{kind=link}

The data offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra data.

Your credit score rating tells banks, lenders, landlords and even some employers quite a bit about your monetary state of affairs and duty. However, in keeping with TransUnion®, 45 million Individuals are both credit score underserved or credit score unserved, that means they lack a credit score historical past and a credit score rating. For those who’re one in all them, determining the way to begin constructing credit score for the primary time is important. Beneath, we discover just a few credit-building methods you could wish to use.

Key takeaways:

- Your credit score rating acts as a snapshot of your monetary well being and helps lenders, landlords and even some employers to resolve in the event that they wish to work with you.

- Turning into a licensed person or opening your individual bank card can assist you construct your credit score historical past and enhance your credit score rating over time.

- Checking your credit score report with every of the three credit score bureaus can assist you perceive the place you stand and make smarter monetary choices.

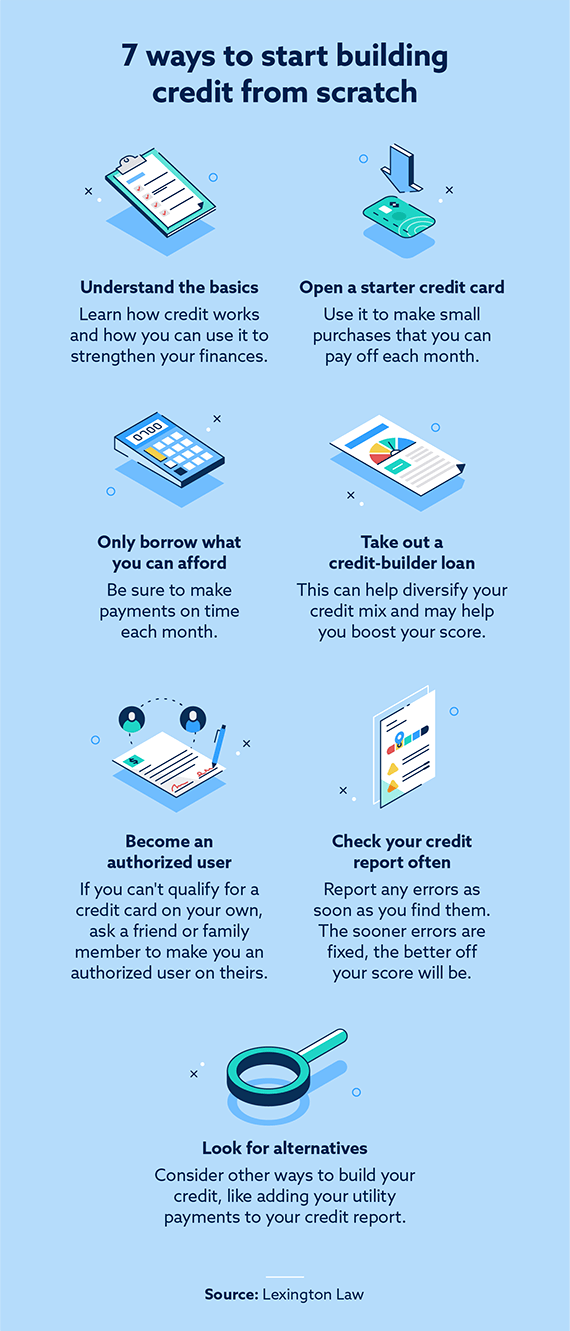

1. Perceive the fundamentals of credit score

Earlier than you can begin constructing good credit score, you must perceive the fundamentals of credit score and the way it works. Credit score refers to any mortgage or bank card that you could be take out. It represents a promise between you and your chosen lender or bank card supplier. They promise to lend you cash or offer you a bank card, and in trade, you conform to repay what you borrow.

If you make funds on time and in full, you’ll construct your credit score historical past and begin to see your credit score rating go up. There are totally different forms of credit score scores, however the commonest one is the FICO® credit score rating.

The FICO scoring system appears at your cost historical past, how a lot debt you’ve gotten, how a lot you’re charging on bank cards relative to the credit score restrict (often called your credit score utilization) and different comparable components. Your lenders and bank card issuers ought to report this data to the three major credit score bureaus throughout every billing cycle.

If you’re on prime of your funds and aren’t maxing out your playing cards, you’ll possible construct good credit score. For those who’re late persistently or miss funds, max out your bank cards or borrow greater than you possibly can afford to repay, your credit score rating might drop.

When you perceive the fundamentals of credit score, you can begin constructing your credit score historical past and enhancing your credit score rating.

2. Apply for a starter bank card

Starter bank cards are designed for people with poor credit score histories or no credit score histories, and so they’re out there from most banks and credit score unions. These playing cards usually have low credit score limits, making it more durable so that you can borrow greater than you possibly can afford to repay.

Some starter bank cards could also be secured bank cards. These playing cards are backed by a money deposit that you just make and have a credit score restrict equal to that deposit quantity. For those who make funds on time and in full, you possibly can preserve utilizing your bank card with out challenge. For those who miss a cost or can’t repay the bank card, your safety deposit will cowl it. Take into account that you’ll nonetheless be charged curiosity on these late or missed funds, and should you carry a steadiness from month to month, you’ll be charged curiosity, too. This charge can add up over time.

These playing cards might be straightforward to qualify for, even should you don’t have a credit score rating. Nonetheless, their low limits might make it laborious to make use of them for greater purchases.

For those who’re nonetheless a scholar, you might be able to qualify for a scholar bank card. These playing cards are sometimes unsecured bank cards, so that you received’t should make a money deposit. However the credit score restrict you’re eligible for could also be small as effectively.

