{kind=link}

1. Home loan prices will certainly fall under the 5% array

2. Home rates will certainly be level (otherwise reduced)

3. Cost will certainly boost however continue to be constricted

4. Home sales will certainly climb, however not as long as anticipated

5. The home building contractors will certainly battle to relocate stock

6. A lot more debtors will certainly transform to variable-rate mortgages

7. The largest home mortgage lending institutions will certainly get market share

8. A lot more property owners will certainly touch equity to preserve way of lives

9. We’ll see brief sales make a return

10. The real estate market won’t collapse

Benefit: We’ll see some kind of brand-new real estate plan turned out by the Trump Management.

2025 Was a Little Better Than 2024

Welp, one more year has actually reoccured, and while it wasn’t a lot various than 2024, points were a little more vibrant for the home mortgage and property market.

If you remember, the stating in 2024 was “endure ‘til ’25.” There doesn’t appear to be a comparable motto for 2026 so possibly the most awful lags us.

Sure, some still believe we get on the cusp of one more real estate accident, however when you go into the information, all the components merely aren’t there.

Rather, possibilities are it’ll be a little bit even more of the very same in 2026, though with problems gradually going back to typical.

Obviously, property is regional so efficiency will certainly constantly differ by market.

Home Mortgage Prices Will Certainly Come Under the 5% Variety

I constantly begin with home mortgage prices since that’s constantly one of the most discussed subject.

My basic reasoning is home mortgage prices will lastly dip right into the fives in 2026, likely by the initial quarter.

I obtain that there’s resistance at those degrees, however we’re additionally just regarding 20 basis factors away.

Eventually, it will just take a negative work report or more to obtain us there, presuming rising cost of living remains to reveal indications of renovation.

The month-to-month cost savings could not be big, however it would certainly suffice to obtain even more price and term refinances to pencil.

And it would certainly be a mental success for possible home customers from a view point ofview.

You can see all the 2026 home mortgage price forecasts in the linked blog post to see what others believe. The fast takeaway is mainly level.

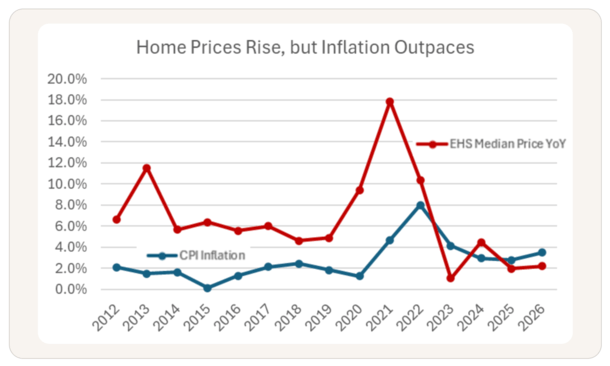

Home Costs Will Certainly Be Apartment (or perhaps Reduced)

Equally as a lot of experts anticipate level home mortgage prices in 2026, a lot of anticipate home rates to be fairly unmodified too.

The projections differ rather, however Zillow just anticipates a 1.2% increase in residential property worths following year.

And it’s an also reduced 0.5% rise from Compass primary financial expert Mike Simonsen.

Over at Real Estate Professional, they anticipate a 2.2% rise, which is still quite level, and very little far better than the 2.2% seen this year.

That indicates genuine home rates, readjusted for rising cost of living, would certainly be down, also if they’re up on a small basis.

In some markets, such as the hard-hit Sunlight Belt, home rates can really drop on a small basis.

I don’t anticipate large decreases, however it’s definitely feasible to see adverse YoY adjustments provided increasing stock and bad cost.

Cost Will Certainly Boost Yet Inadequate

Mentioning real estate cost, the mix of reduced home mortgage prices and level (or reduced) home rates will certainly be a favorable for possible home customers.

The trouble is it’s most likely not mosting likely to suffice to actually relocate the dial. We’ve seen cost gradually boost this year for these very same factors.

And it’ll likely proceed right into 2026, however could not suffice to obtain a consumer’s DTI proportion in array. Or merely lure them to embark on the fencing.

At the very same time, it might not persuade somebody to provide their home, understanding they’ll require to acquire a substitute residential property.

We’ve had a great deal of potential vendors control the marketplace in the last few years, and we additionally have potential customers as well.

