{kind=link}

June was the most effective month ever for my Peer to Peer lending Portfolio, not a lot for the Crypto Portfolio, however that in itself could also be a chance. Extra on that later.

Progress Portfolios continued in the precise route, though I really feel like we could also be due for a pullback within the not too distant future.

Simply as an FYI; I applied a few newsfeeds on my web site. One for Peer to Peer Lending Information, and the opposite for Cryptocurrency Information. To be completely open, I did this for me personally as they only pull collectively completely different sources that I often learn with out having to go to every particular person web site, however I assumed I’d make them public in case any of you of us discover them helpful.

Quick intro this month so let’s get proper into it with the detailed Peer to Peer lending replace first.

Peer to Peer Lending Websites & Portfolio Replace

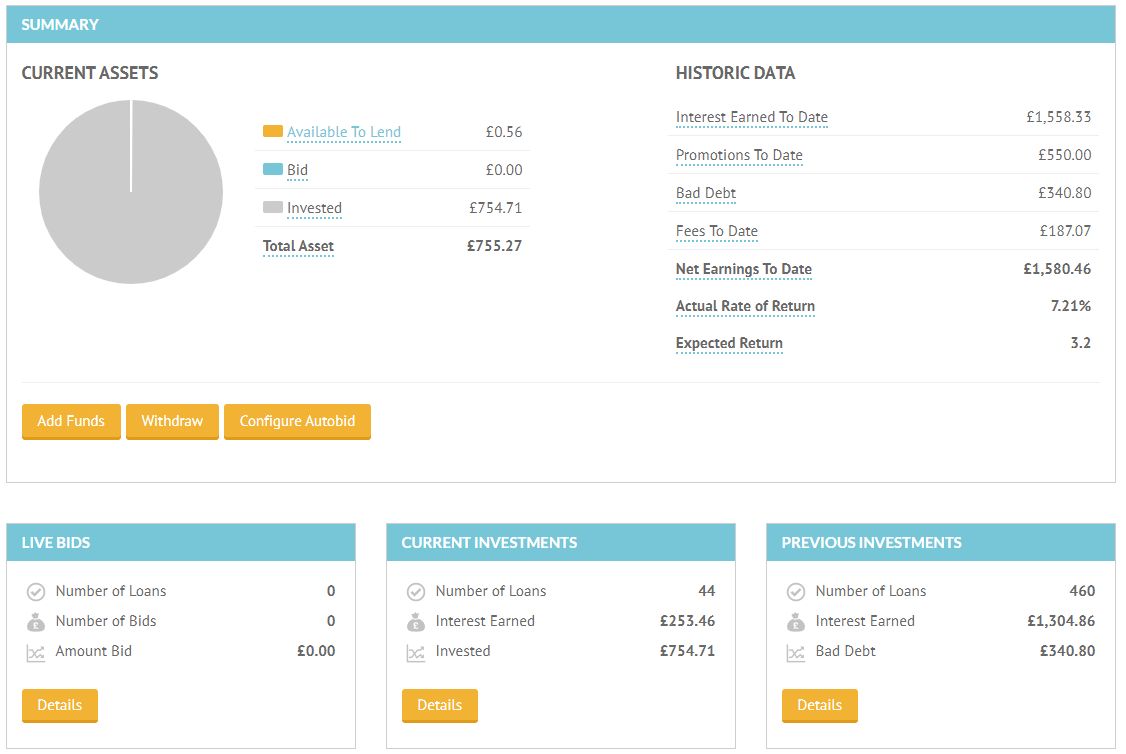

The Peer to Peer lending portfolio funding elevated solely barely from £189,751 in Might, to £194,318 in June.

General, it was the most effective month the portfolio has ever had with a complete earnings for the month of £3,288.67, due primarily to the brand new lender Assetz Trade, and likewise for as soon as, Funding Circle got here up trumps. Nice months from Kuflink and CrowdProperty additionally didn’t harm something. I’ll clarify in additional element under within the particular person updates.

You possibly can all the time see the dwell Peer to Peer Lending Portfolio knowledge right here >>

Disclaimers

The knowledge under is comprised of my opinions on present funding market situations and my private actions with my investments. It mustn’t in any means be construed as monetary recommendation. Please do your individual analysis earlier than making funding selections and don’t base them solely on what you learn on this web site. Please learn my full disclaimer of extra info.

A few of the hyperlinks on this web site are affiliate referral hyperlinks. For cashback affords, you’ll typically want to make use of these hyperlinks to qualify for the cashback. When you use these hyperlinks I can generally obtain a fee, at completely no value to you. This helps me to run the web site, write new platform critiques, publish month-to-month portfolio updates & typically preserve me excited about taking the time to share the data you might be at the moment studying. I don’t obtain commissions from all hyperlinks, and it has no impact on my ongoing opinions on investments, that are completely centered on producing Revenue and preserving capital.

Particular person Peer to Peer Platform Updates

Ablrate had a few new loans in June, however I didn’t put money into any. Not a lot new to report right here. Alblrate nonetheless appear to be doing okay however I’m nonetheless not motivated sufficient to take a position extra capital with them because the work concerned to seek out good loans with a small quantity of capital is just not price it (for me a minimum of). I’m nonetheless on the sidelines with Ablrate till I get a while and inclination to take a position more cash with them.

Here’s a view of my Ablrate account because it stands on the finish of June 2021.

My present Ablrate Investments. You might have observed that there at the moment are 2 loans on maintain (final month just one). This will occur although for simply late funds so I’m not worries about it.

My Ablrate Technique.

There are some nice returns accessible by Ablrate in the event you’re keen to place the time in to do the analysis and purchase the most effective loans. As much as 15% each year. The most effective charges of all UK Peer to Peer lending websites.

For some it is going to be completely well worth the effort. For me with my “Lazy Investor” angle, the time dedication required exceeds my enthusiasm in the mean time. That will change within the subsequent few weeks, however for now I don’t have the time to diversify a major quantity of capital in the way in which I would love.

When you do have the time to spare, Ablrate are top-of-the-line paying lenders on the market so far as returns go. The truth that they’re nonetheless round after the pandemic additionally has to say one thing about their enterprise mannequin and the saftey of the platform.

Ablrate Signup & Cashback Presents

£50 Ablrate Cashback on £1000+ funding for New Traders

Use this hyperlink to qualify for Ablrate cashback or to signup >>>

See Full Assetz Capital Evaluation

Assetz Capital shocked buyers initially of June with an e mail saying that they now have extra funding of their Entry Accounts than they’ve loans to place the capital into, in order that they have been returning a few of buyers capital.

