{kind=link}

The globe is significantly going electronic, consisting of the financial system. The economic climate has actually been swamped with electronic possessions and also mobile applications that customers are crowding to over conventional cash and also banks. Cryptocurrencies like bitcoin are taking the lead on the electronic improvement in a worldwide economic climate where rising cost of living has actually raised its head and also apparently plans to remain for some time. The surge of bitcoin has actually tested the heritage monetary system and also put a fire under the feet of nations that have actually not currently done so to go electronic.

It is hard for banknotes to take on fast digital repayments on the blockchain. As well as the even more customers hold right into electronic money, the much less they will possibly make down payments right into conventional financial institutions, which intimidates to interfere with the version of banks.

Reserve banks electronic money (CBDCs) are primarily electronic variations of cash money denominated in the neighborhood fiat money of a country or location. Worldwide reserve banks are significantly seeking them as they prepare to take on the surge of electronic money in the economic sector. For its component, the European Reserve Bank (ECB) is discovering the assimilation of an electronic euro.

In this write-up, we will certainly discover just how a CBDC really functions anyhow along with when an electronic euro may really emerge. We will certainly additionally think about the benefits and drawbacks that policymakers are considering along with the function of the Baltic countries in the critical study procedure.

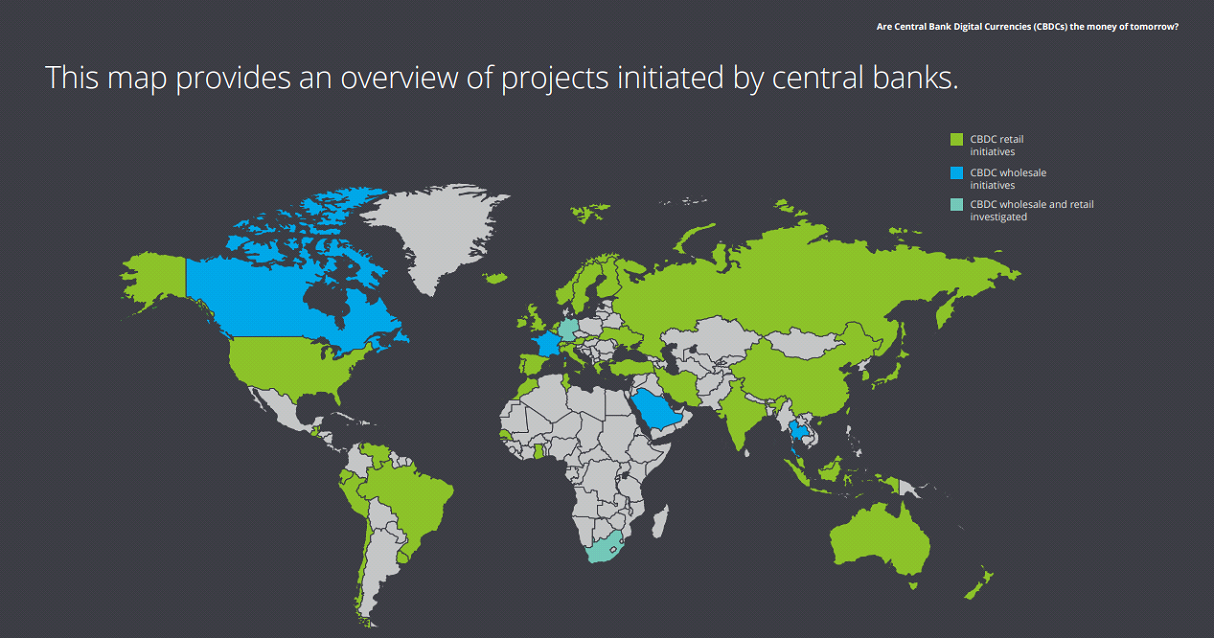

El Salvador has actually taken the remarkable action to make bitcoin lawful tender for customers and also sellers in the Central American country. The course that a lot of nations are taking, nonetheless, is to go after CBDCs. In between 70-90% of worldwide main financial institutions are in the procedure of thinking about the application of a CBDC.

For authorities, CBDCs can supply the very best of both globes– a money provided by reserve banks that flaunts the active features of an electronic property. One nation that is apparently not decreasing this roadway is Australia. The Book Financial institution of Australia appears skeptical that an electronic buck is required, though it prepares to dig a little bit deeper on the subject.

On The Other Hand, the ECB has actually made CBDCs a concern, yet the wheels of development turn gradually for a lot of federal governments, with the exemption of electronically wise countries like Estonia. The ECB is making progression. Furthermore, there are nations beyond the eurozone that are making their very own electronic money strategies, a few of which are additionally in advance than others.

