{kind=link}

Mortgage fundamentals: “How to buy a mortgage.”

Every so often I deal with mortgage 101 as a result of it appears the apparent stuff isn’t at all times so apparent.

Whilst you would assume that looking for absolutely anything is comparatively simple, it’s typically not.

That is very true of mortgages, which include added confusion and potential pitfalls.

Let’s talk about how greatest to buy a house mortgage to acquire the very best rate of interest with the bottom charges. Oh, and make sure you wind up with a reliable lender.

First Off, Make Certain You Truly Store!

It’s cliché, but it surely’s true, and bears repeating. Only a few shoppers store round for his or her mortgage. And it could possibly price them, quite a bit.

In reality, one more survey, the newest from Zillow Residence Loans, revealed that potential residence patrons spend extra time researching their subsequent automotive buy or trip than their mortgage.

This even though the mortgage will probably be paid for the following 30 years in some circumstances, and weigh closely on their pocketbook.

These people additionally indicated that they spend about the identical period of time researching TVs to purchase as they do mortgage lenders.

I assume individuals watch a variety of TV, so it’s fairly necessary to get a top quality set. Jokes apart, this can be a downside if you wish to get monetary savings.

Why? As a result of there are actual research that show that buying round is the important thing to saving cash in your mortgage.

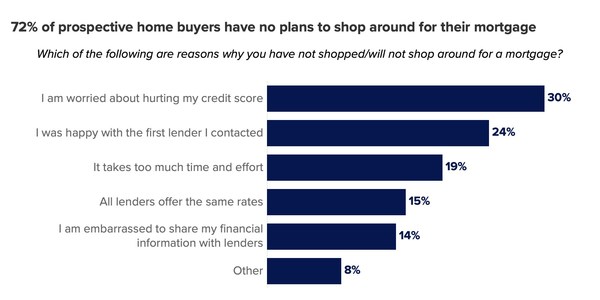

In fact, Zillow’s survey additionally discovered that 72% of potential residence patrons haven’t shopped round for a mortgage, nor have they got any plans to take action.

As for why, the highest cause is concern of hurting their credit score rating, which whereas considerably legitimate, shouldn’t maintain you again.

The second cause is solely being “pleased with the primary lender,” adopted by it taking an excessive amount of effort and time.

There’s additionally the assumption that each one lenders provide the identical charges, which is much from the reality.

Oh, and a few people are apparently embarrassed to share their monetary particulars, however can pay additional to maintain issues hush hush.

Mortgage Charges Can Fluctuate By 1% or Extra Between Lenders

To the purpose about all mortgage lenders providing the identical charges, it’s not true. Some lenders might provide related charges, however others might not.

And if you happen to contact that first lender you’re “pleased with” who occurs to supply the next price than the competitors, you may miss out huge time.

In spite of everything, most folk don’t store round, so the primary lender’s price is the one price they see.

Zillow researched mortgage price variation a couple of years in the past and located that quoted charges had been as a lot as 1.09% totally different.

That’s a big vary, and even larger for these with the bottom credit score scores. Debtors with scores between 620-639 noticed a variety of 1.33% between the bottom and highest APR for a 30-year mounted.

In the meantime, the CFPB pointed to a working paper that discovered “vital value dispersion” for retail mortgage charges.

A typical residence purchaser with a primary credit score rating and a 20% down cost “may see an expansion in rates of interest of fifty foundation factors” for a conforming mortgage.

That quantities to an additional $342 yearly for each $100,000 of mortgage quantity.

In the meantime, Freddie Mac performed a survey and located that only one extra mortgage price quote might save the common borrower between $966 and $2,086 over the lifetime of their residence mortgage.

And the common anticipated financial savings close to $3,000 if the borrower obtains 5 price quotes.

So a reasonably easy technique to “win” mortgage price buying is to easily store! Fairly simple, proper?

Examine Out Every day Charges Earlier than You Store to Decide Market Costs

Earlier than you store, because you now know you must store, get a gauge of market costs.

As you’ll different gadgets, like a TV or automotive, you want to perform a little research.