I had round 10% of my capital returned, so I withdrew it and despatched it over to Kuflink the place returns are higher anyway frankly.

I nonetheless like Assetz Capital, however they’re going by some fallout from the COVID19 scenario (having an excessive amount of capital is just not essentially a foul factor, it simply requires extra loans which they might want to work on).

I nonetheless imagine in Assetz Capital and suppose they nonetheless are a comparatively secure wager. As quickly as they determine issues out, I’ll don’t have any qualms about investing extra capital with them.

Presently I’m principally invested within the 30 Day Entry Account at 4% as I don’t really feel just like the 90 Day Entry Account is price it for the additional 0.10% (complete 4.10%) for an additional 60 days lockup on the money. I could begin and have a look at a number of the Guide Lending Account loans if I get a while. There are a lot better charges accessible on the MLA, nonetheless there’s work wanted find the nice ones and naturally there isn’t a provision fund. Managing them takes work too so I’ll must see if I get motivated sufficient. The additional 3% or 4% accessible on loans within the MLA is probably going solely price it if I make a extra important capital funding.

Right here’s what my Assetz Capital account seems to be like now:

My Assetz Capital Technique.

I’m a little bit over £17k invested with Assetz Capital. As soon as they get extra loans accessible to allow them to settle for bigger investments, I’ll probably be shifting more cash over there.

Assetz Capital Signup & Cashback Presents

No present Cashback Presents

Use this hyperlink to examine for brand new affords or to open account >>>

See Full CrowdProperty Evaluation

CrowdProperty are maintaining the nice work. Nonetheless placing out 8-12 loans monthly it appears, I’m getting capital into each one I can.

June was the most effective month but for returns from CrowdProperty with a number of loans paying again this month there was a complete revenue of £256.37

The one single drawback (in the event you can name it that) with CrowdProperty simply now’s how briskly the loans fund. Actually 2.7 seconds the final one I invested into. It’s develop into like a sport the place I sit on the laptop when the loans are launched (sometimes at 10:00am and in 10 minute intervals after that if there are multiple mortgage in a day) and as quickly because the mortgage will get launched, it’s a typing and clicking frenzy 🙂 to this point I’ve managed to get into each mortgage I’ve tried for, so it’s attainable, you simply must be proactive about it. Auto-invest is mainly a waste of time if you wish to get any important capital invested right into a mortgage. When you can’t be on the laptop once they’re launched although, it’s the one possibility.

I’m actually having fun with CrowdProperty in the mean time. Nice danger/reward and mainly does what it says on the tin.

The XIRR jumps up and down with each CrowdProperty and Kuflink as returns solely sometimes come again when loans are repaid, so it’s not a straight earnings line like Loanpad or easyMoney.

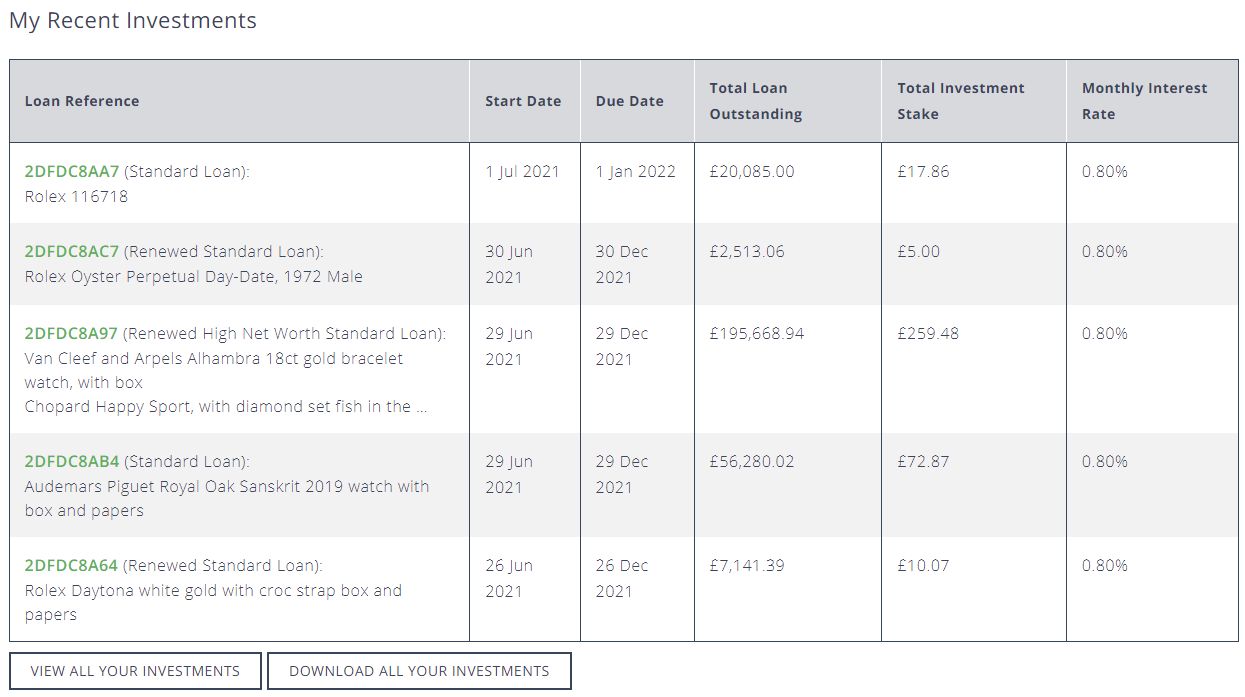

Right here’s a number of the loans I received into in June:

Right here’s a screenshot of my CrowdProperty account on the finish of June 2021.

Listed below are the upcoming loans for July 2021

My CrowdProperty Technique.

My technique because the starting with CrowdProperty is to take a position £500 into virtually each mortgage they’ve for good diversification. If the LTV is low, and it’s a tranche 1, I’ll make investments £1000. I do some due diligence on every mortgage earlier than it goes dwell. Infrequently I see one thing I don’t just like the look of and I don’t put money into that individual mortgage. I’ll usually look carefully at greater stage (numbers) tranches and go over a few of them at occasions. General although, that occurs very sometimes so it’s just about £500 or £1000 into every mortgage.

CrowdProperty Signup & Cashback Presents

No present cashback affords from CrowdProperty.

