The market rollercoaster for first-time householders within the UK might have ended however continues to be difficult. Following the dip in 2020, specialists say was attributable to the stamp responsibility vacation, charges of first-time consumers elevated once more in 2021. Nonetheless, home costs proceed to rise, and youthful generations should wait to purchase a home.

The common age of first-time consumers has crept as much as 34 years of age, 6 years older than 15 years in the past. Round 55% of 25-34-year-olds hire houses somewhat than purchase.

“Based mostly on our evaluation, there are about 2.4 million individuals who hire however may personal within the UK,” mentioned Trevor Stunden, CEO and Co-founder of Kettel Houses. “That doesn’t appear to be getting smaller. When you concentrate on the final six months and the challenges we see, general demand is usually softening due to rates of interest and different challenges. Nonetheless, there may be nonetheless very a lot demand accessible.”

“What we discovered was the three main challenges that first-time consumers are having, which can come as no shock is; the affordability, their credit score, and their deposit.”

“We discovered was that there’s a big hole for individuals who had some financial savings for a small deposit, that they had the means to get themselves to a bigger one, however additionally they didn’t perceive the method. What finally ends up occurring is that they flounder within the personal rental sector, not doing what they need to be doing to get themselves to homeownership.”

Assist to purchase fairness mortgage grew to become too large for the federal government

The federal government has led varied packages to encourage first-time consumers and make actual property extra reasonably priced regardless of rising costs.

The Assist to Purchase: fairness mortgage program was began in 2013 and was projected to run for ten years, coming to an finish in March 2023. It presents first-time consumers who can afford charges and curiosity funds an opportunity to purchase their first residence in new builds with a mortgage of 5%-40% of the property buy worth. Candidates should pay a deposit of at the very least 5% and prepare a compensation deposit of at the very least 25%.

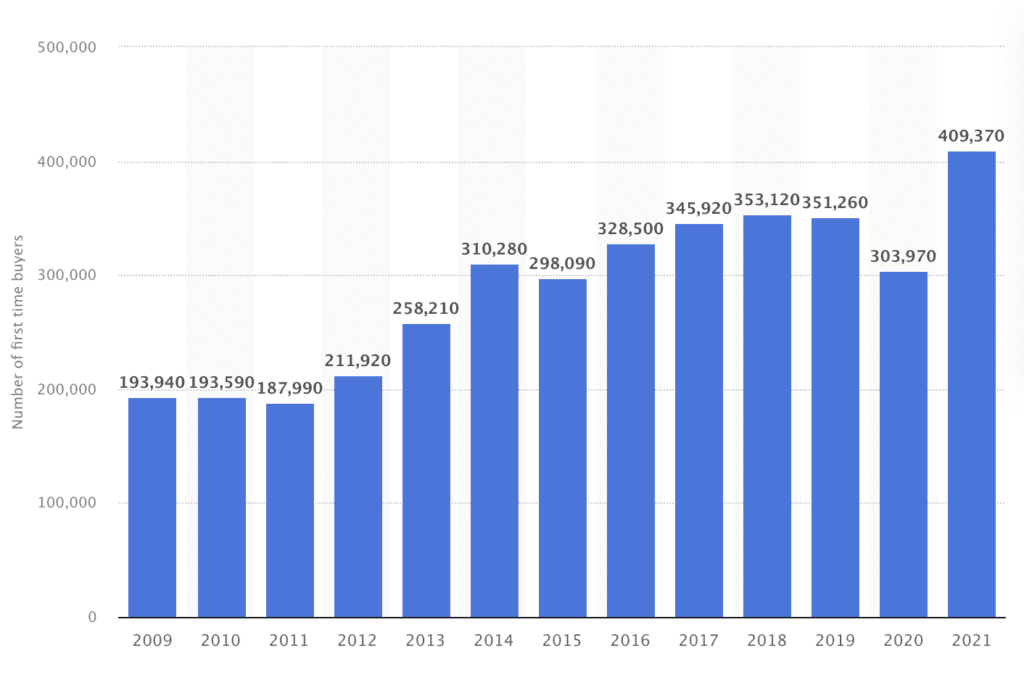

Since its inception, the scheme has facilitated 350,000 first-time buys. Based on Stunden’s contact in Houses England, Nick Merkley, it has turn into too giant a sum on the general public steadiness sheet, amounting to round £23 billion in debt.

“It’s a superb program; it’s simply turn into too large for the federal government,” mentioned Stunden. “The limitation of that program is that it’s solely on new builds. Kettel primarily focuses on current builds. One profit we offer is that we’re getting folks into houses that aren’t costing the planet when it comes to emissions.”

“Current builds even have a way more secure development fee. In case you’re shifting into a brand new construct, usually, you’ll be in adverse fairness for the primary three to 4 years due to the premium related to shopping for a brand new construct.”

