{kind=link}

The data offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra data.

Debt consolidation loans normally don’t harm your credit score in the long run. Arduous inquiries that happen once you apply for a mortgage can briefly have an effect on your rating. Conversely, making your mortgage funds on time can progressively enhance your credit score.

Debt consolidation loans normally don’t harm your credit score in the long run. These loans can enhance your credit score by combining your debt into one account. However debt consolidation can initially knock your rating down a bit, so it’s necessary to study as a lot as potential about this technique.

How does a debt consolidation mortgage work?

Debt consolidation combines a number of money owed right into a single mortgage. This reduces your general curiosity and helps you set up your debt, making funds extra manageable. Debt consolidation loans gained’t harm your credit score in and of themselves.

Nonetheless, laborious inquiries that happen once you apply for a consolidation mortgage can quickly decrease your credit score rating. There are a number of methods to consolidate your accounts, and every technique has benefits and downsides relying in your distinctive circumstances.

Private mortgage

A private line of credit score, or private mortgage, is on the market at any time and can be utilized to repay debt shortly. Private loans can enhance your credit score by diversifying your credit score profile. Paying off debt with a mortgage reasonably than with a bank card may cut back your credit score utilization, which can enhance your credit score well being.

Do not forget that this course of entails taking out a mortgage that you have to pay again on time. You might also need to rethink this feature in case your present credit standing will restrict you to excessive rates of interest on private loans.

Borrowing from a 401(okay)

If in case you have a 401(okay) retirement account, you’ll be able to borrow as much as half this stability as an interest-free choice to repay debt. Borrowing from a 401(okay) doesn’t have an effect on your credit score, although you have to repay the borrowed quantity in 5 years to keep away from penalties.

It’s necessary to recollect what a 401(okay) is for—retirement. Taking out funds for short-term debt funds can considerably detract out of your retirement financial savings. You might also need to take care of tax repercussions when taking this motion.

Dwelling fairness mortgage or line of credit score

Dwelling fairness loans or traces of credit score are maybe the riskiest types of debt consolidation, however additionally they provide some vital advantages. Lenders will give you a mortgage and use your property as collateral. If you happen to fail to repay the mortgage throughout the period of time agreed upon, you can lose your property.

You have to have wonderful credit score to take out a house fairness mortgage or line of credit score. While you apply, lenders will hit you with a credit score test, which might initially decrease your rating. The impression in your credit score is probably not extreme, however these loans may accumulate very excessive curiosity.

How does debt consolidation have an effect on your credit score?

