{kind=link}

The knowledge offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra info.

The 7 commonest FCRA violations are withholding notices, privateness violations, requesting report for impermissible functions, failure to observe correct debt disclosure procedures, furnishing and reporting inaccurate info, furnishing and reporting previous info, and mixing information.

Key takeaways

- If a client reporting company (CRA) mixes your information with one other client’s, that counts as an FCRA violation.

- As much as $1,000 in damages might be awarded for FCRA violations.

- FCRA violations fall into two classes: willful and negligent.

In 2023, the Client Monetary Safety Bureau obtained about 1,657,600 complaints from individuals regarding errors of their credit score reviews. Congress created the Honest Credit score Reporting Act (FCRA) in 1970 to assist shoppers towards unfair credit score reporting practices. Discovering FCRA violations in your report can lead to optimistic adjustments to your credit score rating.

Under, we’ll discover seven widespread FCRA violations on this information and break down your credit score reporting rights. After studying, you’ll know what to look out for in your credit score report, and also you’ll have extra credit score restore assets to dispute inaccuracies.

What’s the Honest Credit score Reporting Act (FCRA)?

The Honest Credit score Reporting Act is a invoice created by Congress to guard shoppers’ credit score info for different events. By requiring FCRA compliance, the federal government reduces the chance that knowledge in your credit score report can hinder your makes an attempt to seek out work, purchase a home and pursue a greater high quality of life.

7 Honest Credit score Reporting Act Violations defined

Listed below are the seven commonest Honest Credit score Reporting Act violations, together with recommendations on tips on how to treatment these violations as soon as they’ve been recognized.

1. Withholding notices

As a client, you’re entitled to know the way your credit score info is reported, dealt with and utilized by a credit score bureau. In case you aren’t correctly knowledgeable of how your knowledge is getting used, a violation happens.

The next actions are thought of withholding a discover:

- A creditor refuses to inform you of your proper to dispute inaccurate credit score info

- A creditor fails to offer you your credit score info when it’s used to make a credit score resolution

- Collectors don’t notify you when unfavourable credit score info (like repeated late funds) is provided to client reporting businesses (CRAs)

Backside line: An FCRA violation happens when credit score bureaus don’t talk how your credit score info is getting used.

2. Privateness violations

Your info ought to solely be shared with approved individuals or entities which have demonstrated a legitimate want to your credit score info.

Entities that sometimes have a justifiable motive to see your credit score info embody:

- Landlords, to see you probably have a sample of creating funds on time

- Bank card firms and lenders, to find out should you’re a accountable borrower

- Insurers, to make it possible for you’ll be able to make accountable monetary choices

Credit score bureaus are usually cautious to not share your credit score report with unauthorized events. In case your info is mishandled, nevertheless, you could be entitled to damages.

Backside line: Choose events are entitled to your credit score info below particular circumstances. Mishandling delicate info is taken into account an FCRA violation.

3. Requesting a credit score report for an impermissible function

A credit score bureau could violate the FCRA if they provide your credit score info to somebody for an impermissible function.

Impermissible functions would come with:

- An employer who pulls your credit score info with out written permission

- A creditor that pulls your report back to examine in your present monetary standing for no offered motive (reminiscent of a current software for a brand new bank card)

- An employer requests your credit score report with out your specific permission

Backside line: Entities that require your credit score report with no legitimate motive threat violating the FCRA.

4. Failing to observe correct debt dispute procedures

The FCRA requires businesses to deal with credit score disputes in very particular methods. That features conducting an affordable investigation of your dispute, modifying and correcting any discovered inaccurate info, and eradicating the disputed merchandise out of your credit score report inside 30 to 45 days after receiving discover.

Generally, a credit score bureau can neglect all or any of those obligations, that means they’ve violated correct debt dispute procedures.

Backside line: Failing to deal with credit score disputes in a well timed and correct trend counts as an FCRA violation.

5. Furnishing and reporting inaccurate info

Entities like bank card firms or mortgage collectors mustn’t deliberately provide incorrect info to a CRA below any circumstances.

Some examples of reporting inaccuracies embody:

- Overstating or misstating whole balances due

- Reporting a debt that has been paid off as a charge-off

- Reporting funds paid on time as late

- Mistakenly itemizing you as a debtor on an account

Backside line: Collectors mustn’t deliberately give inaccurate info to CRAs.

