{kind=link}

The data supplied on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra data.

Your credit score rating just isn’t immediately affected once you get married. Nonetheless, spouses can nonetheless influence one another’s credit score by means of different monetary choices.

Marriage will change many areas of your life, however will it change your credit score? The quick reply is, no, getting married doesn’t immediately influence your credit score, however marriage and credit score scores are nonetheless linked.

Some marriage-related modifications can have an effect on your credit score, together with name-change problems and including approved customers to an account. Fortunately, this doesn’t should be seen as a destructive. As a substitute, view your marriage as a possibility to remain financially wholesome collectively. Step one is knowing what is going to influence your credit score rating after marriage. This information breaks it down so you recognize precisely what’s to return and methods to deal with it.

What occurs to your credit score once you get married?

While you get married, nothing mechanically occurs to your credit score rating. Bear in mind, a credit score rating is a mirrored image of 1 particular person’s creditworthiness, so getting married doesn’t inherently have an effect on it. Let’s take a look at what does occur to your credit score after marriage.

You and your partner retain your credit score

Even after the wedding certificates is signed, each spouses retain their very own credit score scores. Neither rating will change mechanically, nor will a partner’s good or poor credit instantly have an effect on the opposite’s rating.

You and your partner can share credit score

In the event you resolve to cosign a mortgage or automotive lease, you’ll share the consequences of that mortgage. Any exercise—good or dangerous—made on this shared credit score account will have an effect on each spouses’ credit score scores.

You and your partner’s credit score could also be restricted

A decrease credit score rating may negatively influence a pair’s approvals for mortgages, loans and shared rates of interest. Lenders performing credit score inquiries are extra possible to attract up phrases and agreements based mostly on a pair’s lowest credit score rating, which may additionally restrict out there credit score on shared credit score accounts.