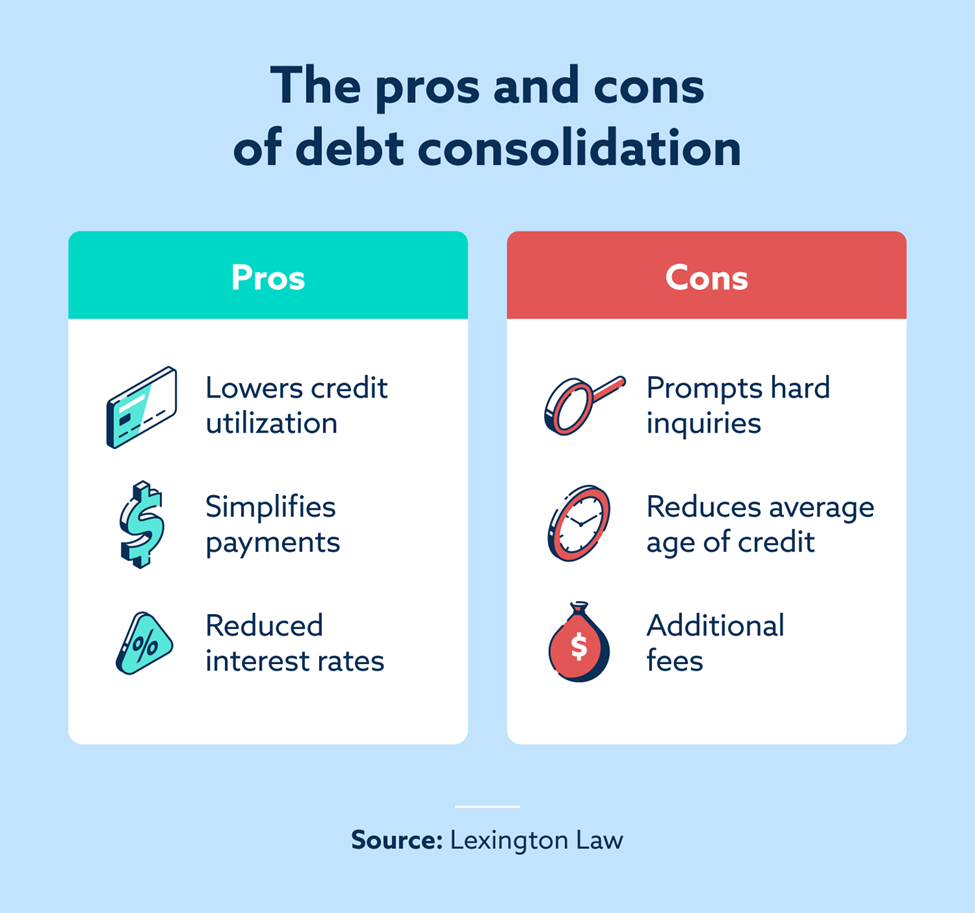

Every debt consolidation technique can have an effect on your credit score positively and negatively. Listed below are just a few areas it might have a adverse impression:

- Credit score purposes: Making use of for a private mortgage or a stability switch card prompts a tough inquiry to be carried out in your credit score. Arduous inquiries can bump down your rating by 5 to 10 factors, they usually can keep in your report for one to 2 years.

- Common age of credit score: The ages of your credit score accounts matter—sometimes, the older, the higher. Opening a brand new account lowers your common credit score age, which can initially negatively impression your credit score.

Alternatively, debt consolidation tends to positively impression the next classes:

- Credit score utilization: A brand new debt consolidation account will normally enhance the quantity of obtainable credit score you may have. So long as you don’t start spending considerably extra after opening the brand new account, you’ll be utilizing much less of your accessible credit score, which is able to profit your credit score.

- Cost historical past: Constantly paying off your new mortgage on time will doubtless positively impression your credit score.

Options to debt consolidation

If debt consolidation doesn’t really feel best for you, there are different debt reduction choices to assist restore your peace of thoughts.

Stability switch

A stability switch permits you to transfer debt onto a single bank card with a decrease rate of interest, permitting you to repay your money owed for much less. Many stability switch playing cards provide 0 % APR throughout an introductory interval, offering an interest-free window to repay debt.

If you happen to determine to pursue a stability switch card to repay debt, examine the cardboard’s APR following the introductory interval. Your rate of interest could take you abruptly and skyrocket should you don’t do your due diligence.

Debt administration program

Debt administration providers may help by counseling you concerning your choices once you’re fighting debt. A debt administration program will doubtless contain a counselor negotiating decrease curiosity with collectors and doubtlessly closing bank cards.

Visiting a debt administration counselor gained’t hurt your credit score in any respect. Nonetheless, your credit score report could mirror any debt administration applications you enroll in till you now not use them.

Debt settlement or chapter

Debt settlement is negotiating with collectors to pay considerably much less cash than you owe to have your debt forgiven. Chapter is a long-term authorized course of that helps folks set up and generally get rid of their debt.

These two choices needs to be a final resort when struggling to repay debt, as they’ll have a considerably adversarial impact in your credit score. Each debt settlement and chapter will stay in your credit score report for seven to 10 years. Nonetheless, if it’s essential to maintain large debt now and take smart monetary steps sooner or later, these processes might finally be the fitting answer for you.

