{kind=link}

The S&P 500 (SPY) is flirting with a break under the 200 day transferring common. A part of the story you already know…that concerning the latest speedy rise in bond charges. Sadly there may be an much more ominous a part of this story that must be instructed right now. That’s the reason 43 12 months funding veteran tries to simplify the dynamics behind the possibly looming Debt Supercycle. Learn on under for the total story.

Generally the investing panorama is extremely easy. Like 85% of your lifetime the economic system has been increasing and the inventory market is bullish. After which from that interval of extra a recession comes alongside making a bear market the opposite 15% of the time.

Every is straightforward to see if you find yourself in the midst of that section. Sadly, it’s somewhat harder to know which it’s for positive on the cusp of the place the 2 durations meet. And that’s the place we discover ourselves right now.

On prime of that we have now an financial boogeyman that has been swept underneath the rug time after time that has reared its ugly head as soon as once more. Sooner or later we should pay the piper for this with a long run interval of under development progress and weak inventory costs.

Has that dreadful time arrived?

That and extra can be on the coronary heart of this week’s Reitmeister Whole Return commentary.

Market Commentary

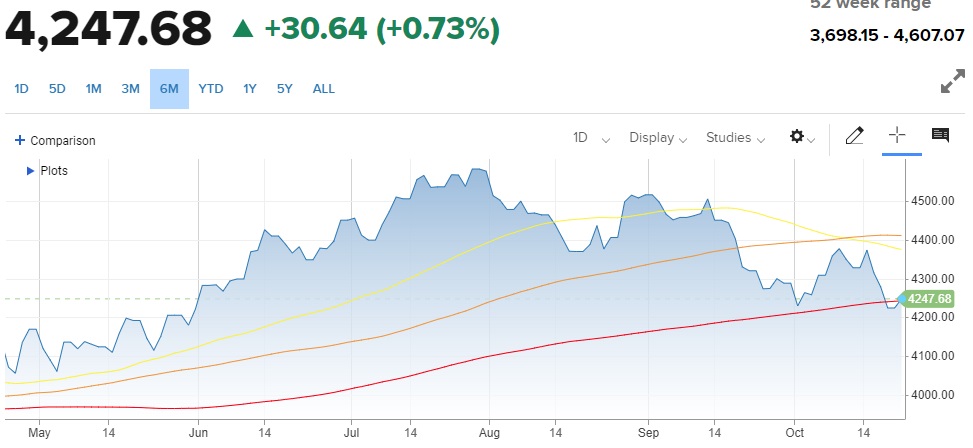

Let’s begin our dialog right now with the precariousness of the technical image for the inventory market.

Transferring Averages: 50 Day (yellow), 100 Day (orange), 200 Day (purple)

The 200 day transferring common for the S&P 500 (SPY) is probably the most very important of the long run development strains. It normal pays to be extra aggressive above that degree…and conversely, to be extra defensive underneath that mark. That’s the reason this week’s tangle with this essential technical degree at 4,237 deserves all of our consideration.

Monday we closed under for the primary time in a number of months. After which Tuesday we climbed again above. That is the second such take a look at of this key degree and as most of you already know dangerous issues usually are available teams of three. That means I doubt that is our final dialog about doubtlessly breaking under.

Due to the above battle and elevated odds we spend a while under this key degree, I’ve moved the Reitmeister Whole Return portfolio right down to 74.5% invested. Arduous to name that bearish by any stretch.

Quite it’s an acceptable dose of warning due to the basic dynamics happening. A few of it has already mentioned in earlier commentaries about how bond charges are “normalizing” again to traditionally common ranges from artificially suppressed ranges.

If that’s the solely issues at play, then probably we’re fairly near the peaks in these bond ranges and bull market ought to resume from right here. (Learn extra about this dynamic in my latest commentary right here)

BUT WHAT IF THIS TIME IS DIFFERENT?

That’s the most harmful expression in all of investing…however at all times one value considering. Particularly as we digest this subsequent subject.

Maybe this isn’t about price normalization, however somewhat the oncoming of the Debt Supercycle.

John Mauldin goes in depth on this subject as soon as once more in his very provocative weekend commentary. Really a should learn you will see that right here.

I’ll strive my greatest to simplify the dialogue with the next.

Far too lots of the world’s governments are overextended with debt. Check out this nation by nation record with the USA coming in with the 9th worst Debt to GDP ratio.

Everyone knows its unsustainable. Sooner or later it should must be paid again But amazingly 12 months after 12 months…and decade after decade we sweep it underneath the rug. Sooner or later the piper will must be paid.

Solely 2 methods to pay it down. And each are horrible for inventory buyers.

Deficit Discount: First, this may by no means occur. Really unhappy however each political events within the US are so beholden to particular pursuits with their arms out, that neither has confirmed any fiscal self-discipline in DECADES. And simply since you steadiness the finances for a 12 months or two…does not actually do something to chop down the $33.63 trillion in debt already collected. And the price of serving that debt is barely going larger by the minute (particularly on this larger price setting).

However pushing again the laughter, lets think about some different universe the place we elect politicians disciplined sufficient to drag this off. WELL that may be a recipe for recession because the Authorities at the moment represents 25% of GDP. So even a modest 5% discount in authorities spending would tilt the economic system into recession. And by the best way…5% ain’t gonna minimize it to make the wanted dent in our mountain of debt.

Whenever you add up the above you respect that this most well-liked path to debt discount remains to be a recipe for catastrophe. So, let’s transfer on to the even worse end result…

Debt Disaster: Think about the Greece scenario from a decade in the past…and now make it about 50X worse. As a result of if the US or Japan begin coming underneath strain it probably could have a domino impact to wipe out the remainder of the weaklings….which is most everybody. That’s the reason some name this the Debt Tsunami.