Internationally, China was a first-mover to release an on the internet variation of its fiat money, the electronic yuan. The Federal Book has mostly had its head stuck in the sand when it comes to technology development and also electronic money.

Not remarkably, Europe has various takes when it pertains to electronic money. Euro banknotes have actually belonged of the EU economic climate for near twenty years. The ECB is not prepared to get rid of cash money completely, yet policymakers are open to technology development. It is an advantage, thinking about digital repayments are rising, having actually climbed up greater than 100% greater in the 2010-2018 duration in the eurozone.

Resource: Twitter

As well as while Europe’s reserve bank has yet to make a main get in touch with the prospective function of a CBDC in Europe, an electronic euro can see the light of day by 2025, authorities have actually claimed. In this write-up, we’ll discover where the ECB depends on CBDCs and also the course some nations beyond the euro location are taking.

CBDC Technicians

Essentially, a CBDC resembles a digital variation of cash money just it is much faster, sleeker and also more affordable to send out. A CBDC can be utilized to earn money transfers, spend for items and also solutions at brick-and-mortar places, or make acquisitions online in a comparable manner in which a card would certainly be utilized.

When it comes to an electronic euro, it would certainly operate like electronic banknotes that are provided by reserve banks consisting of the ECB and also assured by them. It would certainly be offered to customers and also organizations in the eurozone. An electronic euro or any type of CBDC for that issue would certainly transform the manner in which customers spend for daily acquisitions. Generally, it would certainly supply the public a brand-new alternative for repayments, one that the ECB should make certain is protected and also commonly approved.

Lots of people have actually come across electronic possessions, particularly considering that bitcoin’s market cap has balloons to greater than EUR 1 trillion. Not everybody, nonetheless, recognizes with what a CBDC is everything about. No 2 CBDCs will certainly be precisely alike, and also while the blockchain is matched for them, some reserve banks can practically enter a various instructions. CBDCs are the top manner in which financial institutions are anticipated to utilize the blockchain, nonetheless, which is the underlying innovation of electronic possessions.

There is a two-pronged version for a CBDC. A retail variation of a CBDC would certainly be utilized by organizations and also people. These stand for the repayments that customers make to sellers, and also what these deals might be doing not have in worth they offset in quantity. Interbank CBDCs, at the same time, are what financial institutions would certainly utilize for interbank repayments.

Resource: Deloitte

CBDC Pros

The International Monetary Fund has actually laid out the downsides and also benefits to a CBDC system. They promote an extra reliable settlement system as the essential benefit offered the costly nature of handling banknotes. Furthermore, the bankless and also underbanked sections of the populace would certainly have a far better possibility of monetary addition considering that engagement in a CBDC would certainly not need having a savings account.

The IMF additionally proclaims better security that would certainly be related to a CBDC, along with less obstacles to access for start-ups aiming to get in the repayments battle royal. Authorities indicated Sweden and also China, for instance, where they claim there is “a raising focus of settlement systems in the hands of a couple of, huge firms.” China’s Alipay and also WeChat Pay and also Sweden’s Swish mobile settlement system entered your mind.

IMF authorities additionally pointed out CBDCs as a method to “respond to brand-new electronic money.” They claim a main bank-backed electronic money would certainly aid to reduce down the fostering of stablecoins, which are electronic possessions provided by the personal industry yet typically secured to fiat cash, like the USD or EUR. They recommend that stablecoins can be testing to control and also “can posture threats to monetary security and also financial plan transmission.”

Various other pros for a CBDC consist of the rate in which repayments can be resolved. The digital nature of an electronic money is such that the system remains to run 24/7 rather than needing to await the neighborhood time of a matching financial institution to capture up. CBDCs can run all the time, and also repayments can be resolved immediately.

The blockchain, which is an unalterable electronic journal, has actually additionally made sending out repayments more affordable and also a lot more reliable for cross-border and also neighborhood repayments. CBDCs are claimed to supply the very best of both globes– the security of reserve bank cash integrated with the performance that electronic possessions offer.

CBDC Disadvantages

With any type of arising property course there are constantly threats, and also the IMF has actually called a couple of. IMF authorities shed rest regarding the opportunity of customers changing their financial savings from down payments held at banks to CBDCs rather. This may push financial institutions to enhance down payment prices to contend and also accessibility riskier financing, every one of which can put their annual report in danger with the possibility for a systemic danger to the wider economic climate.

