{kind=link}

In line with 2022 Division of Schooling information, about 9 million debtors out of the roughly 43 million complete use an earnings pushed compensation plan (IDR). Below the Biden IDR plan, it’s nearly sure that hundreds of thousands extra will enroll, however the query is what number of?

Assuming no extra debtors join IDR, consultants on the Wharton Finances Mannequin discover the Biden IDR plan would value over $70 billion over 10 years. Nevertheless, with a much more beneficiant IDR plan, you can’t assume no extra debtors would enroll as a result of that’s an absurd assumption.

Hundreds of thousands of debtors will see big financial savings on the Biden IDR plan, notably these three teams:

- Debtors incomes between $40,000 to $100,000 a yr with undergraduate debt

- Debtors with bigger households

- Graduate {and professional} diploma holders who plan to repay their debt finally

To provide you with an correct estimate of the profit and price of the Biden IDR plan, we should take a look at what number of extra debtors would enroll, how a lot decrease their funds could be, and the way a lot curiosity could be sponsored.

How the outdated IDR plans examine to the brand new Biden IDR plan

One very underappreciated a part of the Biden IDR plan is the rise in earnings protected earlier than any funds should be made.

The ICR plan from the Nineties protected 100% of the poverty line. The IBR, PAYE and REPAYE plans protected 150% of the poverty line.

The brand new Biden IDR plan will shield 225% of the poverty line.

For instance, below the perfect 2022 IDR plans (PAYE and REPAYE), a single borrower may earn $20,385 earlier than owing something on their scholar loans. Below the Biden IDR plan, a borrower may earn $30,578 earlier than owing something on their scholar loans (utilizing 2022 poverty line numbers).

For undergraduate debtors, their funds would drop from 10% of discretionary earnings to five% of discretionary earnings. For a single borrower with $70,000 of earnings, he would solely pay 5% of the quantity above $30,578. His month-to-month fee could be $164 a month as a substitute of $413 a month on REPAYE.

Below the outdated IDR regime, this borrower would don’t have any likelihood at forgiveness. But when the borrower acquired married or had youngsters, the fee would fall to as little as $50 to $100 a month, given the rise in household dimension.

If this borrower incomes $70,000 a yr had two youngsters, his fee would fall from $164 a month to $76 a month.

The typical beginning wage of the category of 2020 was $55,260, in accordance with the Society for Human Useful resource Administration. Below the Biden plan, a borrower incomes this earnings would pay $103 a month. We’ll use this estimate for the common IDR fee going ahead in our evaluation.

Further debtors signing up for Revenue Pushed Compensation below the Biden plan

As said above, 9 million debtors use an IDR plan as of 2022.

What number of extra would join IDR?

In case you improve the poverty line by 50%, presumably, you’d see a 50% improve within the variety of debtors who may obtain forgiveness on their scholar mortgage steadiness.

In case you lower the proportion of earnings funds from 10% to five%, you may double the variety of debtors who may gain advantage.

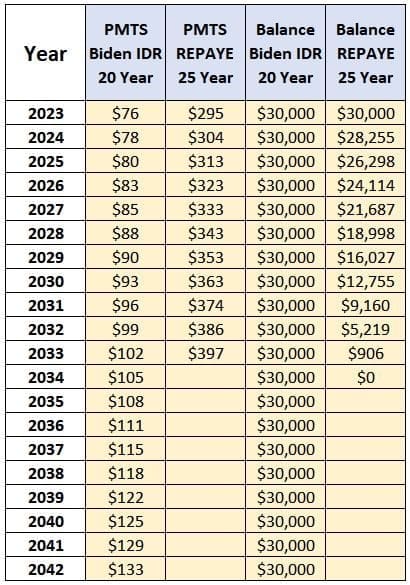

This evaluation is tough, however take into account that the common scholar mortgage debt is $37,013, and the common borrower is an undergraduate borrower making an excessive amount of to get forgiveness on an IDR plan.

