{kind=link}

The data offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra info.

Credit score rating and FICO® rating basically imply the identical factor. Whereas each measure your creditworthiness, your FICO rating makes use of a particular scoring system created by the Honest Isaac Company (FICO).

Your credit score rating is a personally assigned quantity generated by any credit score scoring mannequin that measures your creditworthiness. Lenders and collectors use this rating to find out whether or not they can approve you for loans and credit score, and if that’s the case, at what rates of interest.

Folks typically use the phrases “credit score rating” and “FICO rating” interchangeably. In actuality, a FICO® rating is just one form of credit score rating. Preserve studying for an entire rundown of the variations between a FICO rating and a credit score rating.

Desk of contents:

What’s a credit score rating?

A credit score rating is a three-digit quantity that predicts the probability that you’ll pay a mortgage again on time primarily based on information pulled out of your credit score stories. Your credit score rating is important as it will probably dictate what forms of monetary merchandise you’re authorized for (mortgages, bank cards, private loans, automobile loans) and the phrases and rates of interest on these merchandise. In actual fact, your credit score rating may even attain past your funds, as it may be collected by employers and landlords reviewing candidates.

What does a credit score rating signify to a lender?

The next rating alerts to lenders that you could be be a extra dependable borrower, and also you’ll possible get higher mortgage affords. In the meantime, a decrease rating signifies that you could be be a dangerous borrower and lenders might deny your software or provide you with the next rate of interest to offset the chance.

Who generates credit score scores?

Credit score scoring firms, similar to FICO, calculate credit score scores primarily based on shopper info from the three main credit score bureaus (Equifax®, Experian® and TransUnion®). These credit score bureaus obtain shopper information instantly from lenders and collectors, who report the data month-to-month.

What’s a FICO rating?

A FICO rating is a sort of credit score rating generated by the credit score scoring system developed by the Honest Isaac Company (FICO). The FICO rating originated in 1989 and is without doubt one of the mostly used credit score scoring techniques for lenders as we speak. In response to FICO, 90 p.c of all high lenders use FICO scores.

FICO scores can vary anyplace from 300 to 850. There are a number of variations of FICO scores, however the latest is the FICO Rating 10 mannequin. FICO releases new credit score scoring fashions each few years to adapt to modifications within the market. For instance, one of many most important updates seen within the FICO 10 mannequin is that debt from the latest 24 months is extra closely weighted than different debt.

Trade-specific FICO scores

Along with the usual FICO fashions, there are industry-specific FICO scores, such because the FICO Auto Rating and the FICO Bankcard Rating. These industry-specific scores are made for choose forms of credit score, similar to automobiles, mortgages and bank cards. Whereas commonplace FICO scores vary from 300 to 850, industry-specific scores vary from 250 to 900.

General, FICO industry-specific scores aren’t used as often as the usual mannequin.

Is a FICO rating the identical as a credit score rating?

A FICO rating is a sort of credit score rating. Your FICO rating might differ barely from different forms of credit score scores as a result of credit score scoring firms calculate scores otherwise.

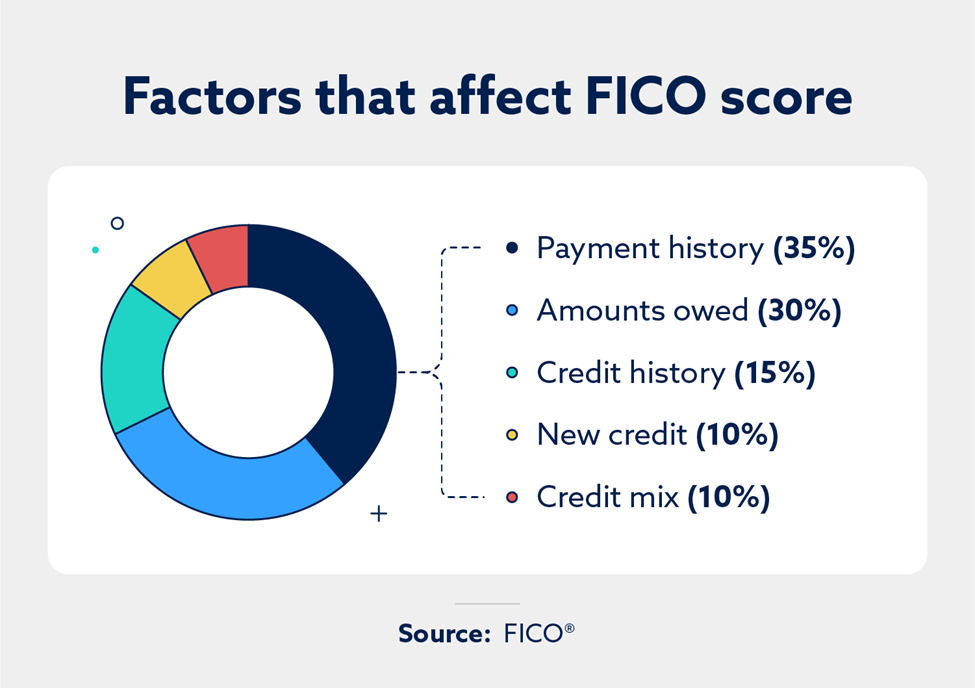

How is a FICO rating calculated?