The IMF counters this danger with the suggestion that CBDCs would certainly not create rate of interest and also consequently their danger to financial institution down payments can be much less serious than been afraid. By the way, there are methods to create rate of interest in the cryptocurrency industry with a market called decentralized money, or DeFi, where the worth of the marketplace presently goes beyond USD 264 billion.

In addition, a just recently released record by the BIS and also various other reserve banks states authorities are worried regarding the opportunity of financial institution runs in times of recession. They claim that the reduced price nature of electronic money deals can result in financial institution runs throughout one more monetary situation.

Academics are stressed over a CBDC interfering with the conventional monetary system and also alert that it can combat technology development in the economic sector. The tendency for cybercrimes consisting of hacks raises as the globe goes electronic. Furthermore, a CBDC would certainly be much less personal than banknotes as there would likely be an electronic identification linked to every purchase. ECB authorities have actually preserved that an electronic euro would certainly strike an equilibrium in between personal privacy and also protection.

The ECB and also a Digital Euro

CBDCs have actually formally gotten on the radar of the ECB this year. Over the summer season, policymakers introduced an official examination right into the idea on the heels of the favorable arise from an earlier study task that included Estonia and also various other nations.

Along with examining the prospective threats and also advantages, policymakers are discovering attributes like just how an electronic euro would certainly be and also look dispersed to organizations and also the general public alike. The ECB should examine just how an electronic euro would certainly impact the repayments landscape along with any type of brand-new plans that may require to be crafted. It is this extremely probe that will certainly establish whether the reserve bank determines to move on with an electronic euro.

Morgan Stanley quotes that an electronic euro would certainly breathe in 8%, or EUR 873 billion, of customer financial institution down payments. This can toss the “ordinary loan-to-deposit proportion” off kilter for a few of the smaller sized countries in the eurozone, consisting of the Baltics. In this instance, Morgan Stanley experts think that euro homeowners 16 years of ages and also up would certainly each transfer EUR 3,000 to an electronic pocketbook managed by the ECB to begin, which is a conventional circumstance.

ECB exec board participant Fabio Panetta lately kept in mind that the ECB is still discovering whether to release a CBDC on the blockchain for a retail usage situation. He recognizes that cash money’s function in culture gets on the decrease, and also if the pattern lingers down an electronic course, banknotes can go the means of the shipping stamp. Also if the economic climate is going electronic, the ECB overall does not anticipate that CBDCs will certainly offer as a substitute for cash money yet instead will certainly supplement banknotes. By using an electronic money, eurozone nations stand a far better possibility of completing with the personal industry’s development that has actually led to the development of bitcoin.

The reserve bank additionally touched a financial exec to lead its electronic euro program. Evelien Witlox, that formerly led worldwide repayments at ING, will certainly come to be program supervisor for the ECB’s electronic euro program in very early 2022.

For his component, Panetta, that was previously at the helm of Italy’s reserve bank, stressed that an electronic euro would certainly not be developed to go head-to-head with cryptocurrencies like bitcoin yet rather to offer one more alternative. He additionally supposedly claimed that more than likely, CBDCs will eventually acquire lawful tender condition in their corresponding nations yet this is not a provided.

In his newest progression upgrade, Panetta clarified just how with a market cap of greater than USD 2 trillion, the worth of cryptocurrency possessions has actually gone beyond that of securitized possessions pre-Global Financial Dilemma. He stated governing technicalities that should still be attended to in the crypto markets, keeping in mind that in a years, if customers do not obtain their electronic possessions from the general public industry, they will certainly do so in other places. Panetta additionally stressed that the goal is to provide electronic possessions without endangering monetary security vis-à-vis criminal task.

Resource: Twitter

A objection of the ECB’s electronic euro consultatory team has actually been that while ECB board participants claim “several top quality specialists from the economic sector want to add to the electronic euro task,” they seem missing out on a vital component. There are apparently no blockchain programmers or decentralized money (DeFi) jobs on the checklist of consultants, which asks the inquiry of just how authorities will certainly have the ability to browse the arising blockchain waters by themselves.

