{kind=link}

May 2023 be good to mortgage charges? In the event you imagine the newest Housing Forecast from Fannie Mae, then sure.

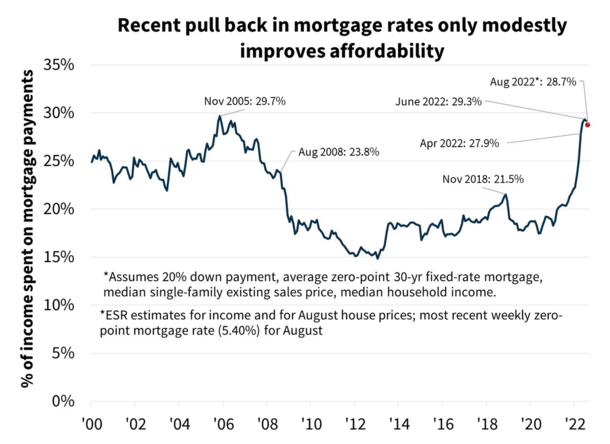

Most everybody is aware of 2022 has wreaked absolute havoc on mortgage charges, with the 30-year fastened up greater than 225 foundation factors from a yr earlier.

This, mixed with rising dwelling costs, has eroding affordability to the purpose of being at its worst since previous to the earlier housing growth (and eventual bust).

However currently mortgage charges have seen some aid after pushing 6%, they usually might even fall again into the 4s subsequent yr.

That might be large for the flagging mortgage trade, and likewise a boon to dwelling builders making an attempt to unload new stock.

Mortgage Charges May See Some Reduction in 2023

In Fannie Mae’s earlier Housing Forecast (for July), they anticipated the 30-year fastened to common 5.1% in 2023, which truly doesn’t sound too unhealthy.

However their newest launch has charges all the way down to 4.5% for 2023, with charges drifting from 5.1% within the third quarter of 2022 to 4.4% within the second half of 2023.

Assuming that involves fruition, the mortgage trade, together with dwelling patrons and the house builders, might see some critical aid.

In any case, many builders have needed to reduce costs or cut back on constructing altogether, whereas potential patrons have pulled out of buy contracts.

If mortgage charges fall again to the mid-4% vary, there’d probably be a surge of demand and an uptick in dwelling gross sales as soon as once more.

It might additionally enhance affordability markedly, which has worsened significantly to pre-bubble territory.

In gentle of those new forecasts, Fannie Mae expects complete originations to hit $2.29 trillion in 2023, a $66 billion improve from final month’s forecast.

In fact, that may nonetheless be under the $2.47 trillion forecast for 2022.

They count on 2022 mortgage refinance quantity to complete $769 billion, up $13 billion from a month in the past, pushed by these decrease anticipated mortgage charges.

And 2023 quantity is slated to be $592 billion, up $74 billion from the prior estimate.

That is excellent news for current householders with excessive charges, together with mortgage lenders that rely closely on refinance loans.

Sadly, dwelling buy mortgage quantity has been reduce by $74 billion to only over $1.7 trillion for 2022.

This is because of a downward revision to the housing forecast and decrease dwelling gross sales worth information for the second quarter.

The forecast for 2023 buy mortgage quantity stays largely unchanged at slightly below $1.7 trillion.

84% of Householders Have Mortgage Charges at Least 1% Beneath Present Charges

Whereas an increase in refinance demand is predicted if mortgage charges do in truth fall again into the 4% vary, it may not be sufficient to avoid wasting many lenders.

The reason being most householders have charges not less than 100 foundation factors under prevailing charges, per Fannie.

That is based mostly on Freddie Mac’s latest common of 5.22% for a 30-year fastened. So a full 84% of mortgage holders have charges of 4.22% or decrease.

In different phrases, they in all probability aren’t refinancing anytime quickly, if ever. On the identical time, this “lock-in” impact means in addition they in all probability received’t transfer.

That ought to maintain dwelling costs propped up, even when there may be some downward stress on the housing market total.

On the identical time, decrease mortgage charges in 2023 might assist many latest dwelling patrons snag a decrease fee.

That is why it might make sense to take out an adjustable-rate mortgage whereas fastened charges are excessive.

And when you’re at it, chances are you’ll not wish to pay low cost factors if the hope is to refinance inside a yr. In any case, you received’t wish to pay upfront for financial savings you by no means truly see.

In fact, that is if Fannie’s forecast comes true. It’s all the time potential mortgage charges might go the opposite manner too.

House Costs Nonetheless Anticipated to Rise 4.4% Subsequent 12 months

Lastly, regardless of all of the housing market crash discuss, Fannie Mae forecasts a 4.4% rise in dwelling costs in 2023.

In fact, that’s nicely under the tempo of 16% for 2022 and 18.9% for 2021. It’s primarily flat as compared.

And doubtlessly detrimental when you take into account inflation. However it nonetheless defies the fears of a extreme housing downturn and factors extra to a cooling housing market pushed by affordability.

Keep in mind, tens of millions of householders aren’t going wherever due to their low, fixed-rate mortgages.

And residential builders are sitting on a bunch of empty tons. This limits housing provide, which continues to be close to historic lows regardless of some latest upticks.

So whereas you will notice itemizing costs come down, and bidding wars grow to be much less widespread, property values probably will nonetheless climb greater subsequent yr.

If mortgage charges actually do retreat again to the mid-4% vary, we might even see a scorching housing market subsequent spring.