The 16 12 months interval of ultralow charges we’re rising from was very helpful to those governments to maintain piling on the debt as a result of its fairly simple to pay again at long run charges of 0 to 2%. That occasion is unravelling proper now as famous above.

The principle query is whether or not charges are simply “normalizing” again to extra practical historic ranges…or is that this a extra painful technique of world debtors saying its “time to pay up”.

Sure, we have now been very lucky that we hold avoiding that day of reckoning. However once more…this time might be totally different. In that regard, let me share with you the important thing part from Mauldin’s article on the subject of confidence:

“Maybe greater than the rest, failure to acknowledge the precariousness and fickleness of confidence—particularly in instances wherein massive short-term money owed must be rolled over repeatedly—is the important thing issue that offers rise to the this-time-is-different syndrome. Extremely indebted governments, banks, or firms can appear to be merrily rolling alongside for an prolonged interval, when bang! — confidence collapses, lenders disappear, and a disaster hits.”

Reity, this can be a scary thought…are you saying that is what is going on now?

Most likely not…however it’s not out of the query. Which is why it is acceptable to take a extra conservative method with our investing proper now. Additionally smart to eliminate our positions most tied to larger charges (which we did this morning).

It is a arduous subject for me personally. I completely HATE owing individuals cash. At all times did.

Thus, I’d keep away from borrowing except completely crucial. After which would completely pay again earlier than anybody requested for the cash.

Now you already know why I am not a politician 😉

The purpose being that I’m very delicate on this topic. Nevertheless, it does not actually take a fiscally accountable particular person like myself…or a rocket scientist, to understand that this case is untenable in the long term.

The troublesome half is saying if that disaster of confidence is beginning now. Or we get to kick that may down the highway as soon as once more. However due to the massive query mark lingering on the market, it appears solely acceptable to be extra conservative/defensive in our method.

Do think about this…the US remains to be one of many higher bets for debtors and certain the primary cracks would happen elsewhere…with different extremely indebted international locations.

(See chart under…2nd column is % of debt to nationwide GDP)

My sense is {that a} smaller, extremely indebted participant like Singapore or Italy would present cracks first of their debt. If that occurred, then just like the Greece scenario it could be smart for all of us to honker down in far more defensive portfolios postures in case the dominos hold falling to different international locations just like the US.

Sure, it could create a recession. And sure shares would tumble right into a nasty recession. And it could keep darkish for fairly some time to work its method out.

Gladly we understand how to make earnings in that setting:

Promote all shares > purchase inverse ETFs to rise in worth because the market declines.

However once more…perhaps that isn’t taking place. And we’re simply coping with the extra benign price normalization points. In that case, we should always really feel good that charges have peeled again a notch this week as 2 of the most important bond merchants, Invoice Ackman and Invoice Gross, are each now betting on charges taking place from right here.

Simply so as to add another wrinkle to the story. Additionally it is doable that charges have normalized and that the discount in charges from right here is from elevated concern {that a} recession is coming.

That means the rationale that the Fed is now anticipated to take a seat on their arms for the following two conferences is as a result of the rising of charges exterior of their efforts is little doubt going to sluggish the economic system from the 4% tempo that probably will get introduced on Thursday.

Gladly slowing from 4% provides quite a lot of cushion to not tip over into recession. Simply moderating to 1-2% progress would nonetheless probably be ample backdrop to remain bullish. Sadly historical past reveals many recessions forming proper after a sturdy financial studying.

A slowing economic system just isn’t essentially like a automotive that’s pumping its breaks to slowly ease right into a purple gentle. Usually it’s like slamming the brakes with everybody flying by way of the windshield into the following recession.

Sure, I’m fairly the ray of sunshine right now 😉

Nevertheless, I assumed it was very important to get all of the practical prospects on the desk. And that we’re in wait and see mode for what comes subsequent.

If simply one other in an extended line of false alarms with charges leveling out and economic system rolling ahead, then we’ll get again to 100% bullish quickly sufficient.

Alternatively, if odds of recession, and even worse, whiffs of a debt disaster decide up, then we’ll at first change into extra defensive and in the end bearish with inverse ETFs.

The purpose is that we have to see what occurs after which react in type. Gladly we all know what to do and can react shortly to make one of the best of the scenario.

What To Do Subsequent?

Uncover my present portfolio of 6 shares packed to the brim with the outperforming advantages present in our POWR Rankings mannequin.

Plus I’ve added 3 ETFs which are all in sectors nicely positioned to outpace the market within the weeks and months forward.

That is all primarily based on my 43 years of investing expertise seeing bull markets…bear markets…and all the pieces between.

In case you are curious to be taught extra, and wish to see these 9 hand chosen trades, and all of the market commentary and trades to come back….then please click on the hyperlink under to get began now.

Steve Reitmeister’s Buying and selling Plan & Prime Picks >

Wishing you a world of funding success!

Steve Reitmeister…however everybody calls me Reity (pronounced “Righty”)

CEO, StockNews.com and Editor, Reitmeister Whole Return

SPY shares fell $0.63 (-0.15%) in after-hours buying and selling Tuesday. Yr-to-date, SPY has gained 12.00%, versus a % rise within the benchmark S&P 500 index throughout the identical interval.

Concerning the Creator: Steve Reitmeister

Steve is best identified to the StockNews viewers as “Reity”. Not solely is he the CEO of the agency, however he additionally shares his 40 years of funding expertise within the Reitmeister Whole Return portfolio. Study extra about Reity’s background, together with hyperlinks to his most up-to-date articles and inventory picks.

The put up Bear Market Warning from the Bond Market? appeared first on StockNews.com