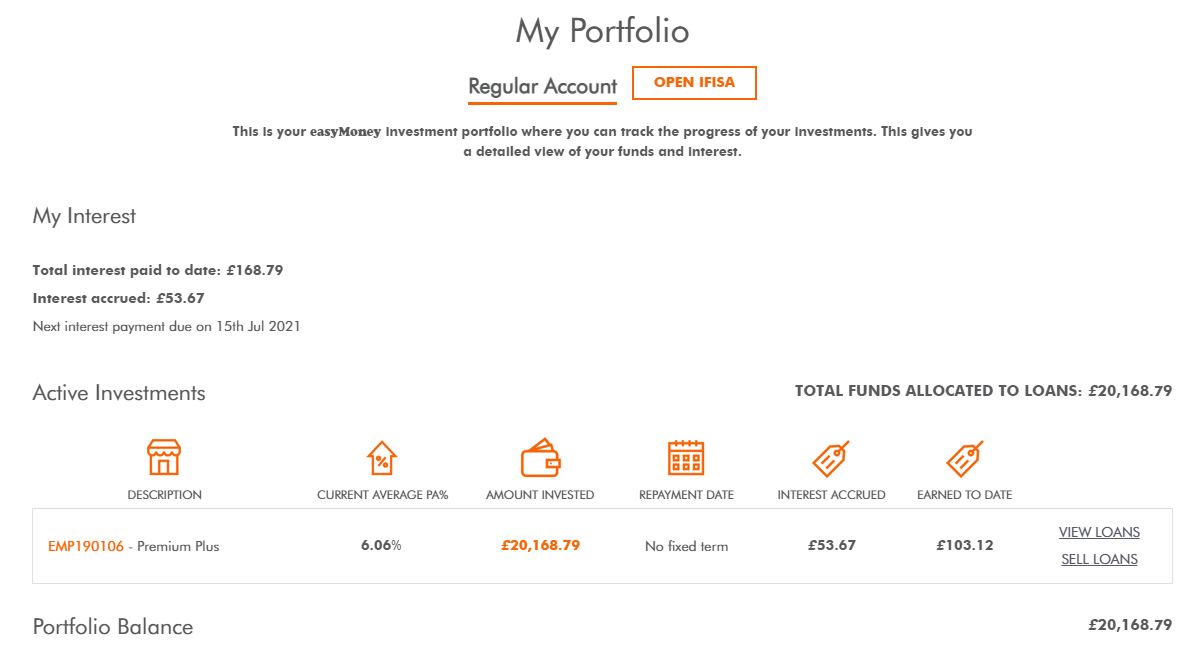

easyMoney was one other new funding for me in April. I wrote extra intimately about them in the Might replace.

I’m getting increasingly assured about easyMoney. They appear very very like Loanpad however with 6%+ return. The loans appear to be very effectively vetted and none have defaulted up to now. That claims lots after the entire COVID scenario.

I’ll probably sooner or later transfer more cash over there, however for now I’m simply watching the curiosity are available in each month.