It’s a standoff that has actually gradually improved, however remains to be smolder since not a great deal has actually transformed.

Home Sales Will Certainly Increase, Yet Disappoint Assumptions

I do think home sales will certainly climb in 2026, however from really reduced degrees. Bear in mind, existing home sales went to a near-30 year reduced in 2024, simply over 4 million.

This year they climbed partially and following year they’re anticipated to inch up even more, however continue to be near to 4 million.

Fannie Mae fixes the existing sales price at regarding 4.4 million, which is a suitable 7.5% renovation, however well listed below what NAR anticipates.

Even More of the very same troubles will certainly torment the real estate market in 2026, consisting of bad cost, home mortgage price lock-in, and minimal for-sale stock.

Maybe a great deal even worse, however it’s not mosting likely to be a treasure trove, despite home mortgage prices possibly dropping listed below 6%.

Specifically if the economic situation deviates as customer costs lastly reaches us, and work losses install.

The Home Contractors Will Certainly Battle

The previous couple of years the home building contractors got on a roll since they were sort of the only video game in the area.

No one was providing their homes, so they had little competitors, in spite of bad home purchaser need.

On top of that, they had the ability to acquire down home mortgage prices dramatically making use of an unique benefit referred to as an ahead dedication.

This implied home mortgage price buydowns right into the twos and sixes (and even reduced), sufficient to lure unreliable customers to start.

Nevertheless, they’ve seen their stock start to accumulate as sales have actually slowed down, with purchases anticipated to drop 1.6% this year, per Fannie Mae.

They do anticipate a 4.5% uptick in brand-new home sales in 2026, however I’m not completely persuaded provided the places of brand-new homes remain in locations with a supply excess.

And despite large sales giving ins, the contractors are battling to relocate homes.

The one caution is if they obtain some kind of increase from a brand-new plan adjustment, or some kind of aid press.

Much More Consumers Will Depend On ARMs

Recently, there’s been a change to variable-rate mortgages, which have actually fallen victim to temporary prices like the government funds price.

With the assumption that the 30-year dealt with might have actually peaked and can be level, some are picking an ARM to attain an also reduced settlement.

It can make good sense if the rates of interest spread agrees with, though you need to take care since some lending institutions hardly use a discount rate versus a 30-year dealt with.

We’ve additionally seen the home building contractors transform to ARMs rather than fixed-rate home loans since it’s less costly for them to drive down the month-to-month settlement for their clients.

Once more, comprehend what you’re obtaining isn’t like a 30-year dealt with. Though today most ARMs are dealt with for 5-7 years or longer, such as the 5/6 ARM and 7/6 ARM.

That’s a great deal of time to expect also reduced prices in the future and in the meanwhile, pay much less and pay for the lending quicker (as a result of the reduced price).

The Greatest Home Mortgage Lenders Will Get Back At Larger

The tale of 2025 was home mortgage lending institutions obtaining property firms and lending servicers, done in an initiative to expand also bigger.

We saw Rocket get both property brokerage firm Redfin and significant lending servicer Mr. Cooper.

And the country’s leading loan provider, United Wholesale Home Mortgage, acquire 2 Harbors, one more bigger lending servicer.

After That there was Reduced, which scooped up property site Movoto and later on partnering with property brokerage firm HomeSmart.

On top of that, Compass got competing brokerage firm Anywhere Property which can profit the favored loan provider Surefire Price.

I anticipate even more of these type of offers to occur in 2026 and for the shut ones to start to thrive.

This accompanies the brand-new trigger regulation guideline, which calls for lending institutions to have approval to connect to debtors (or a previous partnership).

Think that will have a previous partnership? Yep, the large people that have all these various other firms and/or solution the existing finances.

That provides extra regain chances while at the same time locking out their rivals.

This benefits the large people, however might injure customers if there’s much less loan provider option.

Much More Homeowners Will Certainly Touch Their Equity to Maintain Investing

We currently saw home equity loaning increase a fair bit the previous pair years, however it still fades in contrast to the very early 2000s.

On top of that, there are really couple of cash-out refinances nowadays, so most equity removal is just coming through bank loans like HELOCs and home equity finances.

Therefore, the numbers, while greater, aren’t all that insane. I’ve claimed for some time that if and when property owners actually go nuts touching equity, we can encounter troubles once again.