6. Furnishing and reporting outdated info

In case you discover the knowledge in your credit score report is just not up to date after a change in your credit score (like an account being closed), this could possibly be in violation of the FCRA.

Examples of this sort of FCRA violation embody:

- Reporting info older than seven to 10 years previous

- Failing to report debt as being discharged in chapter

- Reporting previous money owed as present

- Reporting a closed account as being nonetheless lively

Backside line: Collectors or CRAs failing to replace your credit score info violates the FCRA.

7. Mixing your information with one other get together’s

In some cases, a credit score bureau can mistakenly “combine” your file with that of one other particular person with related info. This violates the credit score bureau’s obligation to report correct credit score details about each borrower.

Blended file violations embody combining credit score info of individuals with related names dwelling in the identical space, reminiscent of if there are two individuals named “John Smith” who stay in the identical zip code, or not together with “Jr.,” “Sr.,” “II” or different variations for individuals with related surnames.

Backside line: Mixing credit score info between two related accounts is taken into account an FCRA violation.

What are your rights below the Honest Credit score Reporting Act?

Each client within the U.S. has sure protected rights below the FCRA. Under, you’ll discover a abstract of what these rights embody.

|

The FCRA Proper to: |

Examples |

|---|---|

|

Know if info in your credit score file is used towards you |

Getting denied new credit score primarily based on earlier late funds reported by TransUnion |

|

Ask for a credit score rating |

Asking to your credit score rating earlier than making use of for a mortgage |

|

Know what info is in your file |

Had been you denied a mortgage primarily based on current bank card purposes |

|

Get hold of a safety freeze |

Contacting credit score bureuas to freeze your account |

|

Dispute inaccurate info |

Disputing a paid off card that’s nonetheless in your report |

|

An correct, full and verifiable credit score report |

Equifax updating a report inside 30 days of discovering inaccuracies |

|

An up-to-date credit score report |

A chapter 7 chapter have to be eliminated after 10 years |

|

Restrict unsolicited affords primarily based in your credit score report |

Receiving too many affords for preascreened playing cards |

|

Restrict entry to your credit score file |

Different events can solely view related knowledge in your report |

|

Require consent for employers to view your reviews |

Interviewers should acquire consent earlier than viewing your report |

|

Search damages from violators |

Suing if an FCRA violation impacts you |

Suing for damages after an FCRA violation

From a authorized perspective, “damages” discuss with reparations that an individual seeks after they’ve been negatively affected by one other get together. If an FCRA violation by one other get together ends in misplaced funds or hurt to your popularity, you may search damages in court docket.