“Moreover, there’s a limitation on the variety of new builds accessible. Suppose you concentrate on the sorts of properties that we purchase. Based mostly on land registry knowledge, anyplace between 350,000 – 400,000 items commerce inside our core standards yearly.”

As well as, customers of the Assist to Purchase scheme should pay the federal government a share of the elevated worth of the property once they repay the mortgage or resolve to promote their residence.

Shared possession scheme flawed

The opposite authorities program aimed toward boosting first residence possession is the Shared Possession Scheme. Candidates should buy a share of a house with a housing affiliation, native council, or different group. They have to pay a deposit from 5%-10% of the property worth and buy between 25% and 75% of the remaining home worth by means of financial savings or a mortgage.

Candidates then pay hire on the remaining share of the property to the group providing the scheme, with the choice to “staircase” by shopping for extra shares over time.

“Our private view on that is that it’s a little bit of a flawed program,” mentioned Stunden. “The one place the place I see it to be helpful for purchasers is in a expensive surroundings like Central London, the place any individual desires the safety of tenure, they usually don’t have any actual want to personal the house. The extent of true homeownership that anyone strikes from within the shared possession product is extraordinarily low; I feel it’s round 2% a yr. It’s very, very dangerous.”

“There are additionally disincentives. Let’s say you personal a portion of the house; let’s say it’s 25%. In case you staircase up, reselling your property at a better staircase, let’s say you bought to 50%, you truly turn into unattractive for a resale market as a result of the individuals who need to get onto the shared possession aren’t trying to purchase 50%, they’re trying to purchase the minimal worth.”

The shared possession phrases additionally change in line with the market values. “It’s been difficult for folks prior to now few years to both save the quantity wanted or perceive the expansion fee as a result of they solely personal a portion,” he continued.

Kettel has structured itself to resolve these points

“The massive distinction between us and any of those different packages is that we’re fixing the property worth, hire, and financial savings throughout that interval. So it provides you a clearer understanding of what you could do to attain your aim of homeownership,” mentioned Stunden.

Candidates to Kettel’s rent-to-own program select their residence and may very well be granted help so long as it resides inside Kettel’s metrics. “Our acquisitions workforce makes use of about 150 knowledge factors to undergo and be sure that the property matches our standards. We solely approve single-family houses, not flats, as a result of we would like our clients to maneuver into a house they will personal for a few years.”

“Traditionally, from a knowledge perspective, for those who stay in a two-bed or one-bed flat, you reside in it till you develop out of it. Whereas these are freehold homes, they’re a lot cleaner possession constructions and a lot better from an possession perspective.”

The appliance course of is just like a mortgage, with much less give attention to credit score scores. “We have now a bit extra flexibility as a result of we’re not a credit score product. We’re a regular landlord-tenant relationship.”

Family revenue is assessed, and a deposit of at the very least 2% is required. Kettel then calls the applicant and supplies a price range.

On approval, the fastened rental settlement is about for the primary 36 months, with a sure share going right into a linked lifetime ISA. The quantity that goes in the direction of financial savings is calculated with the intention for the house owner to succeed in 10% of the property worth, which is fastened from the second of entry into the settlement. The corporate reviews all rental funds to credit standing companies, constructing the applicant’s credit standing.

“One of many key items for our clients is that they’ve a transparent roadmap of how a lot they’re spending each month and what the repurchase worth will probably be it doesn’t matter what,” he continued. “The additional benefit is that they have an expert purchaser to undergo all the main points of the acquisition with a degree of scrutiny that almost all first-time consumers wouldn’t have the ability to do.”

Nationwide exhibits curiosity

Kettel’s scheme has attracted trade consideration, with Nationwide being one of many first to speculate.

“The enterprise has a social influence element,” Stunden defined. “Getting folks on the housing ladder is likely one of the greatest methods to supply any individual the steadiness for his or her household, and for them to speculate each in themselves and their communities. It’s additionally the best manner of making wealth. Within the UK, most wealth is saved in actual property.”

“These issues all coupled collectively in Nationwide. I consider they’re the most important lender to first-time consumers, so it’s a really clear alternative for them to help the ecosystem they’re a part of.”

What could be carried out to enhance the market?

Kettel’s product may ease the best way for first-time house owners. Nonetheless, the market itself is also adjusted to create a decrease barrier to entry for the demographic.

Stunden believes three essential issues may change to assist the first-time purchaser:

- “As the typical residence worth will increase, the federal government wants to extend the brink of stamp responsibility reduction. All the market is shifting, and I feel stamp responsibility wants to maneuver with it concerning the thresholds.”

- “I want to see the federal government improve the lifetime ISA bonus program, even when it’s structured in a manner the place you can begin saving earlier than you’re getting taxed. I feel it could be helpful.”

- “Schooling, and educating first-time consumers. Sadly, it’s not one thing they educate you in class. It’s the most important buy of your life and probably the most annoying stuff you’ll ever do (based mostly on a number of surveys). So having a degree of training and a clear construction could be very helpful.”

{kind=link}