Specifically if home rates drop and/or if lending institutions obtain even more liberal with optimum CLTVs.

The trouble nowadays is several property owners require to touch equity simply to stay on par with their costs, which is a negative indicator for the larger economic situation.

While that seems frightening, offering requirements today are still way far better than they remained in the very early 2000s.

And as kept in mind, a lot of property owners are maintaining their low-rate, set initial home loans undamaged since they’re so low-cost.

The Return of the Brief Sale

I’ve been listening to a growing number of rumblings of brief sales go back to the real estate market.

This is when homeowner are undersea on their home loans (owe greater than the residential property deserves) however still require to market.

They were really usual throughout 2008-2013, however have actually been basically non-existent ever since as home rates rose and home mortgage prices struck document lows.

Yet we’re currently at an oblique factor once again with home rates dropping in some markets, especially areas like Florida and Texas.

Those that obtained 3%-down home loans that have actually seen their residential property loss in worth can be in difficulty if they required to market.

This is specifically important for the current vintages of home customers, believe late 2022 and 2023, when home mortgage prices were additionally high.

Extremely little of the lending equilibrium has actually been repaid and when incorporated with a flat/lower prices and purchase prices, maybe brief sale region.

Therefore, we could additionally see an uptick in repossessions as loss reduction choices start to tighten up too.

Yet once again, the bright side is the huge bulk of property owners either have their homes cost-free and clear, or have a home mortgage price in the 2-4% array.

The Real Estate Market Won’t Collision in 2026

Something I’ve explained a couple of times is that a lot of today’s home loans were stemmed when prices strike document lows.

This remained in very early 2021, and ever since, home rates have actually additionally risen greater. This indicates your regular home owner has an incredibly reduced price, a little lending equilibrium, and a reduced LTV proportion.

Yes, current home customers remain in the precise contrary setting, having actually purchased the elevation of the marketplace with 6-8% home mortgage prices.

Yet right here’s an essential information. Home sales diminished a high cliff when cost tanked, as we’ve seen with the purchase numbers striking those 30-year lows.

While it’s been hard on the market, whether it’s property representatives or lending policemans and home mortgage brokers seeing less purchases, it’s good for the marketplace.

It’s a healthy and balanced action available for sale to slow down if problems require it. In the very early 2000s, we required sales through highly-questionable funding, which is typically what triggers bubbles.

Many Thanks to the ATR/QM guideline, we simply haven’t seen the very same degree of risky loaning this cycle, also if FHA finances are a weak point.

Like I claimed, the real estate market won’t be devoid of troubled sales in 2026, however it won’t be anything like GFC problems.

It’s really typical to have troubled sales and not a straight-out bull run annually.

Will the Trump Admin Ultimately Provide Real Estate Plan Modification?

One last incentive forecast. I think the Trump admin will certainly come via with some kind of plan adjustment in 2026.

Given, this isn’t a strong forecast since Trump himself claimed a few days ago that he would certainly “introduce several of one of the most hostile real estate reform strategies in American background.”

So he much better appear with something midway respectable. Obviously, he pinned the blame of high home rates on prohibited movement because very same speech.

At the same time, they actually rose as a result of document reduced home mortgage prices incorporated with reduced degrees of home structure post-GFC.

Yet provided his admin has actually currently drifted all kinds of wild concepts, such as the 50-year home mortgage, mobile home mortgage, and making even more home loans assumable, which all failed, it’ll likely be something much less amazing.

Possibly deregulation for home building contractors to construct faster and less costly. Obviously, brand-new builds aren’t the be all, finish all service, specifically considering that their stock is currently accumulating.

Anticipating the home building contractors to construct even more when they can’t also relocate existing stock would certainly be ridiculous.

Though if there were some aids for customers, it can possibly assist. They simply need to bear in mind stabilizing supply and need, and not simply making the marketplace warm once again.

In the meanwhile, we’ll remain to wait on the pledge he made throughout his project to bring home mortgage prices pull back to 3% and even reduced!

Prior to producing this website, I functioned as an account exec for a wholesale home mortgage loan provider in Los Angeles. My hands-on experience in the very early 2000s influenced me to start covering home loans 19 years ago to assist possible (and existing) home customers much better browse the mortgage procedure. Follow me on X for warm takes.