{kind=link}

The knowledge supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

These are the three primary methods to take away closed accounts out of your credit score report: dispute any inaccuracies, ship a goodwill letter requesting removing or look ahead to the closed accounts to be eliminated after sufficient time has handed.

Closed accounts may be eliminated out of your credit score report in three primary methods: (1) dispute any inaccuracies, (2) write a proper goodwill letter requesting removing or (3) merely look ahead to the closed accounts to be eliminated over time. That stated, eradicating closed accounts can have an effect on your credit score rating, so be sure to take into account your scenario earlier than taking any motion.

It’s not all the time attainable to take away a closed account out of your credit score report, however you may try to take action if you need. Nevertheless, it’s not all the time useful to take away closed accounts, and in some circumstances, it may even decrease your credit score rating.

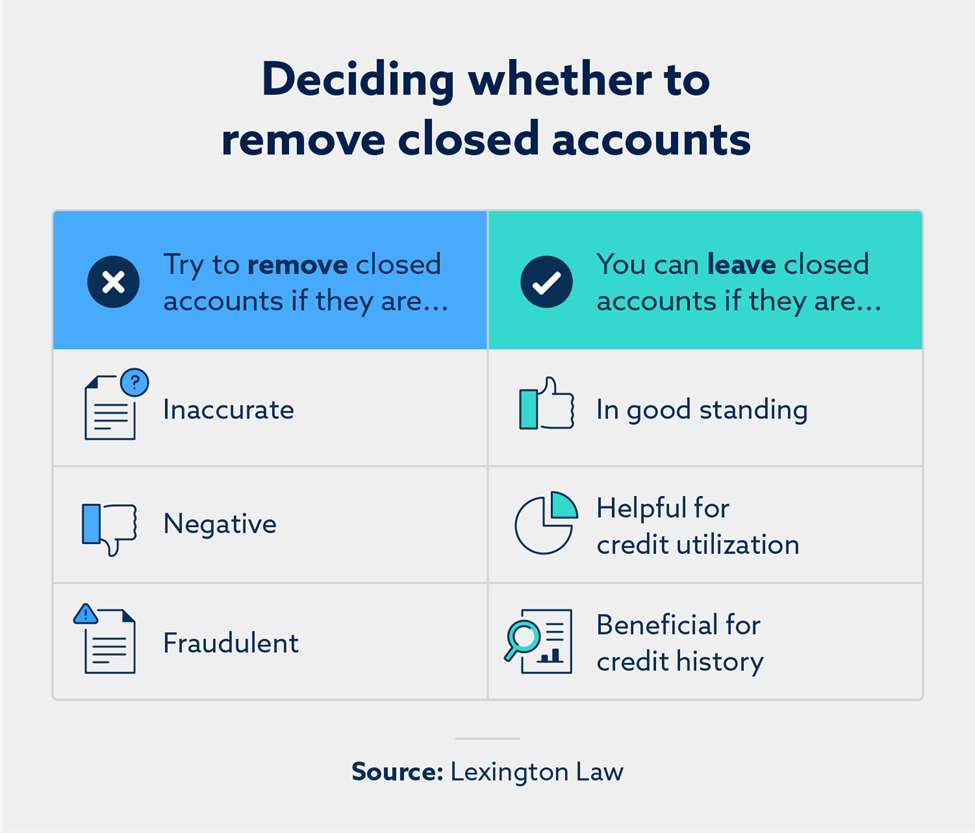

Usually, it’s best to attempt to take away any closed accounts with inaccurate adverse info, however you in all probability shouldn’t contact any accounts which are having a optimistic impact in your credit score historical past.

Beneath, we’ll speak about whether or not it’s best to attempt to take away closed accounts out of your credit score report, how closed accounts might have an effect on your credit score rating and take away closed accounts.

How you can take away closed accounts out of your credit score report

As we talked about, you may try and take away closed accounts out of your credit score report by disputing inaccurate info with the credit score bureaus, writing a proper “goodwill letter” to request removing or just ready till the account is eliminated after a time period.

Learn on to study extra about when to strive every of those completely different strategies for getting a closed account off your credit score report.

1. Dispute inaccurate info

If a closed account in your credit score report contains inaccurate info, you may dispute the data and doubtlessly get the merchandise eliminated out of your report.

How you can dispute inaccurate info:

- Ship a letter to the three main credit score bureaus—TransUnion®, Experian® and Equifax®—that explains what info you’re difficult, why you consider it’s inaccurate and that you desire to it eliminated.