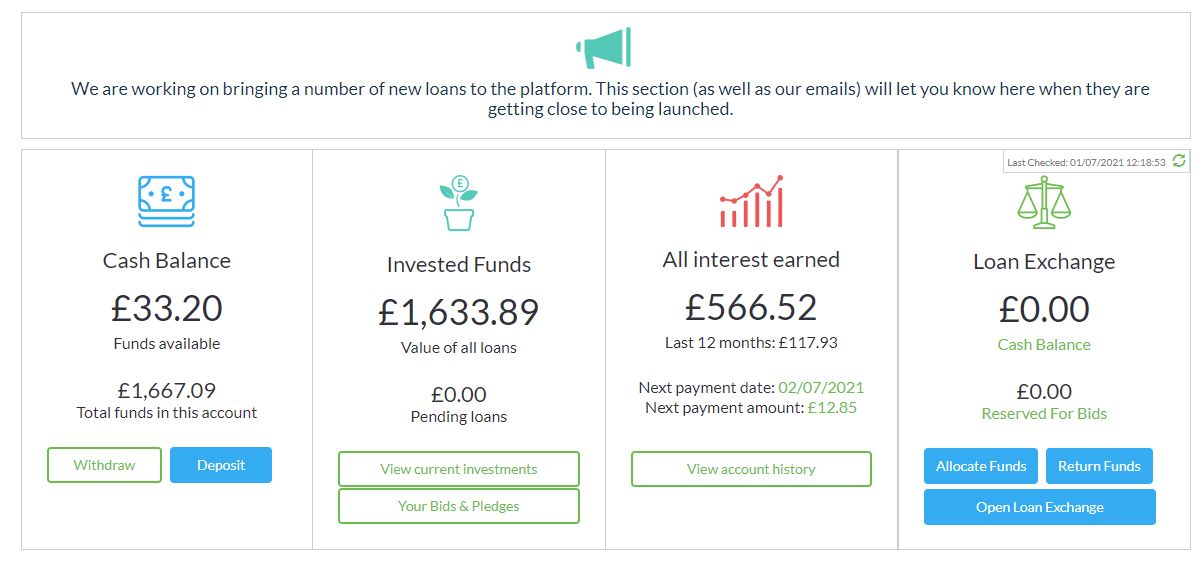

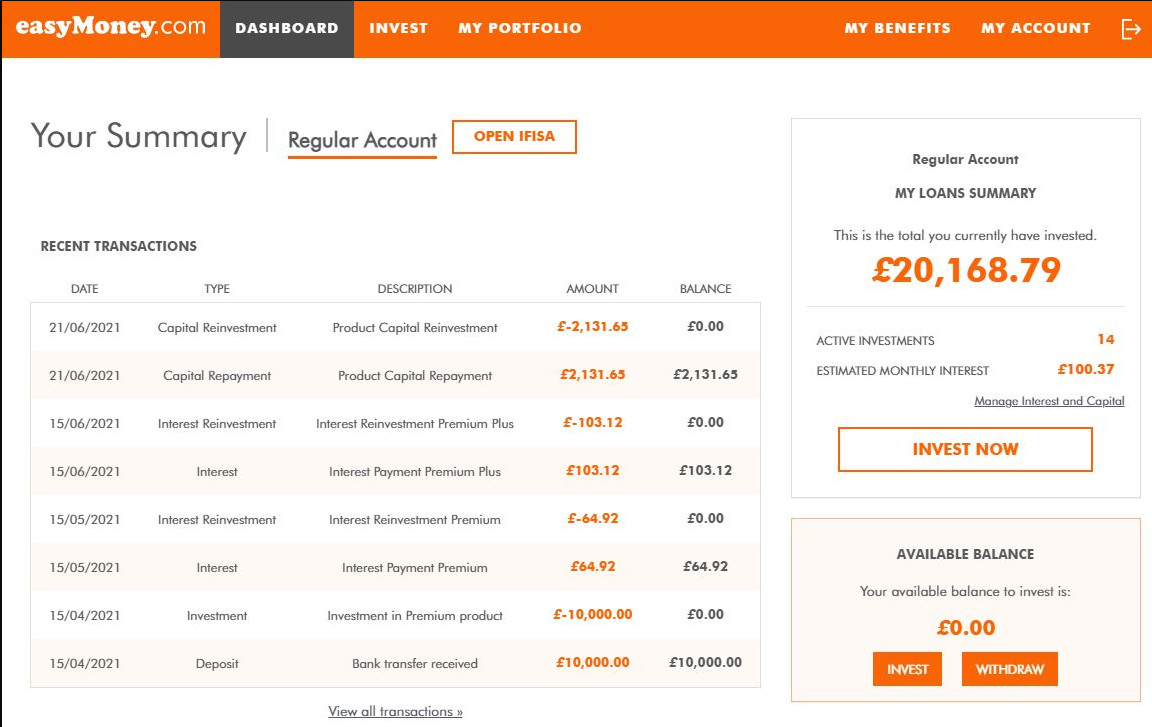

Right here’s my easyMoney account info for the tip of June, 2021.

Right here’s a screenshot of the easyMoney Dashboard

My easyMoney Technique

There’s no actual technique required for easyMoney. Simply deposit your capital and begin incomes curiosity. There’s actually nothing else to do.

easyMoney Cashback Presents & Signup Hyperlinks**

Click on right here to examine for brand new easyMoney cashback affords >>

Signup for easyMoney ISA Account >>

See Full Funding Circle Evaluation

Funding Circle gave me a little bit shock in June which contributed to the over all greatest month for P2P ever. They bought some defaulted loans to a different firm, so a number of the capital I had written off as misplaced over the previous few years got here again! Not lots however I’m not going to complain. All in all £673.77 returned so not a foul little shock.

I withdrew £1,063 from the bought loans plus month-to-month repayments. It’s not attainable to reinvest with Funding Circle anyway right now as they aren’t accepting funding from retail buyers.

Right here is how my Funding Circle account seems to be now. You’ll be aware that Funding Circle’s calculation of XIRR has gone up from 3.2% tp 4.2% (my very own calculation places it at 3.48%). Not an awesome danger/reward ratio in my estimation.

My Funding Circle Technique.

I’ve been drawing down my Funding Circle account since July 1st 2019 – attempting to promote out and get my capital again after occasions that unfolded in 2019. You possibly can learn extra about it within the Funding Circle Evaluation. There may be additionally no choice to put money into Funding Circle at the moment as they aren’t accepting funding from retail buyers.

I elevated my funding with Kuflink once more just a bit in June. I’ll nonetheless preserve filtering small quantities of capital there as I steadiness out my portfolio, however I’m attending to the purpose the place Kuflink is a big a part of my entire portfolio, so I have to preserve it actual to make sure diversification. I’ve completely zero worries about Kuflink. Positively top-of-the-line lenders on the market who do what they are saying. And top-of-the-line issues: you’ll be able to nonetheless get into their loans! Loans sometimes keep round for a number of days earlier than they’re absolutely funded (or a minimum of a number of hours).

Nice returns from Kuflink in June of £289.20 due to a number of loans being repaid. That’s the way it works with platforms like Kuflink and CrowdProperty. Revenue is just not one constant stage like it’s with Loanpad or easyMoney as earnings is barely acquired when the loans repay (except you select to obtain earnings month-to-month, which reduces the ROI), however over time an general XIRR return of 6.73% for Kuflink is among the greatest on the market contemplating the mortgage safety and their monitor file up to now.

They’re nonetheless bringing plenty of nice low LTV loans out, and paybacks all appear to be on time and on worth. The most effective all over the pandemic, no issues.

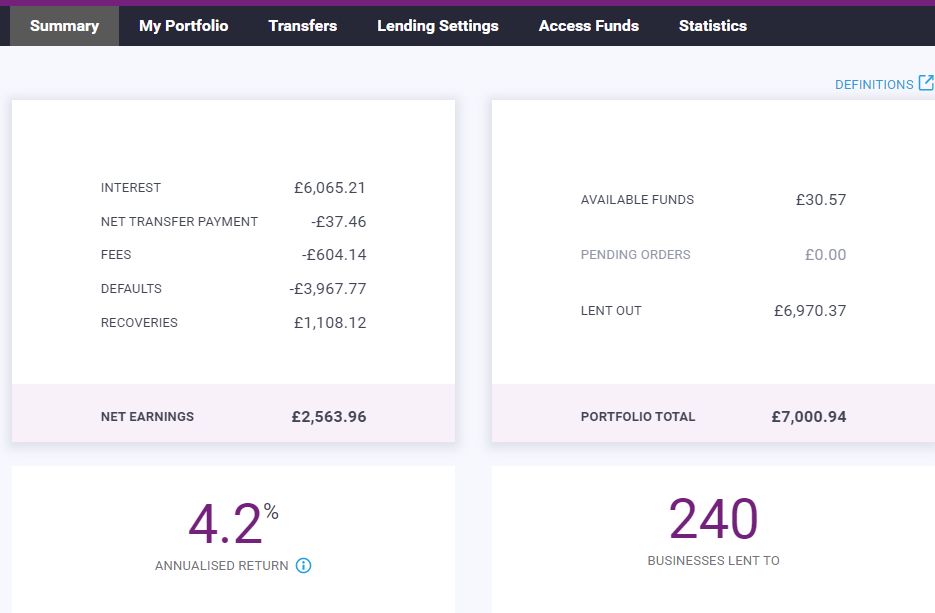

Right here’s my account because it stands on the finish of June 2021.

