{kind=link}

Credit rating are straightforward as well as exceptionally facility. Maintaining your credit rating in the outstanding or excellent variety can take a little bit of initiative. If you recognize what can affect your rating, you can make the ideal monetary choices for your individual scenario, as well as that can make a massive distinction when attempting to

obtain car loans

or various other funding. Discover a lot more in our total overview to whatever that can affect your credit rating listed below. The 5 Major Credit History Elements Generally, there are 5 significant elements that compose your credit rating. Numerous activities, standings, as well as reported products in these groups can enhance or reduce your rating. Comprehending these 5 aspects is an initial step in recognizing what may affect your credit rating (as well as just how you can

fix your credit report

if required). 1. Settlement Background It matters whether you pay your costs on schedule. A background of on-time repayments reveals loan providers that you’re accountable with cash as well as pay your financial obligations as concurred. Therefore, repayment background is a significant consider your credit rating. This is one reason that acquiring something like an automobile on credit report can be

great for your credit rating

in the long-term (if you pay on schedule).

2. Credit Score Usage Credit score application describes just how much credit report you’re proactively making use of. It’s most pertinent to rotating charge account, like bank card or credit lines. With these accounts, you have a credit line as well as an equilibrium (the quantity you presently owe). Just how much you owe pertaining to the limitation is your credit report application proportion. If you have actually maxed out all your bank card as well as credit lines, loan providers see you as a possibly high-risk customer. It implies you might not have a great deal with on your individual funds if you require all that credit report. As well as you may likewise owe a whole lot in month-to-month repayments, which can enhance the danger that you’ll back-pedal car loans. For these factors, credit report application is virtually as large a variable for credit history as repayment background. Make certain you maintain equilibriums down if you’re making use of credit report cards to develop credit report 3. Credit Score Age Credit score age is the length of time you have actually had a credit report duration in addition to the ordinary age of your charge accounts. This aspect can adversely affect your rating if you have no credit score background or you’re extremely brand-new to credit report. You might not have a credit history rating at all if you do not have accounts at the very least 6 months old.

4. Credit Score Mix

Credit score mix describes having a great mix of sorts of debts. Particularly, loan providers like to see that you can take care of both installation as well as rotating credit report suitably. You do not have a great credit report mix if you just have a

individual lending

or just have a credit report card. That can be negative for your credit rating.

5. When somebody draws that info to assess you for credit report, difficult Questions

Difficult queries reveal up on your credit history record. Each can adversely affect your rating by a percentage, so a lot of difficult queries quickly duration can be negative.

Why You Have Greater Than One Credit History You can really have a excellent credit rating as well as a negative credit rating all at once. Due to the fact that the majority of individuals have even more than one credit report rating, that’s. Below’s why. Initially, there are several credit report bureaus. The 3 significant bureaus are TransUnion, Equifax, as well as Experian. These bureaus do not share the info offered regarding you by others as well as loan providers, as well as not all loan providers report to all 3 bureaus.

That implies the info in your credit report data with each bureau can be various. You might have a late repayment reported with one bureau as well as not the others, for instance.

2nd, there are various credit rating designs. These are formulas that compute your credit rating based upon the info in your credit report account with the bureaus. You might use the very same credit rating design to the info from each bureau as well as obtain 3 various credit history. With these aspects, everyone has lots of possible credit history. The specific number depends upon that is drawing it, what bureau’s info is made use of, as well as what racking up design is made use of.

A List of Every Little Thing That Can Influence Your Credit Score Rating All credit score ratings go up as well as down based on numerous aspects. Comprehending those aspects can aid you Late Settlements checking out a credit history record to recognize what to search for on your own. Default or Collections Accounts Various other products that can be sent out to collections as well as ultimately effect your credit rating consist of: Clinical costs Overdue energy or insurance coverage costs Parking tickets Overdue rental fee or down payments to proprietors Overdue billings for numerous solutions Over-limits or various other quantities owed to financial institutions Decreasing just how much financial debt you presently owe can likewise make it much easier to obtain brand-new financial debt for one more factor: It lowers your debt-to-income proportion. If you presently owe $3,000 a month as well as make $6,000 a month, loan providers might be much less most likely to accept you for a funding than if you just owed $1,000 a month as well as made $6,000. If you’re not saddled with old ones, you’re merely much better placed to pay brand-new financial obligations. When you close old accounts, you’re influencing the total age of your credit report. That can adversely affect your credit rating. Take into consideration the instance listed below to comprehend just how this functions. Sue has 4 charge account: A charge card open for ten years A charge card open for 5 years An individual installation lending open for 2 years Her ordinary age of credit report is presently 5 years. Due to the fact that she desires to lower her credit report application,

to include energy costs or various other repayments to your credit history record.