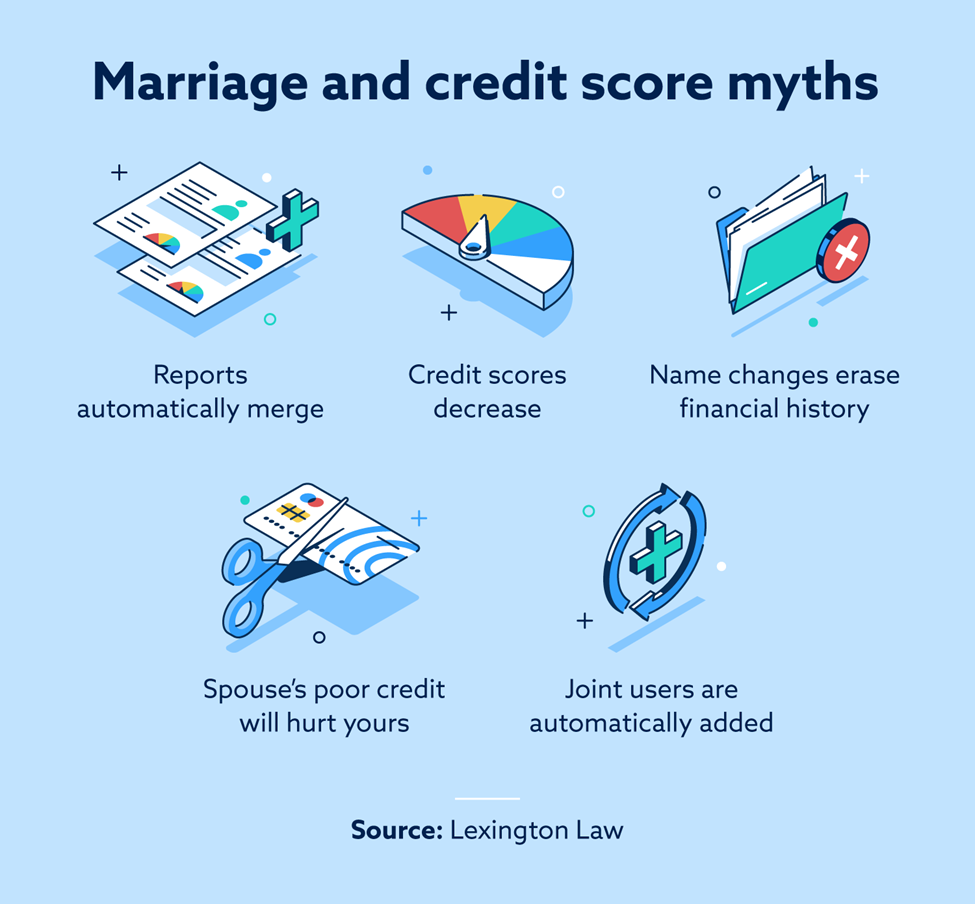

Marriage and credit score scores: 5 frequent myths

The myths surrounding marriage and credit score scores may cause pointless anxiousness heading into a marriage day. Understanding the frequent myths round marriage and credit score scores can assist you put together for what’s to return—and allow you to ignore the issues that don’t actually matter.

Fable 1: Credit score studies merge once you get married

You don’t lose your monetary identification once you get married, nor does it mechanically merge along with your partner’s. Credit score studies are recognized by your Social Safety quantity, not your final title or conjugal relationship. Till you get joint monetary merchandise, like credit score traces or a mortgage, your credit score report will solely replicate your individual credit score exercise.

Fable 2: Marriage lowers your credit score rating

Getting married is not going to decrease your credit score, however merging your spending habits along with your partner doubtlessly can.

If a “saver” marries a “spender,” the saver is likely to be influenced by the partner or should cowl the opposite’s spending. In fact, these issues don’t simply present up after a marriage day. Spending habits are normally clear early on in a relationship, and most {couples} discover a monetary equilibrium.

So, your marriage gained’t decrease your credit score rating. Nonetheless, marrying somebody with poor credit score after which having joint accounts with them may probably damage your credit score.

Fable 3: Your credit score historical past is erased once you change your final title

Altering your final title doesn’t imply you’re beginning a credit score historical past from scratch. Your new title will develop into an extra alias in your report, and your credit score report will stay the identical.

When collectors report your new title on the finish of the following cycle, the three main credit score bureaus will mechanically obtain and document the brand new data in your report. Take into account requesting a free credit score report a month after the swap to make sure the brand new data has been famous.

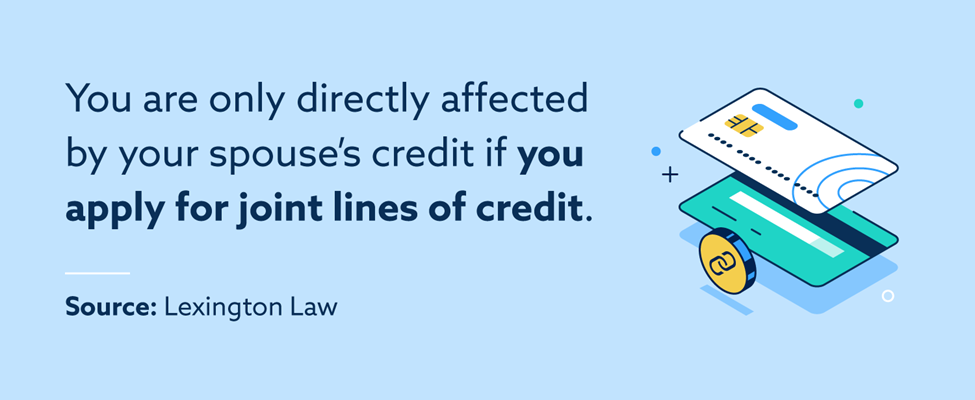

Fable 4: Your partner’s poor credit score will damage your credit score rating

Your partner’s poor credit score gained’t mechanically damage your individual credit score. Nonetheless, your credit score well being could change once you apply for joint accounts or loans. As soon as accepted for a joint account, you’re each accountable for the account. So, in case your partner is maxing out your credit score restrict or lacking funds, it would additionally have an effect on your credit score.