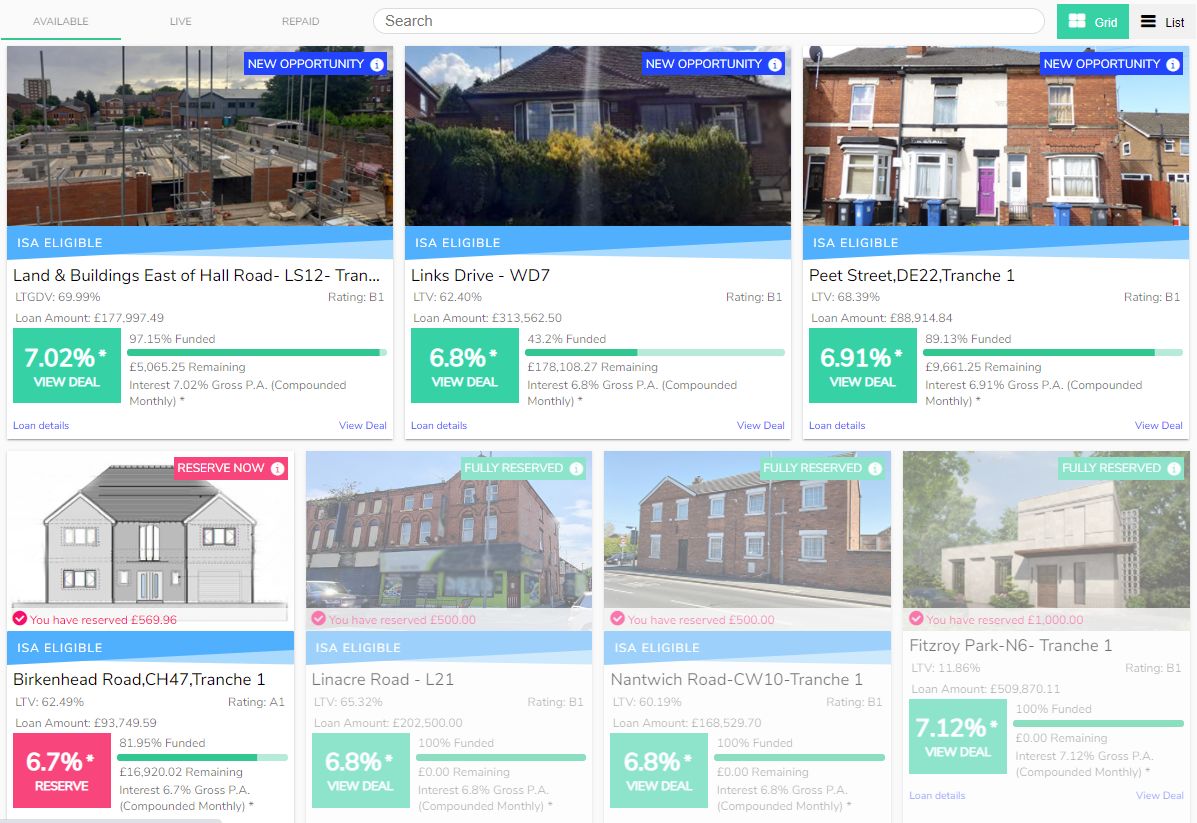

Right here’s a listing of all my present Kuflink loans. Nothing in default, only a couple awaiting standing updates (sometimes means they could be a few days late or the mortgage is about to repay).

You’ll be aware I’m in a number of tranches of some loans & I’m pleased with that. Typically I have a look at a mortgage and determine I would like more cash in it at the next fee (and a little bit extra danger after all) so I take positions in later tranches.

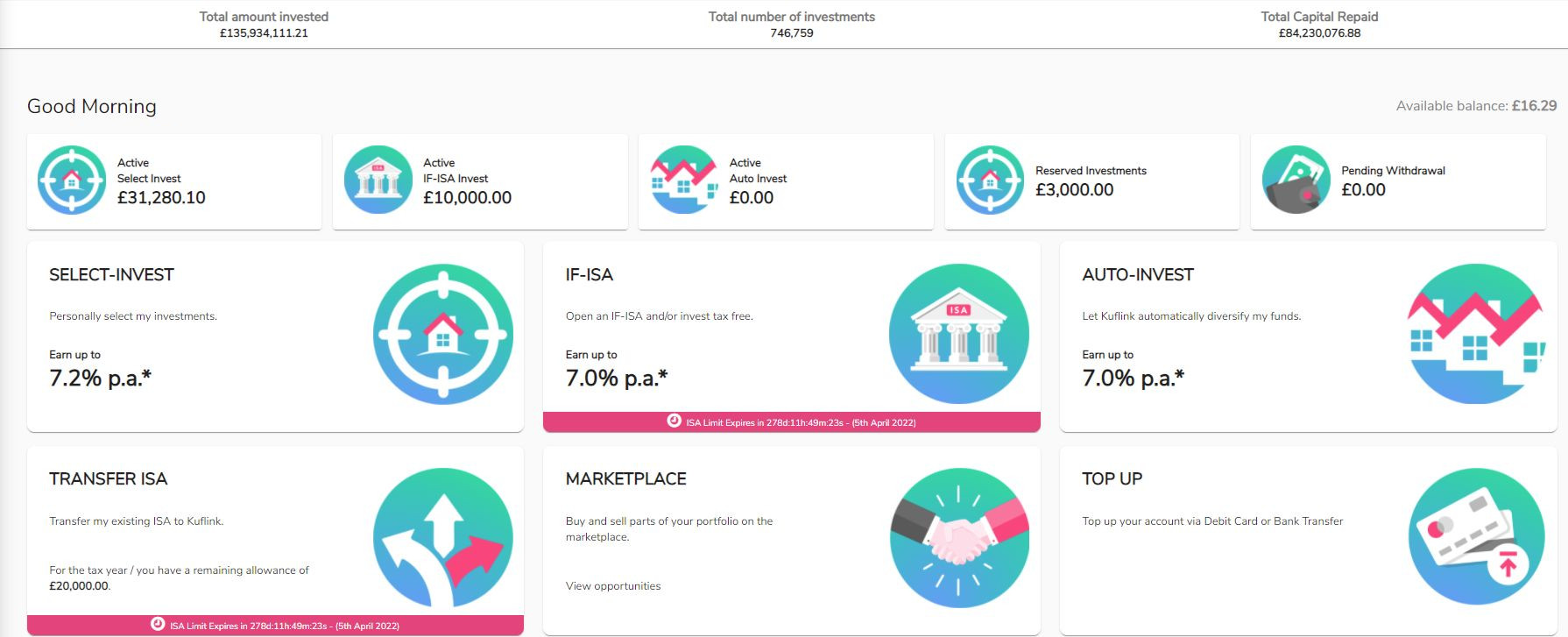

As one other be aware, Kuflink have now began permitting Choose Make investments offers to be invested into by ISA’s. Beforehand Kuflink ISA funding was solely accessible by Auto-invest.

Not all offers are ISA eligible, however you’ll be able to simply see those which can be:

My Kuflink Technique.

I proceed to take a position round £500 into virtually each mortgage Kuflink brings with an LTV over 50%. For loans with LTV’s below 50% & first authorized cost (& often tranche 1), I make investments £1000. As with CrowdProperty I do some due diligence and if I see one thing I don’t like, then I don’t make investments. That doesn’t occur usually although as Kuflink do nice due diligence themselves, so it’s just about £500 or £1000 into each mortgage.