That common borrower is now a wonderful forgiveness case. Think about a borrower with two children incomes $70,000 of earnings with $30,000 of scholar debt. He would pay $24,429 over 20 years. When accounting for inflation, the price could be even decrease. Right here’s how his funds examine to the REPAYE plan at the moment.

IDR adoption additionally relies on how straightforward the Division of Schooling makes it to enroll.

An inexpensive estimate could be something between 50% to 200% extra debtors would join an IDR plan below the Biden guidelines.

If there are 9 million debtors on an IDR plan, meaning the brand new quantity would change into wherever between 13.5 million to 27 million. An inexpensive estimate may be that the variety of debtors on an IDR plan would double to 18 million.

In line with the Federal Reserve Financial institution of Cleveland, the common scholar mortgage fee is $393 a month.

Assuming that the common IDR fee below the Biden plan could be $103 a month, the overall money stream distinction to the Treasury could be the marginally elevated variety of IDR debtors instances the distinction in what they’re paying now and what they might pay on an IDR plan.

9 million debtors * (393 – 103) *12 = $31,320,000,000 per yr in decreased money stream to the scholar mortgage program and internet financial savings to debtors.

It could be affordable to imagine the big improve in IDR adoption would happen primarily with undergraduate debtors as graduate debtors would have the same fee below the brand new plan, though many new graduate debtors may enroll quickly for the curiosity subsidies (extra on that later).

Extra complicated evaluation utilizing current worth may be carried out, with most debtors below this mannequin lowering their prices of compensation between 33% to 50%.

Elevated discretionary earnings for debtors already on an IDR plan

Virtually all debtors at the moment on an IDR plan would see decreased funds below the Biden plan.

A extra complicated evaluation would ask what the common household dimension is per borrower, however an easier evaluation is to simply take a look at the financial savings for a single borrower, regardless that that determine understates the financial savings debtors will expertise.

A single borrower would see their protected earnings rise from $20,385 to $30,578 earlier than they wanted to make a fee. This is able to save roughly $1,020 per borrower per yr for the 9 million present IDR debtors.

That determine could be 9 million * 1,020 = $9,180,000,000 per yr.

Decreased funds for debtors already on an IDR plan

In line with the Richmond Fed, 24% of undergraduate debtors and 39% of graduate debtors had opted into an IDR plan as of 2017.

Graduate debtors have traditionally signed up for IDR plans at larger charges as a result of undergraduate debt has strict borrowing limits and graduate debt doesn’t due to the Grad PLUS program.

The Biden IDR plan permits undergraduate debtors to pay 5% of their discretionary earnings. Graduate debtors may pay a weighted common relying on their mixture of undergraduate and graduate debt.

Utilizing a borrower incomes the common beginning wage of $55,260, he would have paid $291 a month on the REPAYE plan.

He would save $85 a month from the elevated definition of discretionary earnings we already accounted for.

So, the distinction between $206 and $103 (the fee below the Biden plan) is his money stream financial savings.

The typical graduate borrower might need half of their debt from grad college and half from undergrad. Below the weighted common method that the Biden IDR plan takes, his fee could be $154 a month.

Then, the distinction between $206 and $154 is $52 a month.

To estimate this value of decreased IDR funds for present debtors, we have to know what the break up is for graduate and undergraduate debtors on an IDR plan.

To maintain issues easy, let’s assume two-thirds of IDR debtors have graduate debt, and one-third have solely undergraduate debt.

Let’s additionally assume the common borrower earns $55,260, the common 2020 beginning wage.

This is able to lead to financial savings to present debtors of:

2/3 * 9,000,000 * (206-154) *12 + 1/3*9,000,000* (206-103) *12 = $7,433,640,000.

Curiosity subsidies for debtors utilizing an IDR plan

Below the present REPAYE plan, most debtors would obtain a 50% curiosity subsidy on all curiosity that their month-to-month fee doesn’t cowl.