- Equally, ship a letter to the monetary establishment that supplied the data to the bureaus.

- Watch for responses, then test your up to date report and rating after a month or extra has handed.

Now we have a information that particulars the dispute course of that can assist you alongside the way in which.

2. Write a goodwill letter

A goodwill letter is a proper request to a creditor asking for a adverse merchandise to be eliminated.

Though collectors usually are not required to take away adverse objects upon request, they might be prepared to take action if in case you have an extended historical past with them or if there have been particular hardships that led to the adverse merchandise.

Nevertheless, goodwill letters are typically helpful just for late or missed funds somewhat than extra vital adverse objects like assortment accounts and repossessions.

Along with goodwill letters, you may as well request that an account is eliminated utilizing a pay for delete letter. These letters can result in an settlement with a group company to take away an account in alternate for a partial or full cost. That stated, the gathering company might determine to not take away the account, and the unique account that went to collections might stay in your report.

3. Watch for the closed account to be eliminated over time

No objects keep in your report endlessly, so it’s attainable to easily look ahead to a closed account to be eliminated by itself. Gadgets on credit score studies, together with accounts which were closed, can stay on a credit score report for round seven to 10 years.

So in the event you’re fearful about an older closed account with adverse info that’s doubtlessly reducing your rating, know that ultimately it is going to drop off your credit score report. Constructive details about closed accounts additionally leaves your report after sufficient years have handed, so it’s vital to proceed to follow good credit score habits with quite a lot of account sorts.

Do you have to take away closed accounts out of your credit score report?

It’s best to try and take away closed accounts that comprise inaccurate info or adverse objects which are eligible for removing. In any other case, there may be typically no have to take away closed accounts out of your credit score report. Inaccurate info could possibly be hurting your credit score rating and must be addressed, however older accounts that present accountable credit score utilization could also be serving to your rating.

Even after closing an account—like a private mortgage or bank card—the data associated to your balances and cost historical past stays in your credit score report for a few years. Accounts closed in good standing might keep in your report for as much as 10 years, whereas accounts with derogatory marks, like assortment accounts, might stay in your credit score report for as much as seven years.

Deciding whether or not to attempt to take away a closed account finally comes all the way down to understanding the components that have an effect on your credit score.

Your FICO credit score rating is calculated based mostly on 5 primary components:

- Fee historical past (35 p.c)

- Credit score utilization (30 p.c)

- Size of credit score historical past (15 p.c)

- Several types of credit score (10 p.c)

- New credit score functions (10 p.c)

As a result of a credit score report contains each open and closed accounts, a few of these credit score components may be affected by a closed account leaving your report. For instance, in the event you made funds on a private mortgage for quite a lot of years and that account is not in your report, yourlength of credit score historical past may lower, which may negatively have an effect on your credit score.

Having a closed account eliminated out of your report might not have an effect on your rating, however in lots of circumstances, it’s smart to depart accounts in good standing in your report, as they may have a optimistic affect general.

Nevertheless, closed accounts with adverse objects eligible for removing and inaccurate info can result in a decrease rating, so working to get these accounts eliminated is a part of a sound credit score restore technique.

Eradicating closed accounts out of your credit score report: FAQ

Nonetheless not sure about take away a closed account out of your credit score report? Listed below are a couple of generally requested questions and solutions.

1. When to take away a closed account out of your credit score report

It’s best to attempt to take away closed accounts which have inaccurate or adverse objects, however depart accounts which are having a optimistic impact in your credit score historical past. Accounts with inaccurate info may decrease your credit score rating.

2. How lengthy does a closed account keep on my credit score report?

Closed accounts can keep in your credit score report for seven to 10 years, relying on the standing of the account.

3. Why is a closed account nonetheless on my credit score report?

All closed accounts keep in your credit score report for a few years relying on their optimistic or adverse historical past, except you are taking steps like sending goodwill letters or disputing inaccurate or unfair info to attempt to get the closed accounts eliminated sooner.

In case your credit score report accommodates closed accounts with inaccurate adverse objects, the staff at Lexington Legislation Agency can help you with credit score restore. By analyzing your credit score report and aiding with disputes, our staff may make it easier to make strides in bettering your credit score.

Notice: Articles have solely been reviewed by the indicated legal professional, not written by them. The knowledge supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for normal informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained inside the website don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.