Kuflink Signup & Cashback Presents

New Kuflink prospects obtain the next Kuflink cashback on an funding of £1000 or extra once they use signup hyperlinks from obviousinvestor.com. Should make investments into loans inside 14 days of first funding to qualify for cashback.

| Funding quantity | Cashback |

| £ 1,000.00 – £ 5,000.00 | 2.50% |

| £ 5,000.01 – £25,000.00 | 3.00% |

| £ 25,000.01 – £50,000.00 | 3.50% |

| £ 50,000.01 – £99,999.99 | 3.75% |

| £100,000.00 | 4.00%* |

*Cashback capped at £4,000.

Use this hyperlink to signup & qualify for the present Kuflink cashback supply >>>

See Full LendingCrowd Evaluation

No adjustments. Simply withdrew a little bit capital which was paid again.

Recap:

I made a decision to retrieve capital (the place attainable) from lenders who’ve unsecured loans to cut back my general publicity to Peer to Peer lending when the pandemic hit. Though LendingCrowd do have some secured loans, many simply have administrators private ensures. Traditionally, attempting to get better from simply these private ensures has been hit or miss. So, I made an early resolution to withdraw my capital.

I used to be capable of promote about 75% of the loans as I used to be early to begin promoting in March 2020.

Repayments have nonetheless been coming in slowly for the final 12 months and LendingCrowd are at the moment lending solely by the UK authorities backed CBILS scheme and as such aren’t accepting new capital from retail buyers. Hopefully when issues get again to some type of normality, LendingCrowd will open its doorways to retail buyers once more.

Here’s a screenshot of how my account seems to be at the moment

My LendingCrowd Technique.

As talked about beforehand; LendingCrowd are at the moment lending solely by the UK authorities backed CBILS scheme and as such aren’t accepting new capital from retail buyers.

As quickly as they begin accepting investments once more, I’ll decide on if & when to extend my funding once more with LendingCrowd.

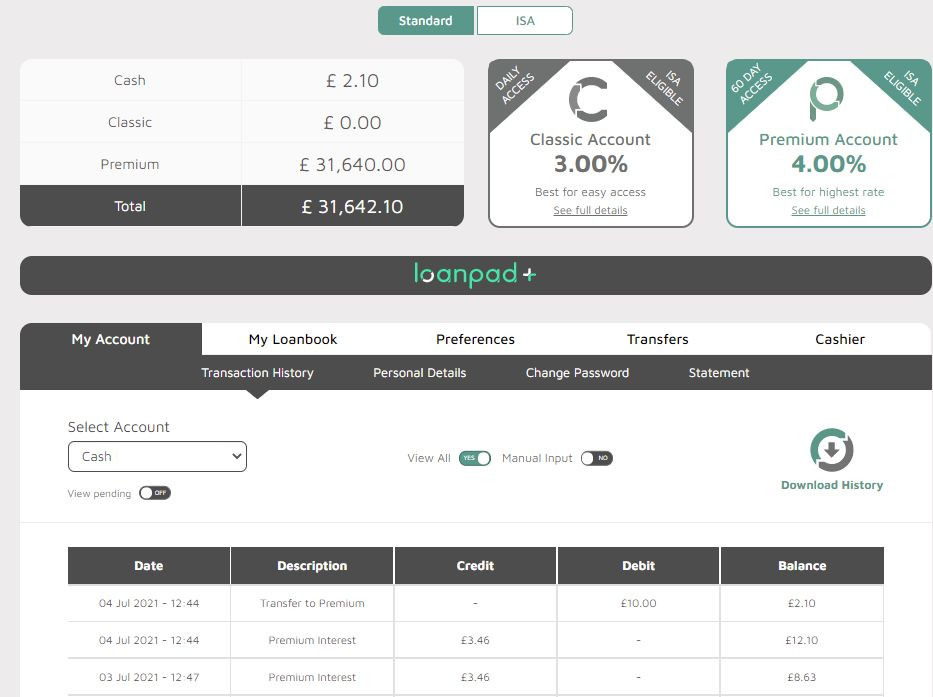

Loanpad is similar as standard, easy-peasy. Returns simply are available in on daily basis after which get routinely reinvested as soon as the money account reaches a worth of £10. Straightforward as pie. Secure as homes (actually) with the bottom LTV loans within the enterprise. Closest platform to a financial institution you’ll get (NOT a financial institution although by any means, no FSCS insurance coverage and also you capital is in danger).

There have been a number of gripes on a number of the P2P lending boards about LTV’s beginning to creep up with Loanpad. And it’s true, however they’re typically nonetheless below 50%. The issue is lots of their mortgage LTV’s have persistently been from 5% to 25%, and buyers have come to anticipate that. Nonetheless as Loanpad have develop into extra profitable and are rising at a really excessive fee, they will want to herald extra loans to satisfy the elevated capital necessities. Loans with 5% LTV’s aren’t the norm so they will creep up as mortgage circulation will increase.

So long as they keep below 50% (which is what Loanpad have all the time promised from the get go), and their due diligence stays good, I’m snug. Heck they’ve over £50k of my capital proper now so I’d higher be snug 🙂

Here’s a screenshot of how my accounts (normal & ISA) seemed on the finish of June 2021

My Loanpad Technique.

There’s probably not any technique needed with Loanpad. Simply deposit your funds, select your account & accomplished. Nothing extra you are able to do even in the event you wished, it’s all taken care of for you behind the scenes. After all 3% or 4% aren’t big returns so far as some P2P platforms go, however I imagine they’re in regards to the most secure lender on the market for the danger/return and that’s the rationale they’re my largest lending account by worth.

Loanpad Cashback Presents

£50 bonus in the event you make investments right into a lending account a minimal of £5,000 inside 4 weeks put up registration and preserve it invested for 1 12 months

£100 bonus in the event you make investments right into a lending account a minimal of £10,000 inside 4 weeks put up registration and preserve this invested for 1 12 months.

Use this hyperlink to go to the Loanpad web site & qualify for Loanpad cashback affords >>>

Unbolted seem like getting a number of extra loans in as my money steadiness as truly gone down in June. I’ll control them and can in all probability ship over some extra funding capital if it continues.

Unbolted are an awesome lender and I really like the truth that they aren’t actual property property loans. Simply one thing completely different to diversify into & they’ve an awesome monitor file.

In case you’re unfamiliar; Unbolted supply pawnshop model loans to most of the people with very liquid property. A lot of these property will be bought in a short time upon default so the demand for Unbolted loans exceeds the accessible loans.