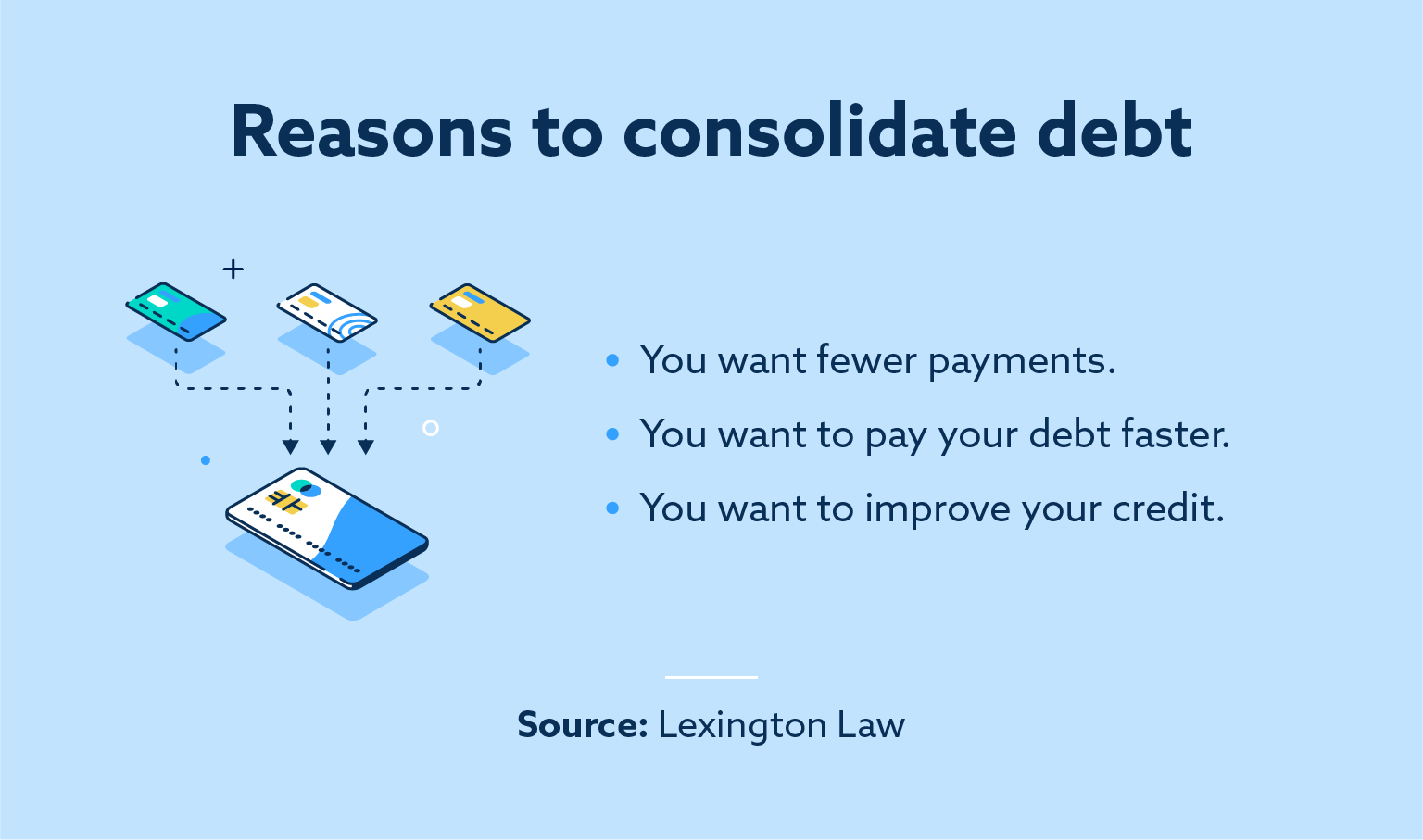

Ought to I consolidate my debt?

Earlier than pursuing debt consolidation, it’s necessary to take a complete have a look at the explanations you’re curious about consolidating debt and your plans for the foreseeable future.

Do you may have a excessive rate of interest?

If the curiosity on the debt you owe is 20 % or extra, you’ll doubtless get monetary savings by consolidating debt. Nonetheless, sure stability switch choices cost exorbitantly excessive charges. Analysis beforehand to find out which possibility saves you extra money.

Are you lacking funds?

Holding monitor of your entire accounts may be disturbing. If remembering to pay your payments has been a battle, and also you’ve repeatedly missed funds, debt consolidation could assist.

Consolidating your debt might simplify your monetary life by permitting you to maintain all funds directly. This may even profit your credit score in the long term, since missed and late funds can hurt your credit score well being.

Do you want wonderful credit score within the brief time period?

If you happen to plan to take out a mortgage or a mortgage quickly, it’s possible you’ll have to safeguard your credit score in any respect prices. Since many debt consolidation strategies will put a brief dent in your credit score, it might be smart to carry off till after a lender has accepted you.

In the end, whether or not you determine to pursue debt consolidation and which technique you select is dependent upon the load of your money owed and what would profit your credit score most. If you happen to’re nonetheless on the fence, it’s a good suggestion to seek the advice of a monetary advisor earlier than making selections that might have long-lasting penalties.

No matter choice you make, keep in mind to maintain your credit score well being on the forefront of your thoughts and take the steps to restore your credit score to increase your monetary alternatives.

Be aware: Articles have solely been reviewed by the indicated lawyer, not written by them. The data offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary, or credit score recommendation; as an alternative, it’s for common informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the web site don’t create an attorney-client or fiduciary relationship between the reader, person or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.