Fable 5: You might be mechanically added as a joint consumer in your partner’s account

While you get married, you don’t mechanically develop into a joint consumer in your partner’s account. Additionally, word that your credit score and financial institution accounts aren’t mechanically merged. To authorize your partner in your account or open a brand new account collectively, you should mutually talk about it along with your monetary establishment. {Couples} could select to merge accounts earlier than marriage or stay financially impartial.

Does your partner’s credit score have an effect on yours?

After tying the knot, you and your partner could begin looking forward to your subsequent important monetary milestone. When this occurs, you could surprise how your partner’s credit score can have an effect on your choices.

Each spouses’ credit score scores can have an effect on main credit score evaluations, together with once you:

- Merge and create joint accounts

- Try to purchase a house or make one other massive buy

- Apply for rates of interest and different qualifying affords

While you and your partner resolve to get a brand new account or mortgage collectively, the lender pulls each of your credit score studies to make the lending determination. Mismatched scores may have an effect on mortgage rates of interest, credit score limits and approval possibilities. Since funds and relationships are intertwined, realizing how your partner’s credit score may have an effect on you is necessary.

While you get married, do you share debt?

While you get married, you solely share debt should you open a joint account, cosign a mortgage or develop into a licensed consumer in your partner’s account. In any other case, premarriage debt is the duty of the one who accrued it.

Nonetheless, money owed collected throughout your marriage are handled otherwise relying on the place you reside. States following group property legal guidelines contemplate debt acquired through the marriage to belong equally to spouses. In frequent regulation states, money owed are typically the only real duty of the one who acquires them. In the event you want additional clarification on the property legal guidelines of your state earlier than, throughout or after marriage, seek the advice of an lawyer.

And keep in mind, even when a debt isn’t legally attributed to you, it could influence you. In case your associate has large quantities of debt, you may discover your high quality of life affected. It is best to talk about all money owed and absolutely perceive your associate’s monetary state of affairs earlier than getting married.

Bettering your credit score along with your partner

Each spouses’ credit score scores can profit when a pair combines their funds. For some, linking monetary accounts additionally helps {couples} outline, handle and enhance budgets, bills and credit score scores. These monetary modifications don’t must occur suddenly, and there’s no one-size-fits-all reply for spouses managing their funds.

Licensed customers

Including your partner as a licensed consumer to an account can generally assist enhance the decrease of your two scores. Spouses could contemplate this methodology if one particular person doesn’t have an extended credit score historical past or has a excessive credit score utilization ratio.

Joint traces of credit score

Even when {couples} preserve separate accounts, opening a joint line of credit score for on a regular basis purchases and payments can assist elevate credit score scores. Moreover, in case your partner has low credit score, opening a joint line of credit score to enhance their credit score well being can assist you qualify for a greater rate of interest collectively.

Cosigning loans

While you cosign a mortgage, the exercise on the mortgage will influence each of your credit score scores. In the event you signal for a mortgage collectively and make funds on time and in full, it could assist the particular person with the decrease credit score see a little bit of a lift.

Ought to married {couples} merge funds?

Merging funds as a pair is a sizzling subject, with monetary specialists arguing on each side. A 2023 research discovered that {couples} who merged funds have been happier of their relationship long-term. It’s because they have been extra prone to expertise monetary concord and so had much less battle round their funds.

In the end, although, it is a private determination each couple must make for themselves. {Couples} ought to do what works greatest for his or her partnership to stay wholesome, blissful and secure.

How marriage impacts your credit score report

So, does getting married have an effect on your credit score rating? Despite the fact that tying the knot doesn’t immediately have an effect on your credit score, there’s a superb likelihood there’ll be an influence on it in some unspecified time in the future. You’re beginning a life with this particular person, and your funds can be intently intertwined.

In the event you change your title or mix funds, monitor your credit score studies for inconsistencies or errors. Credit score report errors can negatively have an effect on your credit score well being and needs to be handled as quickly as attainable.

Lexington Regulation can assist you’re employed to handle inaccurate and unfair destructive objects in your report. Get a free customized credit score report evaluation at the moment.

Observe: The data supplied on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for common informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained inside the website don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.