3. Grow to be a licensed person

For those who don’t wish to tackle a bank card of your individual otherwise you don’t qualify for one, you might ask a trusted good friend or member of the family to make you an licensed person on their bank card. As a licensed person, you can also make purchases and construct your credit score rating on a card another person certified for. Finally, the bank card proprietor (your good friend or member of the family) is answerable for making month-to-month funds, so that you’ll have to work out an settlement on the way you’ll repay them for what you buy.

The advantage of turning into a licensed person is that you just’ll nonetheless construct your credit score rating over time with out having to tackle a bank card of your individual. Nonetheless, your credit score rating might take a success if the first cardholder misses funds or maxes the cardboard out.

4. Take out a credit-builder mortgage

For those who don’t have a confirmed credit score historical past, you might be able to use a credit score builder mortgage to construct your credit score. These are small loans designed that will help you set up a credit score historical past by making common on-time funds till you repay the mortgage in full.

In contrast to conventional loans, you received’t obtain the cash you borrow upfront. As a substitute, your lender (usually your financial institution or credit score union) will deposit the cash in a financial savings account. When you repay the mortgage in full, you’ll acquire entry to the cash in that account and might use it nevertheless you see match.

These loans can have decrease charges than credit-building bank cards, making them supreme for debtors who wish to keep away from excessive curiosity funds.

5. Use credit score responsibly

Utilizing credit score responsibly can assist you create a powerful credit score historical past and enhance your credit score rating over time.

Right here’s how one can develop into a accountable credit score person:

Strengthen credit score historical past

Establishing or strengthening your credit score historical past is step one in utilizing your credit score responsibly, and the best manner to try this is to pay payments on time and in full every month. To remain on prime of funds, enroll in autopay each time attainable and let your bank card firm, lender or different service supplier debit the cost out of your checking account robotically.

Frightened about spending greater than it’s best to? Restrict what you employ your bank card for. For instance, you might use your bank card to pay for a streaming service and arrange autopay for that one invoice. This may make it easier to pay the cardboard off in full with out placing you susceptible to spending greater than it’s best to.

Maintain your credit score utilization low

Your credit score utilization ratio refers back to the quantity of credit score you’re utilizing in your card relative to the cardboard’s restrict. By holding it low and never maxing out your playing cards, you’ll strengthen your credit score historical past over time. Most monetary consultants suggest holding your credit score utilization ratio beneath 30 p.c.

Strive committing to solely utilizing your card for purchases you realize you possibly can repay in full and have already budgeted for, just like the streaming service talked about above. After you have a historical past of creating on-time funds, you possibly can ask your bank card issuer for a credit score restrict enhance. The upper your credit score restrict is and the smaller your excellent steadiness is, the decrease your credit score utilization shall be.

Combine up your credit score varieties

Credit score combine performs an necessary function in your credit score rating and your credit score historical past. Moderately than simply taking over a variety of bank cards, you could discover it useful to use for different forms of credit score. Private loans, auto loans and credit-builder loans can all enhance your credit score combine.

Bank cards are thought of revolving debt that you need to use and repay till you shut the cardboard. Private loans, auto loans and credit-builder loans are forms of installment loans that allow you to make set funds every month till the top of the mortgage’s time period or till you repay the mortgage in full. Having a mixture of the 2 varieties might enhance your credit score rating.

6. Search for alternative routes to construct credit score

Listed below are just a few alternative routes to construct credit score if taking over a brand new mortgage or opening a bank card doesn’t meet your wants.

Add different information to your credit score profile

Credit score bureaus are keen to think about different credit score information when figuring out your credit score rating and establishing your credit score historical past. You might be able to add utilities, hire funds, mobile phone invoice funds and different recurring bills to your credit score profile.

So long as you make funds on time and your utility supplier, landlord or mobile phone firm stories these on-time funds to the credit score bureaus, you’ll construct your credit score historical past and enhance your rating over time.

Take into account cash-flow underwritten bank cards

These bank cards allow you to cost sure month-to-month payments like streaming providers, web payments and different comparable providers with out having to bear a credit score test. The cardboard issuer will as an alternative take a look at your complete revenue and checking account exercise to find out should you’re eligible for the cardboard and the way a lot they’re keen to lend you.

As you make funds on time, the cardboard issuer stories these funds to the credit score bureaus, serving to you identify your credit score historical past.

Qualify primarily based on international credit score historical past

For those who lately immigrated to the US, you received’t have a longtime credit score historical past within the nation. Nonetheless, when you’ve got a powerful credit score historical past in your house nation, you might be able to use that historical past to qualify for loans or bank cards.

When you begin making funds and utilizing your traces of credit score or loans responsibly, you’ll construct your credit score historical past in the US. It’s a approach to put your good monetary habits to work in your new house. Main bank card issuers like Chase, Capital One and American Categorical all challenge playing cards to qualifying immigrants.

7. Monitor your credit score often

Get within the behavior of checking your credit score rating and your credit score report often. This may make it easier to monitor your rating over time and observe your enhancements. When you have a unfavorable credit ratings rating and preserve working in your monetary habits, you’ll have the ability to observe your progress and see enhancements so you possibly can keep motivated.

Instruments like Credit score.com make it straightforward to test and monitor your credit score rating without spending a dime. AnnualCreditReport.com enables you to test your credit score report from every of the three main credit score bureaus without spending a dime frequently, so you possibly can monitor your report for errors. For those who discover any errors, you possibly can dispute them with the credit score bureaus. If these errors are fastened, your rating would possibly go up.

Prepared to begin constructing your credit score?

Determining the way to begin constructing credit score for the primary time can really feel overwhelming, however so long as you retain these methods in thoughts, you’ll be effectively in your approach to establishing an excellent rating. For a view of the place you stand, get your free credit score evaluation right now to see your credit score rating and a brief abstract of your credit score report.

Word: Articles have solely been reviewed by the indicated lawyer, not written by them. The data offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the web site don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.