I’ve been lending with Unbolted for a number of years now, and though there have been many defaults, property have all the time bought at greater than the excellent mortgage precept and I’ve all the time been paid again each precept and curiosity in a short time. Loans are brief to medium time period in nature so a whole exit will be had by turning off auto-invest inside 3 to 12 months.

Sadly the one drawback with Unbolted is getting capital invested as a result of they’ve so few loans now, and too many buyers with a whole lot of capital ready to get in. Though it seems to be like which may be altering, so I’ll be keeping track of them and including capital as wanted.

Right here’s a screenshot of my account because it stands on the finish of June, 2021.

Listed below are a number of the latest loans capital has been put into by auto-invest in Might. You’ll discover nonetheless solely small quantities being invested. Loans are being repaid, however the newer accessible loans can’t sustain. I did get £259.48 in to a regular mortgage, that’s as a result of they’re essentially the most dangerous so individuals don’t like to take a position a lot in them. I don’t thoughts as they nonetheless have good asset safety.

My Unbolted Technique.

I’d fortunately make investments extra capital with Unbolted if I may get it invested with out the money drag and good diversification. I actually love the platform and I’ve been lending with them for a very long time now.

I’ll control them and as quickly as capital begins to get invested faster, I’ll enhance funding in Unbolted by a major quantity. The query is; when will this occur after all.

Unbolted Signup & Cashback Presents

No present affords.

Use this hyperlink to signup with Unbolted >>>

EURO Lenders Replace

{kind=link}

I’ve been drawing down my Euro investments slowly as as a result of I dwell in Portugal a number of the time, after I’m right here I dwell on Euros. So I’ve been utilizing the Euros that I’ve invested in Euro Lenders for dwelling bills.

Sometimes I’d change US {Dollars} or GB Kilos for Euros, however the Euro has been rising quickly lately in opposition to the USD, and the GBP has nonetheless not recovered absolutely from Brexit. So I made a decision to make use of the Euros I’ve earlier than altering extra at this excessive fee within the hope it comes again down quickly.

If in case you have Euros to take a position and are in search of concepts. There are a number of Euro Lenders which have come by the pandemic and appear to have been largely unaffected, particularly Crowdestor, Swaper, Peerberry & Robocash have all accomplished what they’re alleged to do. I’ll put money into these all once more as soon as I’m prepared to take a position Euros once more. I imagine they’re all respectable investable corporations paying superb returns. Mintos can be price investing in so long as you understand you’re not investing in Mintos, you’re investing of their LO’s, and as such it is best to pay extra consideration to them than to the platform.

Securities, Bonds, Gold & Crypto Portfolios

USD Progress Portfolio

No adjustments from final month. All the pieces performing as anticipated. This portfolio by no means disappoints. That’s why most of my private wealth is invested in these property.

I’m truly unsure why I preserve this part within the month-to-month replace, this portfolio is so dependable it has been doing the identical factor for a few years. I suppose it’s helpful for once we get one thing completely different occur within the markets like when the COVID19 scenario occurred. Nonetheless didn’t change the general most drawdown of the portfolio although and it truly carried out very effectively by 2020.

Recap:

My fundamental Progress Portfolio is doing as anticipated. REITs took a tumble initially of the pandemic. Really all property received hit initially as panic set in, however REITs received hit the toughest shedding round 50% of their worth in a number of weeks. Loopy stuff! That’s what panic does for us.

As all the time occurs, the “secure haven” property (Bonds & Gold) picked up the slack and began to rally simply as they all the time do when the “large cash” (funds) begin to transfer capital into these property as a security hedge. The portfolio carried out admirably all through the pandemic after the preliminary “shock drawdown”.

When you have a look at the opposite portfolios based mostly on Harry Browne’s Permeant Portfolio, you’ll see that this Progress Portfolio beats them fingers down with simply the addition of the REITs. Though the entire Everlasting Portfolio property did as anticipated.

You might have observed that the returns numbers have elevated considerably for this portfolio. That’s as a result of earlier than I used to be utilizing inflation adjusted knowledge. I made a decision to cease that as the information is troublesome to correlate so now it simply the uncooked numbers. If it is advisable to understand how that appears traditionally in opposition to inflation, you’ll have to do some quantity crunching your self 🙂

Everlasting Portfolios (all currencies)

No adjustments from final month. All the pieces performing as anticipated.

Recap:

Portfolios based mostly on Harry Browne’s Everlasting Portfolio technique are all nonetheless doing effectively and as anticipated. All of them skilled some drawdown when the pandemic first hit, however nothing out of the odd. 7% – 12% drawdowns with these portfolios are an everyday prevalence.

None of them carry out in addition to the USD Progress Portfolio as a result of the portfolios that aren’t in USD forex aren’t based mostly on the US markets (traditionally a number of the worlds high performing markets), plus they don’t have the added publicity to REITs and the excessive dividends they carry. The one distinction between the USD Progress Portfolio & the USD Everlasting Portfolio are the REITs, so you’ll be able to see by that the distinction they make over time.

Crypto Foreign money Portfolio

I take advantage of Kraken & Binance for my Crypto Portfolio (shopping for/promoting/staking). And I take advantage of the Ledger Nano X & S for Crypto offline chilly storage.

Over the previous couple of months, ever since I made my first small funding in Cryptocurrency again in February 2021, I’ve been learning and studying about them.

I can say that I’m satisfied they will be a giant a part of the way forward for funding, and likewise finance usually. I understand that was a daring couple of statements, however that’s the place I’m at now. A lot in order that I’ve determined I’d wish to ultimately have round 5% of my general funding capital in varied crypto property after I can purchase them at (what I contemplate to be) cheap ranges.

Though my Cryptocurrency Portfolio is severely within the pink for June as I attempted to “purchase the dip” with many property, and the market proceeded to crash proper by that dip. I feel there’s a large alternative within the making. Plus most of my property are staked so I’m nonetheless making returns despite the fact that they’re within the pink.

When you’re excited about Crypto investing, I did a writeup on the Cryptocurrency Portfolio web page on my reasoning for buying lots of the property. The one factor that’s actually modified this month is that I’ve determined that if I’m going to take a position substantial capital into Cryptocurrencies, a few of that’s going to must be Bitcoin. All of my earlier ideas nonetheless stand in regards to the general potential for Bitcoin, however there isn’t a denying that Bitcoin nonetheless has (by far) the most important market cap, and due to this fact nonetheless leads the general Crypto market up or down. I’ll present you what I imply later.

