{kind=link}

Over the previous a number of years, we’ve been completely centered on excessive mortgage charges.

The 30-year mounted surged from sub-3% ranges to round 8% within the span of lower than two years.

This clearly acquired the eye of everybody, whether or not it was the media or on a regular basis People.

However usually it felt like residence costs had been overshadowed by rates of interest, regardless of additionally surging greater.

In the USA, residence costs have risen practically 50% since simply 2019, and have mainly doubled since bottoming a decade in the past.

We’re Centered on Mortgage Charges, However What About Residence Costs?

I get it, the rise in mortgage charges was unprecedented. Whereas they solely went as much as round 8% this cycle, the rise in such a brief interval is record-breaking stuff.

For context, the 30-year mounted went from about 3% to eight%, which is a 167% acquire, from early 2022 to late 2023. That’s a particularly small window of time to see such a rise.

Conversely, the Eighties mortgage charges went from 9% to 18%, solely a 100% enhance. And it took 4 years. They solely didn’t keep that prime for quite a lot of months earlier than retreating again to the low teenagers.

Both approach, it’s clear mortgage charges have been high of thoughts for everybody due to this dramatic rise.

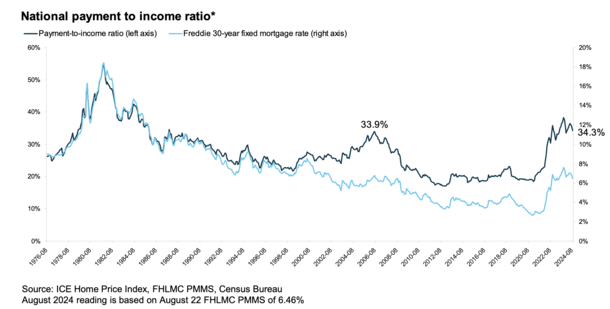

And the upper charges have had actual implications. Housing affordability was traditionally okay previous to the mortgage charge run-up, however rapidly surpassed the early 2000s housing bubble peak late final yr, per ICE (see chart under).

Affordability has since improved a bit as charges have decreased, nevertheless it stays fairly poor and utilizing 2008 as a yardstick in all probability isn’t prudent.

However the level I’m attempting to get at right here is it’s not simply the charges. As I identified final week, we have now a excessive mortgage quantity downside as properly.

Let’s Take into account a Residence That Is At present for Sale Close to Me

I acquired the concept for this submit after receiving a textual content message a few residence on the market close by.

It was a kind of unsolicited textual content messages from an actual property agent promoting their itemizing.

These at all times pique my curiosity as a result of they supply a fast housing market temperature.

The property in query is promoting for about $1.7 million, which instantly appeared steep for the realm. Nevertheless it’s additionally not an outlier given how a lot costs have risen.

The breakdown on Redfin was a month-to-month PITI cost of roughly $11,200. That assumed a 20% down cost (solely about $340k!) and a 7% 30-year mounted mortgage charge.

One you throw in owners insurance coverage and property taxes, you’re a fairly steep five-digit cost. Ouch!

Now I needed to get context so I checked out properties close by the topic, and located one which was backed as much as it and pretty comparable.

Positive, not as up to date and a bit smaller, however nonetheless shut sufficient for me. The present owners bought it in 2015 for about $750,000.

Proper off the bat, we’re speaking a few property that’s double in value, regardless of backing as much as each other and being pretty comparable.

Meaning the rise in PITI goes past only a greater mortgage charge. And don’t overlook the large down cost both.

The identical 20% down on the comparable property was simply $150,000. As for the PITI, solely $3,700!

That’s a distinction of $7,500, or a proportion enhance of 200%!

Evaluating Month-to-month Funds Throughout Completely different Mortgage Charges

| $1.7M Residence Buy | Month-to-month PITI |

| 7% charge | $11,200 |

| 6% charge | $10,300 |

| 5% charge | $9,450 |

| 4% charge | $8,700 |

Let’s simply ignore the truth that the worth is the worth and have a look at totally different funds with numerous mortgage charges.

On the 7% 30-year mounted that Redfin is utilizing by default, the month-to-month PITI is $11,200. We knew that already.

However what a few charge of 6%? Nonetheless a whopping $10,300 per 30 days, or practically triple the comparable property.

At 5% we get a month-to-month housing cost of $9,450. At the least it’s not within the double-digits anymore, proper?

And at last, at a charge of 4%, which is fairly darn low, the PITI continues to be $8,700 per 30 days! That’s nonetheless 135% greater than the comp residence.

So mainly if mortgage charges returned to near-record lows, the cost continues to be fairly astronomical in comparison with the house purchaser who bought a like property lower than a decade earlier.

If you wish to say hey, it’s been practically 10 years, that’s an unfair comparability. I see comparable properties bought in 2017, 2018, and 2019 for about $850,000 or $900,000.

Merely put, residence costs alone have put affordability out of attain for a lot of. And the upper mortgage charges we’re simply an insult to damage.

Do We Have a Excessive Residence Value Drawback?

As illustrated, even a 4% mortgage charge doesn’t carry mortgage funds down sufficient to make a house buy inexpensive for a lot of.

Paying practically $9,000 per 30 days whereas your neighbor is paying $3,700 appears fairly ridiculous.

So the subsequent most blatant place to look is residence costs. However we all know that residence costs are sticky and infrequently fall, at the least on a nominal (non-inflation adjusted) foundation.

This implies it’s onerous to get a lot reduction there except there a significant uptick in provide, which may result in decrease costs.

However that brings up the opposite cause why residence costs are so excessive to start with. There was a extreme lack of present residence provide for years in lots of markets nationwide.

And it solely grew worse when mortgage charge lock-in reared its ugly head. The one shiny spot is likely to be rising wages, which take some chunk out of the worth enhance.

Nonetheless, it’s not sufficient by itself. You want all three parts to revive affordability, together with charges, costs, and wages.

Positive, mortgage charges and residential costs can come down collectively, and so they may have to as a way to restore affordability.

Learn on: It’s now not a mortgage charge story.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on Twitter for warm takes.