{kind=link}

Sound the alarm. A extreme housing downturn could now be within the playing cards in the USA.

That’s, when you consider the most recent commentary from credit standing company Fitch Rankings.

To be clear, they really stated “the probability of a extreme downturn in US housing has elevated.”

They nonetheless consider such a state of affairs is just not possible, and as a substitute we’ll see a extra average pullback within the housing area.

That principally impacts dwelling builders, who’re already struggling, although it might result in a decline in dwelling costs.

Actual Property Crash vs. Correction vs. Housing Recession

There’s been plenty of negativity within the housing market these days, as I stated there can be some time again.

We have now entered a detrimental information cycle relating to actual property, mortgage charges, and the economic system at massive.

Again in June, economist Mark Zandi of Moody’s, one other credit standing company, stated we had been in a housing correction.

What he meant by that was that we lastly arrived on the tail finish of the housing increase. In different phrases, the great days had been over.

This was principally led by a doubling in mortgage charges, creating an affordability disaster that stalled dwelling value beneficial properties.

Nonetheless, many market watchers consider dwelling costs will proceed to rise, no less than nominally. As soon as factored for inflation, they is likely to be flat or technically decrease.

And naturally, sure markets shall be impacted greater than others, particularly those who noticed unsustainable run-ups over the previous a number of years.

Additionally this week, the Nationwide Affiliation of Residence Builders (NAHB) stated increased development prices have ushered in a “housing recession.”

What this implies is much less housing begins, value reductions, flagging demand from potential dwelling consumers, and fewer dwelling gross sales.

So to tally it up, we’ve acquired a housing correction and a housing recession, and the worry of an actual property crash on the horizon.

Many People Really Need a Housing Crash So They Can Purchase a Residence

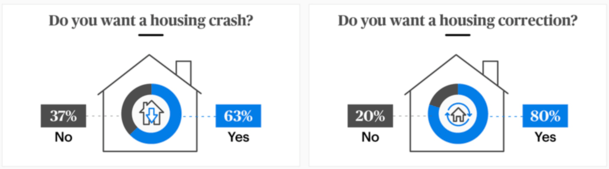

Curiously, many People need a housing crash, per a 1,000-person survey from ConsumerAffairs.

The corporate discovered that 78% consider the housing market will crash quickly and 63% need it to.

If we’re speaking only a housing correction, 80% need one. General, 27% choose a housing correction over a housing crash.

This is able to enable for a gradual pullback in dwelling costs, permitting new consumers to enter the market with out placing current homeowners susceptible to shedding their properties.

Gen Z need a housing crash (84%) or correction (86%) greater than every other era to allow them to buy a house.

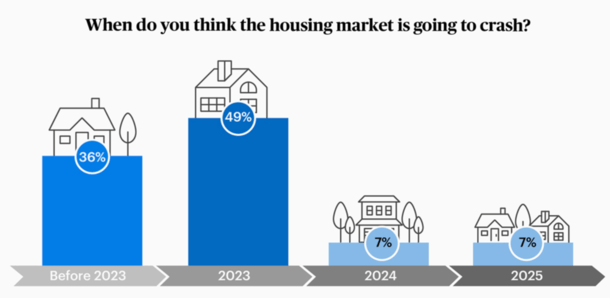

As to when this might all occur, 36% consider a crash will happen earlier than 2023, with 49% calling a 2023 crash.

For a very long time, I’ve referred to as a 2024 peak in actual property, based mostly on historic cycles that return a pair hundred years.

However I’ve questioned an enormous downturn, as produce other economists like Zandi, pointing to key buffers available in the market.

These embody a scarcity of housing provide, high-quality mortgages (most homeowners have 30-year mounted loans) with rock-bottom rates of interest, and a scarcity of hypothesis.

If we issue within the notion of a housing recession the place dwelling builders cease establishing new properties, that places additional pressure on provide constraints.

So in a way, it means even fewer accessible properties, which might bolster property values and defend us from a extreme housing downturn.

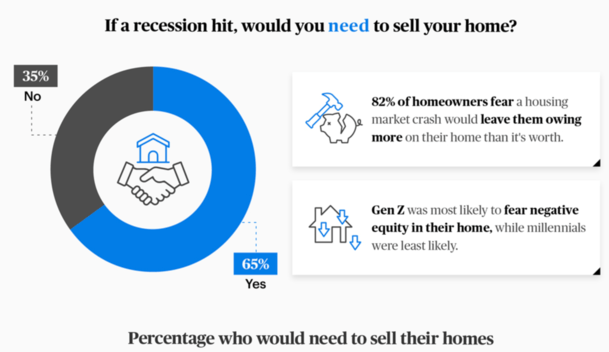

Almost Two-Thirds Would Must Promote Their Residence If a Recession Hit?

Whereas I do consider as we speak’s housing market is way, a lot completely different than the one seen in 2006-2007, we nonetheless must be on the defensive.

For instance, some 65% of householders would apparently “have to promote” if a recession hit. By the way in which, we’re sort of already in a recession.

Assuming that truly occurred, which I don’t purchase into, the actual property market would seemingly crash.

In spite of everything, we’d see a flood of distressed gross sales, comparable to brief gross sales and foreclosures, hit the market.

This is able to be a state of affairs similar to what was seen again in 2008, which sparked the Nice Recession.

However once more, I think most householders as we speak can climate the storm higher due to their low fixed-rate mortgages. And their sizable dwelling fairness positions.

Again then, householders had been grappling with falling dwelling costs, adjustable-rate mortgages resetting increased, and a complete lack of dwelling fairness, and infrequently instances underwater mortgages.

Moreover, three in 4 respondents stated they’d purchase a house if the market crashes, which limits the draw back threat.

For this reason I nonetheless consider a housing correction is extra within the playing cards, during which dwelling costs merely cool off.

And once more, when you think about inflation, dwelling costs could not even fall nominally in plenty of locations.

Additionally observe that each one this worry and loathing is occurring at a historically gradual time of 12 months for the housing market. And mortgage charges could go down once more.

To sum issues up, I consider the housing market acquired method forward of itself these days and is correcting again to a extra balanced place.

This implies fewer bidding wars, the return of contingencies, and extra cheap itemizing costs. It doesn’t imply a hearth sale and even essentially a very good deal on a house.