The brand new Biden IDR plan is ultra-generous in relation to curiosity subsidies, as present debtors have larger REPAYE funds, leading to much less leftover curiosity to subsidize.

Moreover, debtors with massive debt from graduate {and professional} faculties obtain the biggest rate of interest subsidies below the Biden IDR plan.

A resident doctor incomes $60,000 a yr with a $250,000 steadiness at a 6% rate of interest may pay $245 a month, with the remaining curiosity sponsored. Their efficient rate of interest could be roughly 1.18%, under the rate of interest for sponsored loans for undergraduates.

Solely throughout college and a few years out of coaching would their rate of interest rise to the statutory price of their promissory word.

A trainer with $60,000 earnings and $60,000 of debt at a 5% rate of interest (half of which was from grad college) would additionally obtain an curiosity subsidy, however not as massive of 1.

This trainer would pay $2,207 a yr. Their $60,000 mortgage throws off $3,000 a yr of curiosity fees, so about $800 is sponsored. His efficient curiosity could be 3.68%.

After all, a excessive incomes attending doctor would have an rate of interest just like their statutory price, however solely a few years out of coaching as soon as their AGI had been reported on a earlier yr’s tax return.

Assumptions of curiosity subsidy value for present IDR debtors

So as to add to the confusion, these curiosity subsidies wouldn’t be related apart from debtors who used an IDR plan quickly to obtain massive curiosity subsidies earlier than refinancing or paying them off.

Conventional budgeting metrics, although, would seemingly measure the whole curiosity subsidy as a price, as did estimates of the price of the COVID scholar mortgage fee and curiosity pause.

To measure these curiosity subsidies, many assumptions would should be made.

Utilizing the $55,260 earnings “common borrower,” his fee could be $103 a month, or $1,236 a yr.

Assume he has a median $37,000 scholar debt steadiness and that that is consultant.

If that debt has a 5% rate of interest, he would owe $1,850 a yr of curiosity. The distinction between his funds and the curiosity is his curiosity subsidy, which is $614 a yr.

Despite the fact that the REPAYE gives a 50% curiosity subsidy, the funds are excessive sufficient for many undergraduate debtors that there isn’t any curiosity left over to subsidize.

So, 9,000,000 * 614 = $5,526,000,000.

Assumptions of curiosity subsidy value for brand spanking new IDR debtors

The large unknown is that if the very best debt debtors will strategically swap to the Biden IDR plan for the primary 2 to three years of their careers whereas their earnings is low to obtain a really massive curiosity subsidy.

For instance, a Large Regulation affiliate beginning wage is about $200,000.

Most Large Regulation attorneys begin roughly in September annually.

IDR funds are based mostly on the newest tax returns.

So, somebody graduating in 2023 would have a previous yr earnings of $0 (or roughly $30,000 in the event that they did a summer time internship). Their curiosity subsidy in yr 1 could be 100%.

In yr two, they solely earned earnings for 3 or 4 months out of the yr, so they might obtain a close to 100% curiosity subsidy in yr 2 as effectively.

There will not be that many Large Regulation attorneys in comparison with debtors total. However a small proportion of debtors maintain a really outsized share of the scholar mortgage debt total. Any behavioral diversifications of this class of debtors would save this group some huge cash, as the sort of excessive earnings borrower at the moment doesn’t select an IDR plan.

If we merely assume that new debtors will appear like the hypothetical $55,260 earnings borrower above with the identical common debt, then the curiosity subsidy could be comparable. You might assume the 9 million new debtors paying about $1,200 a month with $1,800 a yr in curiosity would obtain the same internet subsidy of $600.

So, 9,000,000 * 614 = $5,526,000,000.

Tuition will increase at undergraduate and graduate diploma packages

One examine by the NY Fed finds that for each $1 improve in sponsored scholar loans, universities improve their tuition by 60 cents.

In a recording of the Nationwide Affiliation of Monetary Help Directors podcast, the hosts warned that faculties wanted to watch out about massive tuition will increase for the primary 12 months of this new IDR program. The Biden administration may additionally record faculties in a report on “faculties that produce graduates with unmanageable money owed.”