Late repayments are commonly reported by loan providers to several credit report bureaus. They constantly have an adverse influence on your rating. The more frequently you’re late with repayments– as well as the later on those repayments are– the even worse the effect. Credit score bureaus make use of a collection of codes to reveal whether an account has late repayments, when those late repayments happened as well as just how late they really were. Discover more regarding

If you back-pedal a funding or account– indicating you’re so late you’re sent out to collections– that’s reported to the credit report bureaus. If the account had not been initially reported, this can be real also. If you never ever pay your cellular phone expense as well as Verizon sends you to collections, the collection account reveals up on your credit history record also though your previous prompt Verizon repayments really did not. Defaults as well as collection accounts have an adverse influence on your credit rating.

Penalties or cash you may owe a collection for not returning publications

Closing Old Accounts

A vehicle loan open for 3 years

Currently File a claim against has 3 charge account:

The auto loan open for 3 years

The individual installation lending open for 2 years

The loan consolidation lending open for 0 years

Her ordinary age of credit report is currently just 1.7 years

Sue might have been far better off, in this theoretical scenario, maintaining the old charge card accounts open as well as simply not utilizing them. Opening New Accounts Opening up brand-new accounts can affect your credit report in a variety of means. A brand-new account can bring down the ordinary age of your credit report. Second, it might have entailed a credit report consult a tough questions. Third, it elevates your financial debt total amount. Every one of these can adversely affect your credit rating.

However in the long-term, a brand-new account uses one more chance to show your solid repayment background. It normally comes to be a favorable aspect for your credit report rating if you pay the brand-new account in a prompt fashion. This is why

locating a funding alternative that benefits somebody without credit report

is usually an initial step for constructing credit report from the ground up.

stay on your credit history record for 2 years

They do not have the very same effect on your rating that whole time. It’s likewise essential to keep in mind that when you’re going shopping prices for something like a vehicle or a home mortgage lending, the credit history designs recognize this. A number of difficult queries within a week or 2 for the very same objective will just count as one “occasion” for the objective of influencing your credit report rating. Foreclosures or repossessions

Repossessions as well as foreclosures have major unfavorable influence on your credit history. For loan providers, these are several of one of the most unfavorable products due to the fact that they show that somebody was so late on a funding that the residential or commercial property safeguarding the lending was confiscated to aid the financial institution recover its losses.

Personal Bankruptcies

Insolvencies are one more significant unfavorable product on your credit history record. Normally, the personal bankruptcy itself might not drop your rating by a massive quantity due to the fact that, by the time somebody data, they’re currently taking care of lots of late repayments, possible repossessions, or collection accounts. A personal bankruptcy can container it for the direct future if this isn’t the instance as well as your credit report is excellent. Insolvencies stay on your credit history record for approximately ten years from the declaring day Fortunately is that these treatments usually permit individuals to obtain or reorganize financial obligations remedy for frustrating monetary scenarios. That might develop the area for favorable monetary choices in the future, as well as those can bring about a far better credit rating. Task on a Financing You Guaranteed If you guarantee one more credit report or a funding chance for somebody, just how they handle their account might affect your credit report. Lots of loan providers report repayments as well as account info to the credit report data of the cosigner as well. Your credit report rating can endure if your close friend or family members participant is late with repayments or defaults on their lending. Being an Accredited Individual on A person’s Bank card Account Being included as an accredited individual to somebody else’s charge card account is one means to possibly improve your credit rating promptly

You obtain the advantage of the various other individual’s solid repayment background if the credit report card business likewise reports to the credit report bureau for licensed customers. If that individual adds their charge card equilibrium or is late with repayments, nonetheless, you can obtain the unfavorable effect of those aspects.

