{kind=link}

The worldwide rise in digital funds has introduced with it a booming marketplace for digital playing cards.

Pushed by the continuing adoption of smartphones, evolving cost applied sciences, and a want for elevated safety, the worldwide digital card market is anticipated to achieve a price of $9.1 trillion by 2027. If realized, this may characterize a 280% development from 2022, the place the market dimension was discovered to be $2.4 trillion

In accordance with a Mastercard Fee Index report, in Could 2021, 93% of surveyed customers used and most well-liked rising cost strategies involving the usage of biometrics, digital currencies, and QR codes, along with contactless cost. Because of this, cost suppliers are growing different options.

Digital playing cards have offered customers with an simply accessible, easy-to-manage different to the bodily card. Digitally centric, it permits the consumer to simplify the cost course of, in addition to handle options akin to spending limits seamlessly.

Juniper Analysis has discovered that B2B funds are more likely to be the following driver of development for digital playing cards. The sector, already accounting for a big portion of digital playing cards’ international transaction quantity, is predicted to make up 71% of the worth by 2026.

Nevertheless, companies, and their accounts receivable (AR) groups, have been met with a difficulty with the elevated digitization of funds. Whereas 90% of suppliers have mentioned that they like digital funds, the velocity has turn out to be overwhelming for a lot of in a panorama of majoritively guide processes.

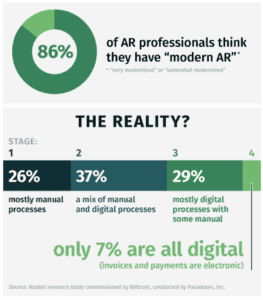

Accounts Receivables in digital card future

In accordance with a research carried out by Billtrust, nearly half of the surveyed organizations ship between 10,000-25,000 per thirty days. AR groups spend essentially the most time on money software and reconciliation, credit score, collections, funds, and invoicing.

Regardless of the vast majority of AR groups stating that their processes are “modernized,” many proceed to function inside a primarily guide atmosphere. The research discovered that over 60% should not have a majority of their funds or invoices as digital, with practically 30% of funds nonetheless being money and paper checks.

As digital cost and digital card adoption proceed their development, with B2B as its flag bearer, this might pose a big situation, weighing groups down with an elevated want for sooner processing that may very well be enormously assisted by automation.

In response, Mastercard, in partnership with Billtrust, launched, on Monday, 25 July, their Receivables Supervisor, immediately focusing on a necessity for improved processing.

The brand new product bypasses the necessity to manually seize and enter digital card particulars to reconcile the huge variety of digital funds acquired.

Card funds from all issuers are consolidated, and the remittance knowledge can routinely be matched to open invoices. It may also be formatted for his or her Enterprise Useful resource Planning (ERP) programs, doubtlessly rising the effectivity and accuracy of bill reconciliation.

“We’re bridging the hole between consumers’ digital card preferences and suppliers’ acceptance challenges by automating guide processes and remodeling the best way accounts receivable groups function,” mentioned Chad Wallace, international head of Business Options at Mastercard.

RELATED: Embedded finance/B2B convergence an essential development: Galileo report