Whereas a number of the most doubtful for-profit faculties have been shut out of federal assist, the overwhelming majority of faculties with unhealthy outcomes, each non-profit and for-profit, really feel completely zero penalties for elevating tuition below this new plan.

What appears undoubtable is that faculties will reply by rising their tuition extra quickly than they did earlier than. Cheaper undergraduate packages may catch on that there’s successfully no distinction between borrowing $20,000 and $40,000 below the brand new IDR plan for many of their college students and refuse to supply tuition reductions or as vital benefit assist.

These adjustments gained’t occur straight away. Debtors will should be satisfied of the deserves of this method and faculties will take some time to appreciate the chance and reply to incentives with out making it seem they’re performing instantly based mostly on the brand new income alternative a extra beneficiant IDR plan represents.

Roughly $100 billion of scholar loans are issued annually. Given the NY Fed’s analysis, it appears affordable to imagine that there could be a 1% improve within the complete quantity borrowed as a consequence of faculties rising their tuition at a price larger than they might have in any other case. This quantity may simply be an order of magnitude bigger.

So, 1% * $100 billion = $1 billion per yr.

Further college students going to varsity and pursuing extra schooling

When the price of faculty goes down for the borrower, extra debtors will pursue larger ranges of schooling.

Debtors may select to go to some faculty versus no faculty. Debtors getting bachelor’s levels may be extra more likely to go forward and pursue larger ranges of graduate schooling.

Any estimate right here is stuffed with ambiguity and assumption. If solely an extra 1% of the American inhabitants pursues faculty due to these adjustments, that’s 3 million debtors. Assuming these debtors take out $5,000 per yr on common, that’s an extra $15 billion of scholar loans annually. That’s not the complete value as you would need to measure the subsidy price.

The purpose is that if the worth for an excellent or service goes down, you’d count on customers to change into extra more likely to buy that good or service. We’ll depart this value out of our estimate as a result of it feels essentially the most speculative.

Complete 10 yr value of the Biden IDR plan

The Division of Schooling has by no means launched statistics on the common earnings of IDR debtors and common IDR funds. In the event that they did, these assumptions may very well be tightened up considerably.

Additionally, many debtors may not know to join this new IDR plan. With out curiosity capitalization below the brand new adjustments, any borrower checking that they need the bottom fee would seemingly be switched into this new plan, so most will seamlessly be converted.

Summing up every of the annual advantages and prices under, we’ve:

- Further debtors signing up for IDR: $31.3 billion

- Elevated discretionary earnings: $9.2 billion

- Decreased funds for debtors on an IDR plan now: $7.4 billion

- Curiosity subsidies for present IDR debtors: $5.5 billion

- Curiosity subsidies for brand spanking new IDR debtors: $5.5 billion

- Further Tuition Will increase by Faculties: $1 billion

- Extra debtors attending faculty and pursuing larger ranges of schooling: Undetermined

Summing up the above, we’ve $60 billion yearly.

Over 10 years, which is the customary interval to take a look at budgetary impacts, the overall financial savings debtors would expertise could be $600 billion.

This determine exceeds the estimated $500 billion to $600 billion in cancellation below the Biden scholar mortgage aid plan.

And the price financial savings for debtors may very well be considerably larger if extra debtors and faculties act of their rational greatest curiosity by optimizing their AGI, borrowing the max, elevating tuition to maximise income, and extra college students understand there isn’t a lot of a draw back to attending faculty from a monetary perspective.

Prices would improve additional if Stafford mortgage limits have been elevated, as they haven’t been for a number of years.

The plan would seemingly trigger the common scholar mortgage borrower to go from paying again her debt to treating her debt like a tax and pursuing scholar mortgage forgiveness as a substitute whereas paying the minimal potential.

What’s clear with the Biden IDR plan is that debtors have hardly ever ever had the chance to save lots of such an enormous amount of cash.