Your FICO rating is made up of the next 5 components, all of which have an assigned weight:

- 35 p.c: Fee historical past

- 30 p.c: Quantities owed

- 15 p.c: Size of credit score historical past

- 10 p.c: New credit score

- 10 p.c: Credit score combine

What is an effective FICO rating?

Typically talking, something above 670 is seen as a good credit score rating. Nevertheless, this can differ from lender to lender.

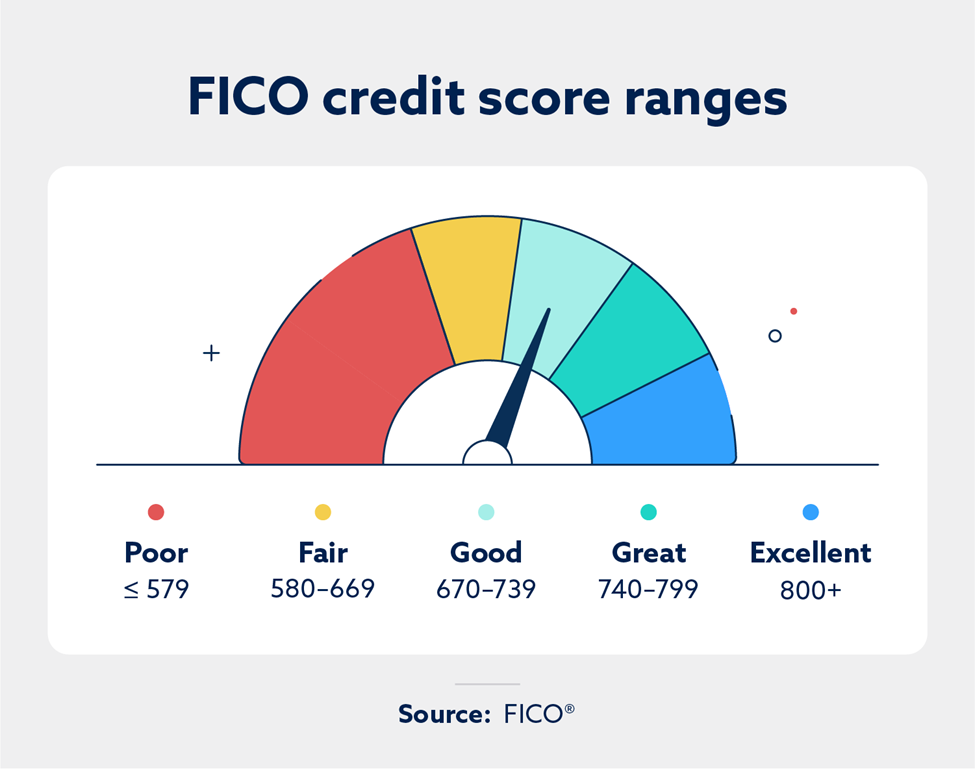

The FICO mannequin teams individuals’s scores into these classes:

- Distinctive: 800+

- Superb: 740 – 799

- Good: 670 – 739

- Honest: 580 – 669

- Poor: 579 and under

An distinctive rating means you’ll possible get rapidly authorized for all the pieces (or nearly all the pieces) you apply for, you’ll obtain the very best phrases and also you’ll safe the bottom rates of interest. Compared, a poor rating will often result in software denials, and if you areauthorized, it’ll be with excessive rates of interest and poor mortgage phrases.

The best way to get your FICO rating

You will get your FICO rating instantly from FICO or one in all its companions.

- Examine the FICO Open Entry Program: FICO has partnered with a number of establishments to offer your FICO rating quantity without spending a dime beneath its open entry program. Examine to see in case your financial institution or credit score and monetary counseling program is listed.

- Buy entry from FICO: You should purchase your rating and different providers from FICO.

- Buy from a certified FICO retailer: FICO-authorized retailers are Experian and Equifax.

If you obtain your rating from any supplier on-line, be certain to substantiate which scoring mannequin was used. Most lenders do use FICO scores when making lending choices, but it surely’s nonetheless useful to know the opposite scoring fashions—like VantageScore®.

FICO rating vs. VantageScore

The 2 dominant credit score scoring fashions are the FICO rating and VantageScore. VantageScore was created in 2006 by the three main credit score bureaus. Whereas VantageScore is much less widespread total, it’s gaining extra market share yearly.

The VantageScore and FICO rating fashions are very comparable—they each vary from 300 to 850 and launch new variations of their scoring mannequin each few years. Nonetheless, there are some important variations between the 2 fashions. For instance, FICO requires shoppers to have an account open for not less than six months earlier than a rating will be given, whereas VantageScore assigns a rating as quickly as an account seems in your credit score report.