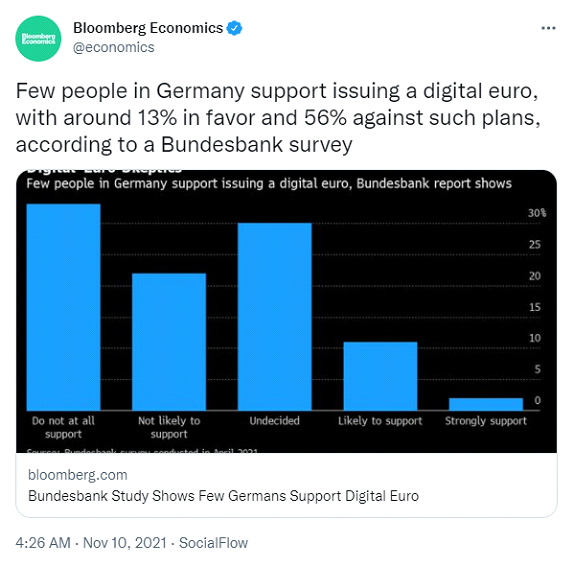

Outdoors of crypto, the electronic euro has various other movie critics. According to a Bundesbank survey pointed out by Bloomberg Business economics, in Germany, a lot of residents are not for providing an electronic euro, with over half of study individuals versus the effort. Roughly 13% of survey individuals sustain an electronic euro. Resource:

Baltic Countries Tip Up

When it pertains to electronic repayments, Estonia is light years in advance of much of the remainder of the globe. The Baltic nation has actually currently produced a “electronic culture” of types that is proclaimed as a version for various other federal governments to mimic. Therefore, its sight of an electronic euro holds a lot of weight.

Estonia’s Eesti Pank, the ECB and also numerous various other reserve banks consisting of those from Spain, Germany, Italy, Greece, Ireland, Latvia, and also the Netherlands lately collaborated to examine the effects of an electronic euro. This study was different from the ECB’s two-year examination right into an electronic euro that is presently underway. The outcomes of the study were assuring for an electronic euro.

In the electronic euro experiment, authorities produced settlement deals with electronic cash utilizing individuals from nations throughout Estonia, Latvia, Lithuania and also Spain. According to their searchings for, a blockchain-based electronic euro system appeals all cyndrical tubes: it can sustain almost an “limitless variety of repayments” concurrently amidst a “huge cash supply” and also is a lot more eco-friendly vs. the conventional card settlement framework. They additionally located

the blockchain-based system to be scalable to ensure that maybe broadened to take care of much more electronic euro repayments. For their research study’s functions, the electronic euro sustained 300,000 settlement deals per 2nd, and also deals were finished in much less than a number of secs. The carbon impact was much less than conventional card repayments.

Estonian authorities additionally reviewed a digital ID, or eID, that would certainly be linked to an electronic euro, which some may suggest would certainly be an infraction of personal privacy. The objective of the eID, nonetheless, would certainly be to make certain both protection and also personal privacy to ensure that information are restricted to the celebrations associated with a purchase, yet anti-money-laundering methods are still supported. Estonia currently proclaims an electronic ID system for its populace of 1.3 million. Eesti Pank policymakers additionally located that the blockchain-based repayments system struck an equilibrium in between personal privacy and also protection, such as anti-money-laundering controls. Latvia has actually additionally evaluated in on the possibility of an electronic euro. The Financial institution of Latvia supposedly identified that

if Europe stops working to act upon an electronic euro, it will certainly come to be prone to both “tactical and also geopolitical threats.”

Final Thought

The ECB’s electronic euro examination is still in the very early innings, yet the wheels remain in movement, which is greater than the USA can claim. As reserve banks drag their feet on applying an electronic euro or various other CBDC, whole nations are moving on by incorporating the economic sector’s electronic money. El Salvador is a vital instance, having actually made bitcoin lawful tender in the Central American country and also preparing the launch of a Bitcoin City. For Europe, cryptocurrency fostering is currently handy. The main, north, and also western European area leads the globe for its cryptocurrency economic climate, which has a worth of USD 1 trillion connected in the 12-month duration leading up to mid-2021, according to

crypto market information company Chainalysis. This area accounted for one-quarter of the globe’s crypto task in between the summertimes of 2020 and also 2021 sustained in component by the surge of the DeFi market. The UK blazes a trail for crypto deals throughout every one of Europe. An electronic euro would certainly need a huge task in regards to framework, costs, fostering, and also a lot more. Authorities are in a little bit of a catch 22. While they remain to do their study, economic sector development is just expanding more powerful, as is cryptocurrency fostering. The ECB’s Panetta has actually sworn to present an electronic euro model by the year 2023. At the very least already, the reserve bank will certainly have tipped its hand to the style of its prospective CBDC. As well as while the ECB does not intend to hurry right into an electronic euro, Panetta has made it clear

that likewise, regulatory authorities intend to “go quick.”

Do not think twice to share this write-up!(*)