{kind=link}

This afternoon the Division of Schooling quietly modified the coverage on one-time forgiveness for debtors with FFEL program loans. The abrupt shift is one more blow for FFELP debtors.

Whereas the information is undeniably dangerous, all hope shouldn’t be misplaced. There’s a likelihood that debtors with commercially-held FFELP loans should but get $10,000 or $20,000 of mortgage cancellation.

This text will clarify what modified, why it modified, and what debtors impacted by the coverage ought to do. Lastly, I’ll cowl the few nuggets of hope in an in any other case awful information day.

The Coverage Change for FFELP Mortgage Debtors

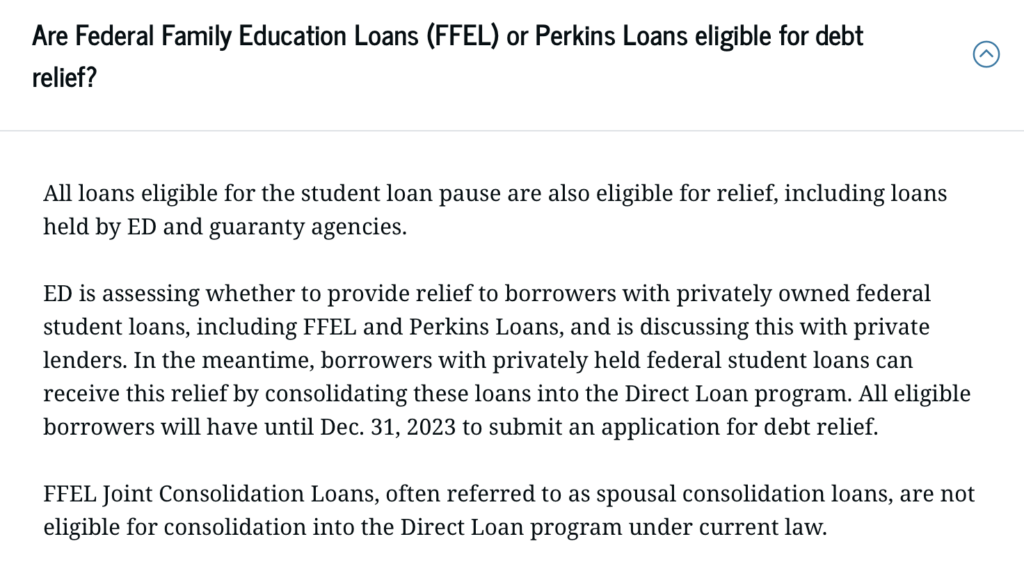

Earlier than right now, the official coverage of the Division of Schooling was that privately-held FFELP loans may qualify for the one-time Biden Forgiveness Program.

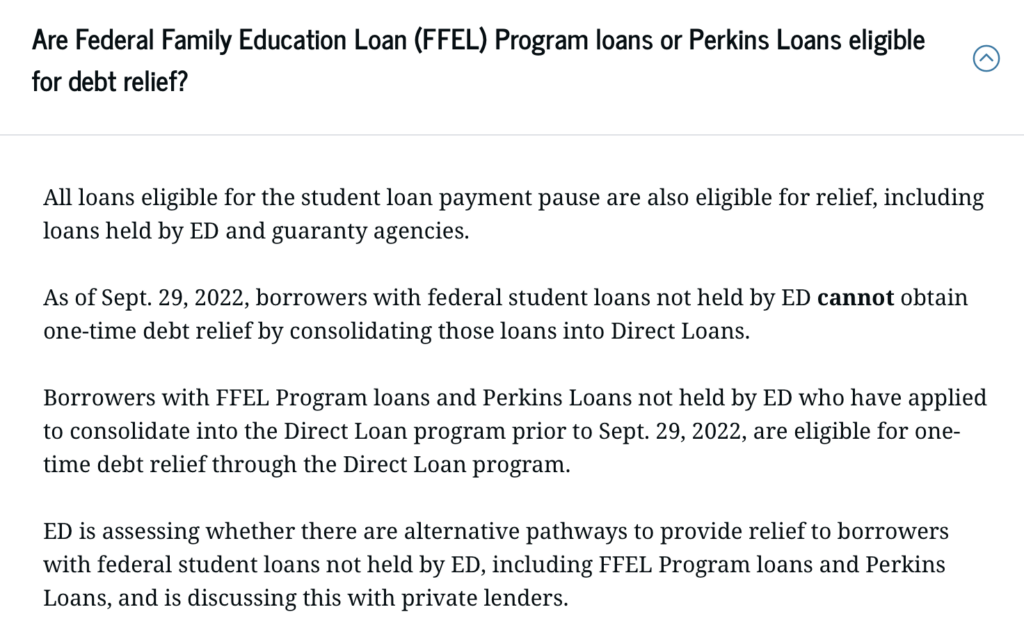

Below the brand new coverage, these debtors can not qualify for mortgage forgiveness, and they don’t have a path to forgiveness.

