{kind=link}

The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra info.

In the USA, the median dwelling worth reached $431,000 within the third quarter of 2023. Until they’ve been stockpiling cash, most individuals don’t have sufficient money to buy a house outright. That’s why mortgages exist. That will help you perceive your financing choices while you’re trying to purchase a home, right here’s an summary of the 5 varieties of mortgages obtainable to residential consumers.

What’s a mortgage?

A mortgage is a kind of mortgage used to buy actual property. In case you don’t repay the mortgage as agreed, the lender has the appropriate to take the property from you, promote it and use the cash from the sale to cowl your stability. It is a course of often known as foreclosures.

While you’re purchasing for a mortgage, it’s essential to grasp the terminology utilized by actual property brokers, brokers and different professionals.

Principal is the amount of cash you borrow. For instance, if you might want to borrow $380,000 to cowl the price of a house, you may have a principal stability of $380,000.

Curiosity is the price of borrowing cash. It’s often expressed as a proportion, for instance, 5.8 p.c. A excessive rate of interest may improve your whole value of possession by a whole lot of hundreds of {dollars}, so it’s essential to buy round for the very best charges.

Your mortgage time period is how lengthy you must pay again the mortgage. The 2 commonest mortgage phrases are 15 years and 30 years. So, for instance, you probably have a 30-year mortgage, you may have 30 years to pay again the principal stability.

While you store for a mortgage, you additionally want to consider your month-to-month cost. In lots of circumstances, you’re required to place property taxes and householders insurance coverage premiums into an escrow account. If this is applicable to your state of affairs, your month-to-month mortgage cost shall be larger to account for insurance coverage and taxes.

5 varieties of mortgages

Though each mortgage has the identical primary goal, various kinds of mortgages tackle totally different conditions. Listed here are the 5 commonest.

Typical

A traditional mortgage is a mortgage that’s not a part of a authorities program. You get this sort of mortgage via a non-public financial institution or credit score union. One of many fundamental benefits to getting a standard mortgage is you don’t need to pay for personal mortgage insurance coverage should you make a down cost of at the least 20 p.c of the acquisition worth of the house.

Personal mortgage insurance coverage is a kind of insurance coverage that protects your lender within the occasion you default in your mortgage. It’s important to pay additional for PMI, so avoiding it’s a good solution to hold your prices as little as potential.

One of many main drawbacks of standard mortgages is that they have stringent credit score necessities. You typically want a rating of at the least 620, making standard loans a poor match for subprime (scores starting from 580 to 619) or deep subprime (scores under 580) debtors.

Conforming

Each conforming mortgage should comply with (conform to) the requirements set by Fannie Mae and Freddie Mac, that are dwelling mortgage companies backed by the U.S. authorities. Each companies present funds to banks, making extra mortgages obtainable to American shoppers.

To evolve to the Fannie Mae and Freddie Mac requirements, lenders should vet mortgage candidates fastidiously. This implies you typically want respectable credit score to qualify. You additionally want an appropriate debt-to-income ratio. This ratio compares your month-to-month debt funds to your gross month-to-month revenue to verify your estimated mortgage cost isn’t too excessive.

The principle disadvantage of a conforming mortgage is that there’s a restrict to how a lot you may borrow. The Federal Housing Finance Company has introduced that the 2024 baseline mortgage restrict for a single-family dwelling is about at $766,550. In areas with a excessive value of dwelling, the mortgage restrict for a single-family house is $1,149,825.

