{kind=link}

Fintech is posing an ever-increasing downside to monetary establishments nonetheless reliant on legacy constructions.

Till now, conventional finance has managed to stave off fintech’s disruptive forces, counting on their a long time of multinational to put in belief and an air of stability for the buyer. However there are indicators that that is beginning to change.

“The power to quickly innovate and iterate is quick changing into a aggressive differentiator,” wrote Aite-Novarica Group in a report. “Nonetheless, the demand for innovation poses a major useful resource administration problem. One made worse by monetary establishments’ ongoing reliance on legacy structure and an especially aggressive marketplace for technical employees.”

Banks have, for a while, seen a drain on client deposits, and it appears that evidently fintechs are making up the distinction. A brand new report by Cornerstone Advisors discovered that to this point this yr, fintechs have managed to seize 47% of recent checking account openings.

“Established monetary providers and insurance coverage corporations are dealing with an ideal storm of challenges, together with nimble fintech startups, legacy core platforms that aren’t sufficiently agile to assist fashionable imperatives equivalent to digital transformation, personalization, and fast software improvement, and stress to modernize core platforms safely and securely,” mentioned Teodor Blidarus, CEO and co-founder, FintechOS.

One strategy might be to accomplice with fintechs, which might deliver scalability. Nonetheless, it may be a protracted, multi-step course of that requires in depth negotiation and, in some instances, an overhaul of organizational processes to accommodate the brand new addition.

For those who choose to proceed in-house, a reevaluation of the core infrastructure is essential to sustaining modern prowess.

Legacy Techniques Substitute: the silver bullet?

The legacy programs of those establishments pose a major subject when competing with fintechs. Outdated code and layers of the community create friction, a key drawback when competing with fintechs which might rapidly evolve to fulfill client wants.

In line with Capgemini in its World Retail Banking Report 2022, “Structural challenges preserve most banks from totally leveraging data-driven analytics to draw prospects and develop relationships.”

In response to Capgemini’s survey, 95% of monetary establishments mentioned outdated legacy programs and core banking modules inhibit efforts to optimize data- and customer-centric progress methods. As well as, 80% agreed that underdeveloped information capabilities hinder buyer lifecycle course of enhancements. Over two-thirds mentioned they’ve difficulties figuring out new buyer segments, and half reported problem in offering seamless onboarding experiences.

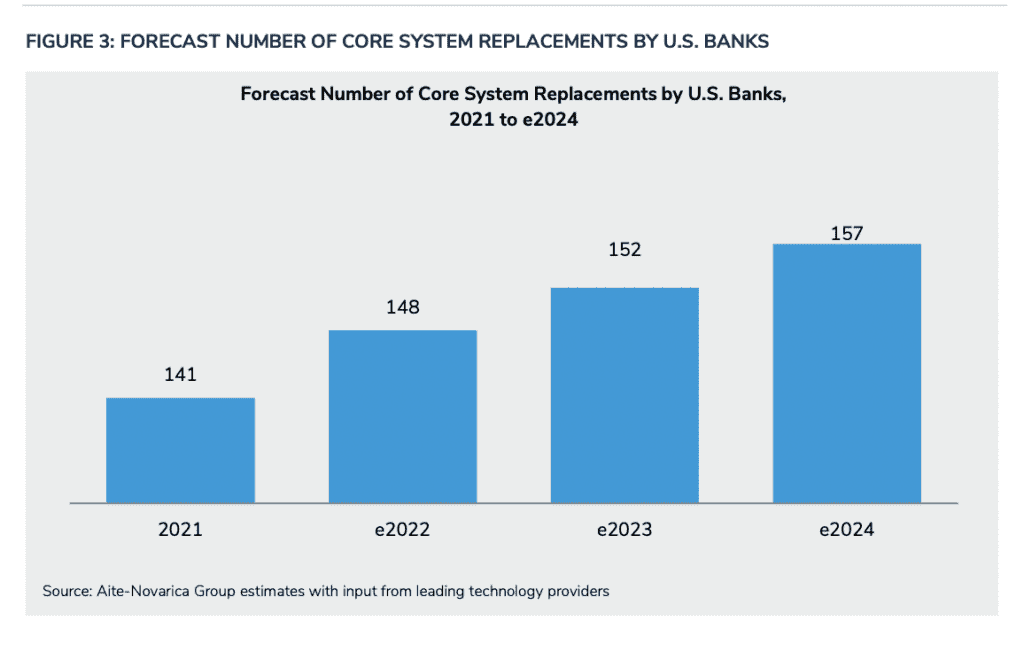

A solution to the problems with core constructions could be to “simply” substitute them. Core system replacements are rising every year, however based on McKinsey, solely 30% succeed.

The change requires vital useful resource allocation, and as a result of complexity, important components are sometimes missed.

“Particularly, core modernization applications that inadequately plan for connectivity and interoperability throughout the financial institution stack decrease their effectivity and effectiveness in driving innovation. This notably consists of connectivity to more and more essential third-party fintech ecosystems, in addition to the important buyer engagement layers that each one FIs depend on,” wrote Aite Novarica.

Nonetheless, the train is unavoidable, and as know-how improvement speeds on, core structure stays additional and additional behind.

“Now’s the time for banks to modernize core banking,” says Jerry Silva, vp of IDC Monetary Insights’ Worldwide Banking Digital Transformation Methods program. “Between fashionable know-how approaches like microservices and APIs and the usage of cloud platforms making certain scalability and resiliency for the financial institution’s again workplace, banks would do properly to begin the journey to core system modernizations immediately.”

So what’s the answer?

Every core system is, sadly, distinctive, which means the technique needs to be personalized.

In line with Aite Novarica, At present, there are three basic approaches, every with its personal challenges:

- “1 – Full “rip-and-replace” of present core infrastructure: Large-bang approaches to core alternative can successfully deploy new fashionable capabilities however are intensive, resource-heavy tasks with very excessive ranges of danger. This consists of the potential for tasks to spiral out in value and timescale and as threats to service ranges for present shoppers.

- 2 – Greenfield launch: Sometimes involving cloud-based platforms, these rollouts contain FIs working a greenfield tech stack that operates parallel to present financial institution infrastructure. New shoppers are onboarded into the greenfield core, whereas older shoppers are later migrated to the brand new platform. This strategy can result in vital disruption for present shoppers and requires a pricey doubling of sources on account of working parallel operations.

- 3 – Wrap-around, or core-hollowing: This strategy usually makes use of containerized programs, or a microservices strategy, to deploy fashionable capabilities piece by piece, with the choice of outright core alternative sooner or later. Whereas dangers are diminished, this strategy requires supporting a viable legacy core system for a number of years, lengthening the time for the general core modernization course of. Moreover, FIs should prioritize areas for modernization, and so they incur dangers on account of vital customization, creating new types of legacy know-how issues.”

Nonetheless, new options are being developed.

RELATED: Generative AI in fintech goes far past the ChatBot

One many are turning to is the usage of fintech enablement methods.

A fintech enablement platform is an infrastructure that acts as an working system for innovation. Decreasing the complexity of launching modern tasks, it’s made up of prebuilt and modifiable elements many occasions utilizing low-code approaches. These could be deployed in a extra agile and responsive methodology than most conventional improvement cycles.

Whereas it isn’t an answer to the tangled net of core infrastructure, it could actually present a extra streamlined strategy to innovation.