Here’s a screenshot from yesterday:

Right now, the language was modified to the next:

Whereas there are numerous jarring facets of the coverage shift, imposing a deadline with out first saying it appears particularly merciless.

A Particular Word for federally-held FFELP Debtors: If in case you have federally-held FFELP loans, this coverage change doesn’t apply to you. Debtors with federally-held FFELP loans stay eligible for as much as $20,000 in mortgage forgiveness.

In case you are not sure in case your mortgage is federally held, the best option to inform is thru the fee pause guidelines. Throughout the Covid aid, if you weren’t required to make funds or charged curiosity, your mortgage is federally-held. In case you needed to make funds, your mortgage is privately or commercially held.

You too can confirm the standing of your mortgage by accessing the database on studentaid.gov.

The Rationalization for the Abrupt Coverage Change

Right now, six states filed a lawsuit difficult Biden’s one-time mortgage cancellation coverage.

The lawsuit raised a number of arguments, however the one which led to right now’s coverage adjustments got here from the state of Missouri, dwelling of MOHELA. MOHELA was created by the Missouri legislature in 1981 and operates as a quasi-governmental entity. Notably, MOHELA is also accountable for some commercially-held FFELP loans.

In keeping with the grievance, “[t]he consolidation of MOHELA’s FFELP loans harms the entity by depriving it of the continued curiosity funds that these loans generate.”

In different phrases, if debtors consolidate their privately-held FFELP loans, MOHELA loses cash.

—

The importance of this element goes again to the authorized idea of standing. Anybody bringing a lawsuit should meet particular necessities to have the courtroom hear the case. If these necessities usually are not met, the case will get dismissed.

Turning to pupil mortgage cancellation, you possibly can’t sue since you don’t just like the regulation or assume it’s a waste of cash. Standing requires an damage to the social gathering bringing the lawsuit. Some have argued that no social gathering would have standing to problem a one-time pupil mortgage forgiveness program.

If privately-held FFEL loans are eligible for forgiveness by consolidation, the state of Missouri has a really robust standing argument. If the lawsuit clears the standing requirement, a federal decide may stop Biden’s complete forgiveness program — not simply the FFELP forgiveness.

The actions of the Division of Schooling right now are a determined try to make sure that a decide doesn’t block Biden’s forgiveness program. It’s the authorized equal of chopping off a limb to save lots of the physique.

Steps for FFELP Debtors to Get Forgiveness

Sadly, there isn’t a fast repair to this case. You’ll be able to’t return in time and submit an software to consolidate yesterday.

The most effective guess for impacted debtors is to use stress on the federal authorities. Go to studentaid.gov and file a grievance. Name your elected representatives and allow them to know that you’re sad with the FFEL coverage change.

The timing of the unique pupil mortgage forgiveness announcement was clearly geared toward making voters blissful earlier than the midterm elections. If individuals present their outrage over the reversal, it ought to encourage motion.

Proper now, negotiations are seemingly taking place between the federal authorities and FFEL mortgage servicers. Division of Schooling legal professionals have to determine a option to cancel FFEL loans with out hurting FFEL mortgage holders. The extra stress voters apply on their elected representatives, the extra seemingly it turns into {that a} deal is reached to keep away from the lawsuit.

Now could be the time to get loud and be heard.

If that every one fails, it is usually attainable that the sudden change in guidelines results in a borrower lawsuit towards the Division of Schooling. If that day comes, this text might be up to date accordingly.

The Hope for FFEL Forgiveness

The Division of Schooling assertion right now makes it clear that they’re attempting to resolve the FFEL concern:

Our purpose is to offer aid to as many eligible debtors as shortly and simply as attainable, and this can permit us to attain that purpose whereas we proceed to discover extra legally-available choices to offer aid to debtors with privately owned FFEL loans and Perkins loans, together with whether or not FFEL debtors may obtain one-time debt aid with no need to consolidate.

With out query, it is a setback. Nonetheless, there may be nonetheless time for constructive developments.

Moreover, the Biden Administration’s observe report is fairly good in relation to serving to FFELP debtors. The Restricted Waiver on PSLF allowed many public servants with FFEL loans to get the credit score they deserved. Likewise, new laws will assist debtors with FFELP Spousal Consolidation Loans qualify for IDR reimbursement and PSLF.

Right now’s developments are a transparent signal that anyone dropped the ball. Nonetheless, there’s a observe report of fixing issues for FFELP debtors and a said need to repair this explicit concern.

If FFELP debtors make sufficient noise about getting misled and excluded, it may encourage one more repair.