Mortgages generally is a little extra difficult, as mortgage sort, credit score rating, down cost, and different elements can weigh closely.

So first decide your mortgage state of affairs, plugging in these attributes like anticipated FICO rating, down cost, mortgage quantity, and so on.

Then take a look at real-time lock knowledge for mortgage charges that share the identical attributes as your mortgage state of affairs.

One website that’s useful on this regard is the Optimum Blue, which supplies such knowledge on typical 30- and 15-year mounted mortgage charges, together with charges for FHA, USDA, VA, and jumbo loans.

You possibly can filter by credit score rating tiers to see what the everyday mortgage price is for a sure mortgage sort and FICO rating mixture.

From there, you’ll at the very least have an concept of what lenders are providing most prospects. Do take into account that mortgage factors don’t appear to be factored in.

So if you happen to’re paying factors, guarantee your price is on the decrease finish of the vary. And if you happen to’re not paying factors, your price is perhaps larger to compensate.

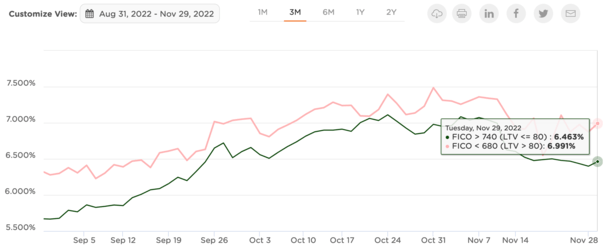

To offer an instance, the common lock for a 30-year mounted conforming mortgage with a FICO rating of 740+ and LTV of 80% or much less was 6.463% as of November twenty ninth, 2022.

In the meantime, the identical mortgage with a sub-680 FICO rating and an LTV above 80% got here in at a mean of 6.991%.

It’s mainly a half-point larger when you have a riskier mortgage state of affairs.

These numbers may give you ballpark figures to look out for, so if Lender A quotes you 7% for that first state of affairs, you may wish to transfer on.

Assuming you place within the time to succeed in out to Lender B and maybe Lender C, you may get a quote of 6.5% and even decrease.

Whereas charges are essential, additionally be aware of any lender charges or low cost factors required for the quoted price. Each price and charges matter, collectively the mortgage APR.

The place to Store for a Mortgage

Now that we all know how necessary buying a mortgage really is, and what to look out for as you store, let’s talk about the the place piece.

You possibly can store for a TV at Greatest Purchase and Amazon, amongst different locations. However what a couple of residence mortgage?

Properly, there are many locations to buy, together with on-line and brick-and-mortar choices.

Clearly, it may be best to begin on-line since you may store from a smartphone within the consolation of your house.

This will likely embrace aggregator web sites like Bankrate and Zillow, which show charges from quite a few corporations, much like a Kayak for vacationers.

You may mainly fill out a number of lead varieties and get quotes from 3-5 of those corporations inside a couple of hours or much less.

And also you is perhaps stunned at simply how totally different the quotes you obtain are.

Past that, you may get involved with your individual financial institution that holds your checking and/or financial savings account.

They may not provide the very best pricing (or they might!), but it surely’s a straightforward one to verify off the record because you’ve already obtained a relationship.

You can too attain out to a neighborhood credit score union or two and see what they’ll do. Usually, pricing will be fairly good they usually may additionally provide distinctive mortgage applications.

In the event you’re not tremendous into buying, you may also communicate with a mortgage dealer, who can store your house mortgage in your behalf.

Brokers usually have a number of wholesale lender companions they work with, so contacting one dealer means getting pricing from three or extra totally different corporations without delay.

Whilst you’re at it, examine mortgage brokers too to place your mortgage buying into overdrive. Talking to 3 brokers may imply getting 10 quotes.

Lastly, there’s the referral choice. Ask buddies/household/co-workers who they used and in the event that they’d advocate them. If that’s the case, give them a name and see what they’ll provide.

Bear in mind, arguably a very powerful half of buying a mortgage is definitely buying. Try this a lot and you need to be in fine condition.

Learn extra: 10 Tricks to Rating a Higher Deal on Your Residence Mortgage