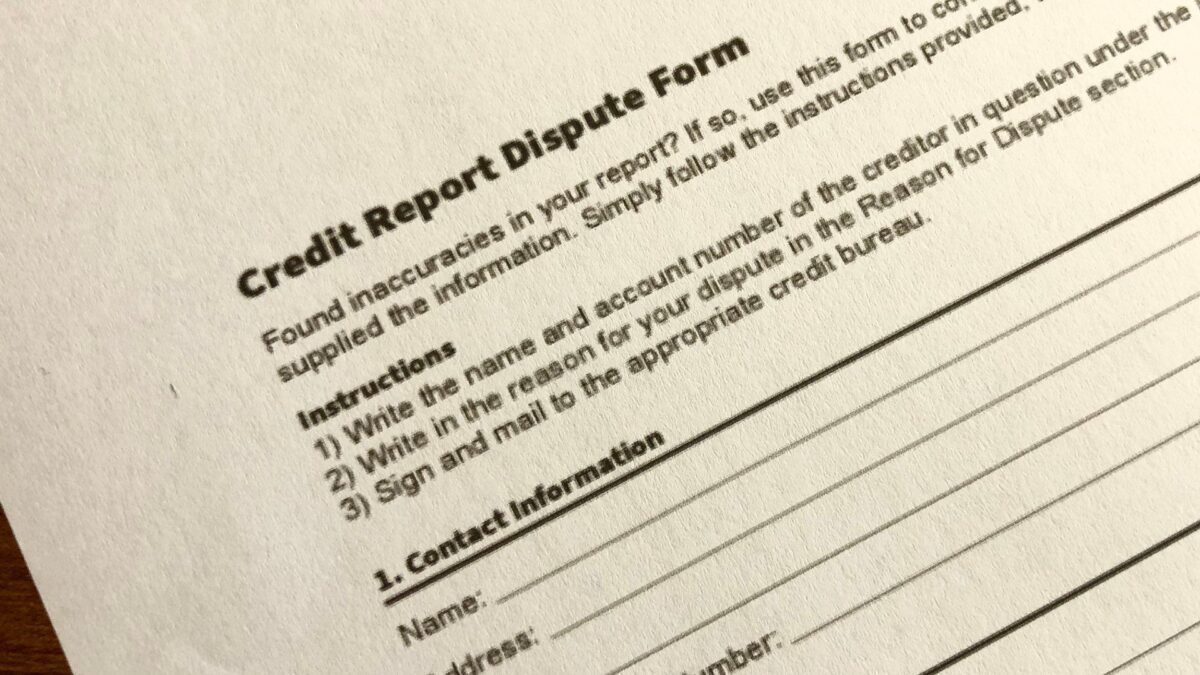

Mistakes/Incorrect Info(*) Around (*) 20% of individuals discover mistakes on their credit report records(*) If your record has imprecise unfavorable info, such as late repayments or defaults on car loans that aren’t also your own, that influences your credit rating. The good news is, you have a right to a exact as well as reasonable credit history record. You can ask the bureau in concern to examine as well as make adjustments if you examine your record as well as discover mistakes. Make your demand in creating for the very best possibility at a favorable result. (*) Time (*) Time plays a crucial duty in your credit rating. Many unfavorable products age off in about 7.5 years, which implies they quit influencing your rating. As well as for the most part, an adverse product has much less effect as time passes. You can constantly function to develop a much more favorable credit rating in the future because of this truth.(*) Comprehending (*) car loans as well as credit report(*) is essential for everybody. Whether you’re seeking a (*) individual lending(*) currently or simply wish to (*) guarantee your credit rating is healthy and balanced(*), recognizing what influences it is a fantastic primary step. Contact us to discover even more regarding our (*) accountable financing(*) method. Obtaining a funding just takes mins as well as, relying on your financial institution, you can have the cash as quickly as the following company day.(*) The referrals had in this short article are made for educational functions just. Important Loaning DBA Wise Finance does not ensure the precision of the info offered in this short article; is exempt for any type of misstatements, mistakes, or noninclusions; as well as is exempt for the repercussions of any type of activities or choices taken as an outcome of the info offered over.(*)