Moreover, how VantageScore values varied points of your credit score information differs from FICO. VantageScore assigns the very best weight to credit score utilization, credit score combine and fee historical past and the bottom weight to new accounts and credit score historical past age.

Because of these variations, your VantageScore and FICO scores can differ. Sadly, even should you rating increased with one mannequin, you received’t often have the ability to use this information to your benefit. You typically received’t know if a lender will pull a FICO rating or a VantageScore.

Other forms of credit score scores

There are various different credit score scores generated and utilized by different lenders and firms. Frequent ones are academic credit score scores and enterprise credit score scores.

An academic credit score rating relies on a non-public lender or credit score bureau’s rating of your monetary info.

For instance, the PLUS rating was designed by Experian to present a fundamental concept of your danger degree and creditworthiness. Though they’re designed to measure credit score danger, lenders don’t use academic credit score scores.

Fashions just like the PLUS rating are meant for shopper use solely, so lenders don’t take into account them when reviewing your mortgage software.

Enterprise credit score scores predict your organization’s monetary stability and the way dependable you’re by way of managing firm funds.

For instance, Dun & Bradstreet’s D-U-N-S Quantity is used to determine your small business and is the important thing to finance-related details about your organization, like your small business credit score report, your D&B Delinquency Predictor Rating and extra.

All of your credit score scores will possible differ since quite a few scoring fashions are used, and these fashions weigh info otherwise. They might additionally pull info from one, two or all three credit score bureaus.

As an alternative of specializing in the particular standards for every rating, you must give attention to responsibly managing your credit score with FICO’s standards as a suggestion since that rating is mostly used.

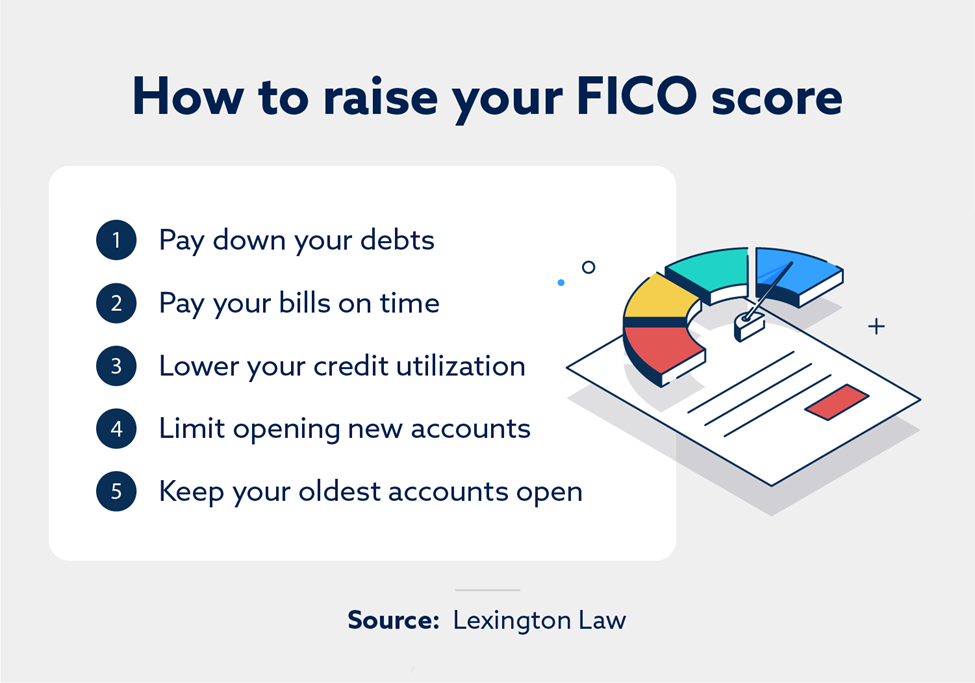

The best way to enhance your FICO rating

The excellent news is that should you’re unhappy together with your FICO rating, you may take steps to enhance it. By understanding the 5 components that make up your credit score rating, you may also decide what you may doubtlessly do to enhance your credit score, similar to:

- Paying down your money owed

- Paying your payments on time

- Conserving your credit score utilization low

- Solely opening new accounts when mandatory

- Avoiding too many laborious inquiries

- Conserving your oldest accounts open

It’s additionally vital to test your credit score stories often. Your credit score stories may give you a greater understanding of what’s hurting your credit score, and also you’ll need to be sure that your credit score stories don’t include any inaccurate or false info that’s unfairly affecting your credit score. If that’s the case, Lexington Regulation Agency will help you handle the errors to get the correct credit score report you deserve. Try our providers as we speak.

Observe: Articles have solely been reviewed by the indicated lawyer, not written by them. The data offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the website don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.