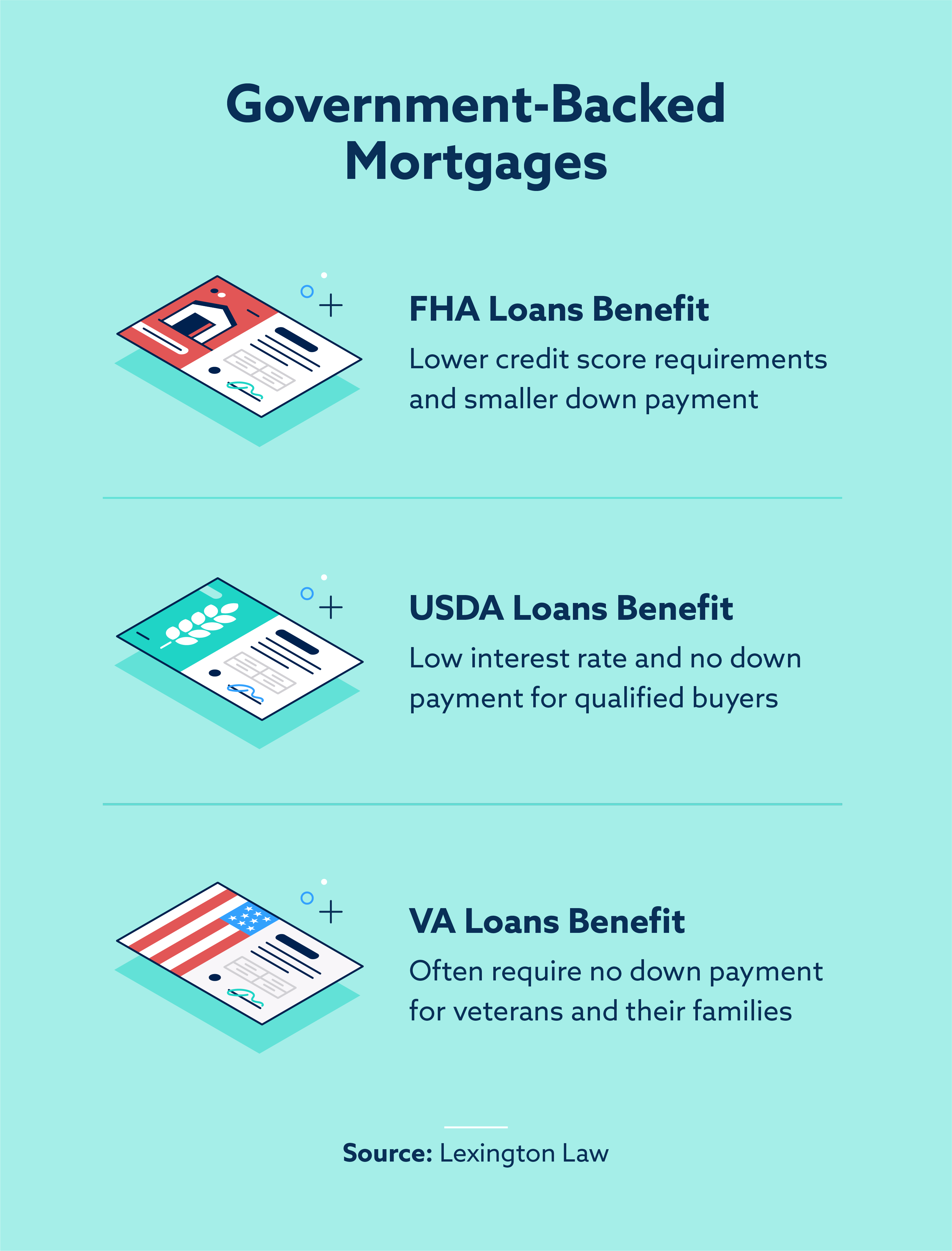

Authorities-backed

A government-backed mortgage is insured by the federal authorities, however it’s issued by a non-public lender, supplying you with the very best of each worlds. One of many greatest benefits of government-backed loans is that banks view them as much less of a threat than different varieties of loans. Subsequently, you could get accredited even when your credit score rating is just too low for a standard mortgage.

One potential disadvantage is that you will have to pay for personal mortgage insurance coverage should you can’t afford to place down 20 p.c on a house. This will increase the overall value of buying.

These are the three commonest varieties of mortgages backed by authorities companies:

- VA loans: To thank veterans and present members of the army for his or her service, the Division of Veterans Affairs backs loans for eligible service members. The most important benefit of getting a VA mortgage is that you simply don’t all the time need to make a down cost. You do want to fulfill sure lending necessities, nevertheless.

- FHA loans: The Federal Housing Administration backs some loans to make it simpler for Individuals to buy their properties. In case you qualify for an FHA mortgage, you could possibly put down as little as 3.5 p.c. FHA loans are additionally obtainable to shoppers with scores under 580, making them a lovely various should you can’t qualify for a standard mortgage attributable to your credit score historical past.

- USDA loans: The U.S. Division of Agriculture backs loans made to debtors in rural areas. To qualify, you have to meet the minimal revenue and credit score necessities.

Curiosity-only

An interest-only mortgage is a particular sort of adjustable-rate mortgage (you’ll study extra about adjustable charges within the subsequent part). Through the first few years, you don’t pay again any of the principal stability. As an alternative, you simply pay the curiosity.

After this preliminary interval, you start paying the principal and the curiosity. Because the fee is adjustable, it adjustments annually primarily based on market situations.

The principle benefit of an interest-only mortgage is that you’ve got a low cost for the primary few years. That stated, your cost will go up finally. Your rate of interest may additionally improve considerably.

Jumbo

Jumbo mortgages are perfect for debtors dwelling in areas with very excessive prices of dwelling. For instance, it’s powerful to discover a dwelling within the Los Angeles space that prices lower than $1 million. You may not get very far with the conforming mortgage mortgage restrict.

A jumbo mortgage means that you can borrow greater than the conforming restrict set by Fannie Mae and Freddie Mac. As a result of amount of cash concerned, your lender might require wonderful credit score and a low DTI ratio. It might additionally take longer to get accredited for this sort of mortgage.

How does curiosity work on a mortgage?

Lenders provide fixed-rate mortgages and adjustable mortgages. A set-rate mortgage is precisely what it seems like—a house mortgage with a hard and fast rate of interest, a fee that stays the identical for all the mortgage time period.

The principle benefit of a fixed-rate mortgage is that you realize precisely how a lot you’ll pay each month. You don’t need to play guessing video games primarily based on adjustments available in the market. That stated, should you apply for a mortgage when charges are excessive, you’ll be locked into the identical fee until you refinance your mortgage.

An adjustable-rate mortgage has an rate of interest that goes up and down. In case you apply when charges are excessive, there’s an opportunity the speed may go down sooner or later. Nevertheless, there’s additionally an opportunity your fee will go even larger, growing your month-to-month cost past what you may comfortably afford.

Ideas for getting the very best mortgage phrases

To maintain your prices in examine, comply with these tricks to get the very best mortgage phrases obtainable:

- Save up: Save as a lot as you may for a down cost. The extra money you set down, the much less you must borrow.

- Store round: You don’t need to go together with the primary lender you discover. Take time to match charges and discover the very best deal to your state of affairs.

- Clear up your credit score: Some varieties of mortgages are solely obtainable to shoppers with good credit score. If in case you have low scores, work to extend them earlier than you apply for a house mortgage.

In case your credit score is holding you again from the house of your goals, don’t despair. The crew at Lexington Regulation could possibly assist by addressing any inaccurate damaging objects listed in your credit score stories.

Word: Articles have solely been reviewed by the indicated legal professional, not written by them. The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained inside the website don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.