t pay your mortgage again, the lender will have the ability to seize the property you place up as collateral.

In case you don’t want a mortgage instantly, you could possibly take into account making an attempt to rebuild your credit score earlier than making use of. There are credit score builder loans, that are particularly designed that will help you construct up a robust fee historical past and enhance your credit score within the course of. Not like a standard mortgage, you pay for a credit score builder mortgage every month after which obtain the sum after your closing fee. Since these loans signify no threat to lenders, they’re typically keen to increase them to folks with poor credit score historical past trying to increase their rating.

Backside line: You may get a mortgage even with poor credit—however typically it’s sensible to seek out methods to boost your rating earlier than making use of.

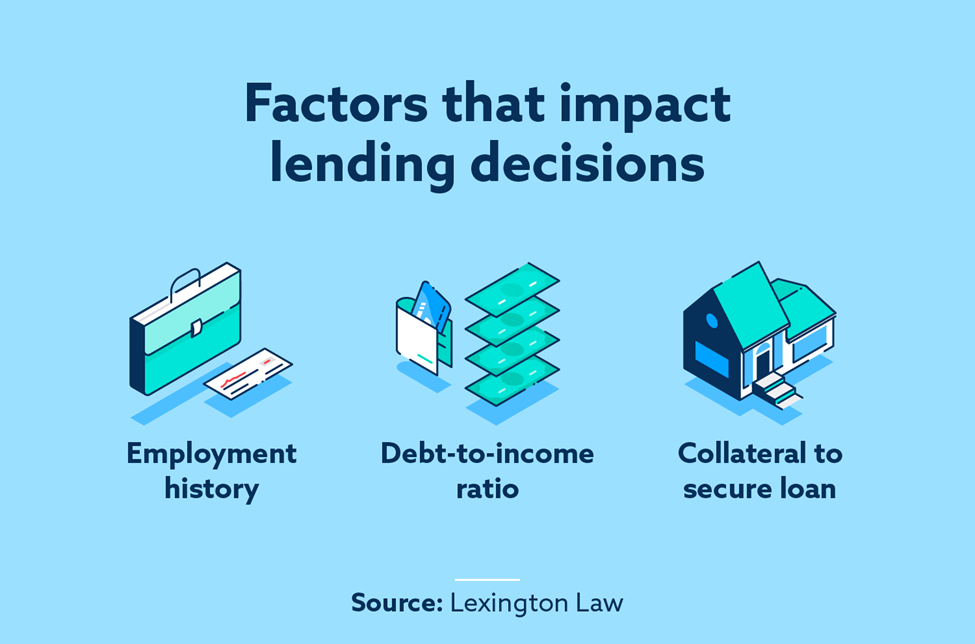

12. Credit score scores aren’t the one deciding issue for lending choices

Whereas credit score scores are necessary in lending choices, lenders could take different elements into consideration when deciding whether or not to give you new credit score. For instance, your revenue and employment can play a big position in your approval odds. Moreover, some loans (like auto loans and mortgages) are secured by collateral that the lender can seize in case you default. These loans could also be thought-about much less dangerous for the lender in sure circumstances as a result of the asset will help offset any losses from nonpayment.

In lots of circumstances, your debt-to-income ratio can be an necessary consider whether or not you’re permitted for a mortgage or bank card. Lenders take into account your present month-to-month debt funds (from all sources) in addition to your month-to-month revenue to find out whether or not you might be overextended financially.

Two completely different folks could pay $1,500 every month for pupil loans, a automobile fee and a mortgage. That mentioned, if one particular person makes $3,500 every month and the opposite makes $8,000 every month, their conditions will likely be thought-about very otherwise by a possible lender.

Backside line: Holding your credit score rating excessive will help you safe credit score if you want it, however you’ll wish to keep on high of all points of your monetary well being.

13. Your credit score report will help you see fraud

Recurrently checking your credit score report will help you discover fraud or identification theft. If somebody is utilizing your info to open accounts, they are going to present up in your credit score report.

In case you discover an account that you simply didn’t open, you’ll wish to begin taking steps to defend your identification from any additional harm. You might also wish to freeze or lock your credit score, which prevents anybody from utilizing your info to open up extra accounts.

Backside line: Reviewing your credit score report offers you a chance to note when one thing is amiss.

14. Joint accounts have an effect on your credit score scores, however you do not need joint scores

When you’ve got a joint account with another person, that account will likely be mirrored on each of your credit score stories. For instance, a mortgage that was opened by you and your partner will present up for each of you—and can have an effect on each of your credit score scores. That mentioned, your credit score historical past, credit score report and credit score rating stay separate. Nobody—together with married {couples}—has a joint credit score report or joint credit score rating.

Along with joint accounts, you might also have licensed customers in your bank card, or be a licensed person your self. Approved customers have entry to account funds, however they aren’t chargeable for money owed. That signifies that in case you make somebody a licensed person in your bank card, they will rack up expenses, however you’ll be on the hook in the event that they don’t pay.

As a result of joint account house owners and licensed customers can affect credit score scores in vital methods, we advise you to watch out about who you open accounts with or present authorization to.

Backside line: Though joint account house owners and licensed customers can affect another person’s credit score, there aren’t any shared credit score stories or joint credit score scores.

15. Many credit score stories comprise inaccurate credit score info

The Federal Commerce Fee discovered that one in 5 folks has an error on not less than certainly one of their credit score stories, and these inaccuracies can significantly impression your credit score. (Additionally see this 2015 follow-up research from the FTC for extra info concerning credit score report errors.) For this reason you must regularly test your credit score report and dispute any inaccurate info. For instance, since fee historical past accounts for 30 % of your credit score rating, one unsuitable late fee can considerably harm your rating.

It’s necessary to get your credit score information straight so that you perceive precisely how various things impression your rating. One of many first issues you must be taught is how one can learn your credit score report so you’ll be able to rapidly spot discrepancies and be sure that the knowledge reported is honest and correct.

After scrutinizing your credit score report, you’ll be able to look into different methods to repair your credit score, like paying late or past-due accounts, so you’ll be able to assist your credit score together with your newfound information. It’s also possible to benefit from Lexington Legislation Agency’s credit score restore companies to get further assist and extra authorized information to help you.

Backside line: Your credit score report might have inaccurate info that’s hurting your rating unfairly. Thankfully, there’s a credit score dispute course of that may provide help to clear up your report and guarantee the entire info on it’s right.

Observe: Articles have solely been reviewed by the indicated legal professional, not written by them. The data supplied on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained throughout the web site don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.