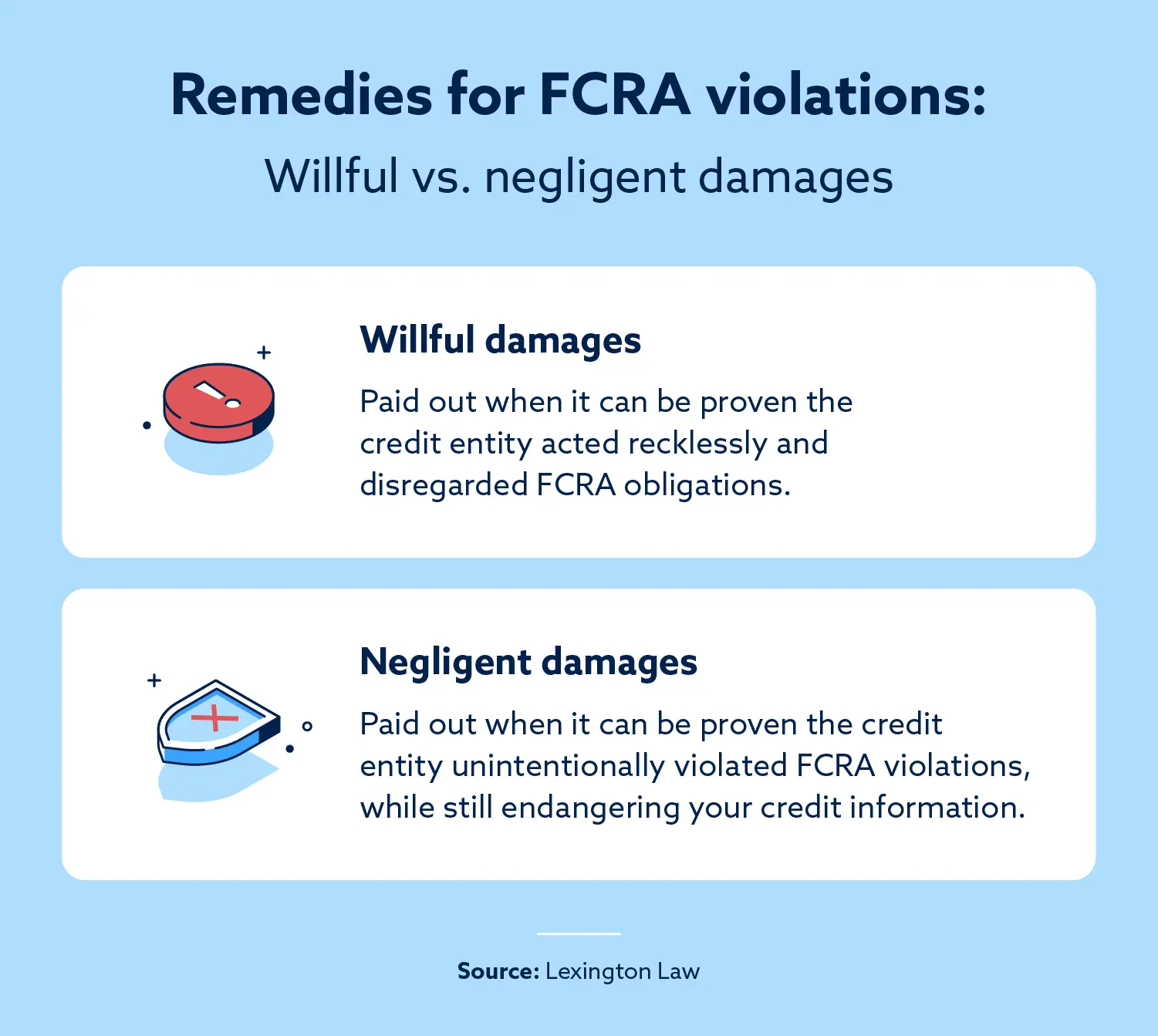

When you’ve recognized that the Honest Credit score Reporting Act has been violated by a CRA or one other credit score entity, you’re capable of sue that entity in court docket for one among two sorts of damages: willful or negligent violation.

Willful violation

A willful violation means you may show that the CRA or credit score entity acted recklessly together with your info and didn’t respect their obligations, each to the FCRA and your protected rights below the FCRA.

This doesn’t imply you and your lawyer need to show past an affordable doubt that the entity deliberately violated your rights — simply that they did so within the first place and that they need to have identified to not accomplish that.

In case you can show this in court docket, you could possibly recuperate the next damages:

Fundamental damages:

- Provable damages with no set restrict, or

- Statutory damages between $100 and $1,000

- Punitive damages as determined by the court docket

- Lawyer charges and prices

Damages from a person violator who lied or used your credit score report for an improper function:

- Provable damages with no set restrict, or

- $1,000 flat

- Punitive damages as determined by the court docket

- Lawyer charges and prices

Negligent violation

A negligent violation means the CRA or credit score entity violated your rights below the FCRA with out figuring out they did so or with out that means to.

In case you’ve recognized and confirmed negligent violations relating to your credit score, you could be entitled to the next damages:

- Precise damages with no set restrict or minimal

- Lawyer charges and prices

Earlier than you name your lawyer, you need to be conscious that there’s a penalty for an pointless, or “frivolous,” FCRA lawsuit that may include a hefty effective — you’ll have to pay the opposite get together’s lawyer charges if it’s discovered your go well with was filed in dangerous religion or for functions of harassment.

Let Lexington Regulation Agency Assist You Dispute Credit score Errors

Examine any suspicious info in your credit score report, as they could change into errors incurred by FCRA violations. If that’s the case, contact Lexington Regulation Agency to get assist disputing these inaccuracies. Be taught extra about our companies to see how one can problem errors extra efficiently.

Observe: Articles have solely been reviewed by the indicated lawyer, not written by them. The knowledge offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained inside the web site don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.