So, with the above in thoughts, the query is: “when & how do I enter the market with important capital?”. I have already got an inexpensive funding in a number of of the altcoins (altcoin which means something that’s not Bitcoin) and there are a number of that I wish to purchase extra of, particularly Ethereum (ETH), Cardano (ADA), and Ripple (XRP). You possibly can learn within the Cryptocurrency Portfolio why I bought these property already. My motive for getting extra of simply these 3 is that this;

Ethereum (ETH) is the second largest crypto asset after Bitcoin, so it’s good diversification away from Bitcoin and it additionally has lots going for it as one thing aside from a purely “speculative funding”, which is all Bitcoin actually is.

Cardano (ADA) is a direct competitor to ETH, so with shopping for extra of this, I’m hedging my funding in opposition to ADA truly overtaking ETH sooner or later, which I feel is an outdoor risk. ADA could be very low cost proper now in comparison with ETH, so I can purchase a whole lot of it at decrease ranges.

Ripple (XRP) is a really completely different proposition. It was particularly developed for shifting currencies across the globe and it simply appears to make a whole lot of sense to me. It’s many occasions quicker than the Visa or Mastercard programs so far as transactions it could possibly course of in a second, and the truth that it was developed particularly for shifting property internationally makes it attention-grabbing as anybody who has needed to transfer massive quantities of capital throughout worldwide borders would possibly inform you, and what an arduous course of that may be.

PolkaDOT (DOT) is the opposite one which I like lots, however I’ve sufficient of that for now.

The entire different altcoins I’m invested in, I feel I’ve sufficient of for now. They have been (and nonetheless are) “punts”, and maybe certainly one of them will repay for that golden funding sooner or later, we’ll see.

The remainder of my Crypto capital (about half of the entire) will go into Bitcoin (BTC) as a long run funding. However ONLY on the proper value, which I feel could also be coming, and is certainly NOT $50 or $60k in my view.

Let me clarify what I’m pondering. Check out this chart of BTC & it’s 200 Week Transferring Common under because it began again in 2012.

One thing that occurred to me after I first noticed it was; not as soon as because it’s inception has it pulled again from the most recent ATH (all time excessive) greater than 60% and never returned to the 200 week shifting common earlier than setting off to make a brand new ATH. It pulled again in 2013 earlier than taking off to a ATH, however that was solely a couple of 30% pullback from the final low earlier than it took off and made a brand new ATH.

Bitcoin sometimes makes a brand new ATH then pulls again to the 200 week MA earlier than taking off once more. So, an excellent place to attempt to purchase it could be the following time it pulls again to that 200 week MA, wouldn’t you suppose?

Presently we’re at a .618 Fibonacci pullback (61.8%) because the final time BTC touched the 200 week MA which was again in March 2020. This “Fib quantity” a few of you’ll know is critical as as to if a pullback is certainly only a pullback, or if it’s a major downturn. So if we begin going up once more now from that stage (particularly set on the twenty second of June), we could possibly be probably new highs based mostly on Fib numbers, and BTC can be doing one thing it’s by no means accomplished earlier than, particularly making a brand new ATH with out touching the 200 week MA after a 60%+ pullback.

However, if we come down once more and exceed that quantity, I feel there could be an excellent likelihood we’ll meet the 200 week shifting common earlier than we head off up once more to the brand new ATH.

Now, keep in mind shifting averages are (by their nature) shifting! So on daily basis this common is just not hit, it strikes up a bit. However that line is the place I’ll probably purchase Bitcoin if/when it touches it once more, regardless of the value could also be at that time.

Because the 200 week MA strikes up, so will my purchase stage. The opposite factor to recollect is that the MA is a LONG means down from the place value at the moment is. For value to return down that far now (right now) it will have to retrace about one other 60% from the place it’s as I write this. That’s a giant transfer, however in crypto, it occurs, and it occurs usually. The Bitcoin value may additionally simply keep within the buying and selling vary it’s been at for a number of weeks, and the 200 MA would come as much as meet it will definitely.

Nothing is assured clearly, however all we now have to go on with investing is the previous, so we will solely hope it’s going to proceed to emulate it sooner or later. In spite of everything, markets are only a reflection of human greed and worry, and that hasn’t modified a lot because the starting of time.

Why am I solely discussing charts of Bitcoin? As a result of the entire market mainly follows Bitcoin. Not precisely, however Bitcoin by it’s self is a large a part of the entire Crypto market cap, so the opposite property mainly rotate round it, however on a complete comply with it. Plus it’s simpler to observe one main asset for a gauge to all the remaining.

Simply as a caveat, I’m nonetheless not saying Bitcoin would be the all time winner of the crypto race (in the event you’ve been studying my posts beforehand, you’ll know I don’t suppose that in any respect), however I’ve realized that we now have to respect its dimension in comparison with the entire crypto market at the moment. Out of all of the crypto property proper now, I feel it’s essentially the most secure (form of an oxymoron utilizing “crypto” and “secure” in the identical sentence I do know) however for giant quantities of funding, I want a few of it to be in Bitcoin.

This can be a chart of the entire Crypto Asset class vs. USD:

Right here’s a chart of Bitcoin/USD (these charts are from the free model of TradingView simply in case you’re questioning)

Clearly the patterns aren’t precisely the identical, however the ranges & proportion pullbacks general are very related.

You’ll additionally discover a number of different traces & ranges on the Bitcoin chart. The numbers are varied waves I’m monitoring (Elliott & Wolfe) after which the 200 week MA is the thick inexperienced line.

There are a whole lot of issues occurring round that inexperienced 200 week MA line. The 2019 excessive, and the fifth wave for a number of the counts (though it’s fairly a bit decrease for a few them) are all in that neighborhood all including to the chance of a flip ought to the BTC value pull again to that stage. After all there’s nothing saying that the 200 week MA will nonetheless be at these ranges if/when the worth will get there.

The Crypto market may take off again up and make one other ATH, it may do nothing because it has been doing for the previous couple of weeks, or it may come down some extra, or much more (personally I feel the latter, however nobody is aware of clearly).

Both means, I’m completely happy. If it heads off up, then I’m already out there with the property I purchased earlier within the 12 months, and if it comes all the way down to the 200 week MA, then I’ll purchase in. I’ll purchase Bitcoin and likewise the opposite property talked about earlier on the similar time.

After all then at that time, there’s the chance for it to crash by the 200 week MA, proceed decrease, and by no means make one other ATH, however that’s the danger we take with any funding.

Traditionally BTC has all the time retraced to, then turned again up at or round that 200 week MA. I are likely to imagine that Crypto will proceed this pullback, then resume its upward momentum to very excessive ranges sooner or later as governments preserve printing increasingly fiat cash, and likewise governments & banks tighten their management on capital actions for “cash laundering” (AKA tax harvesting) causes.

It could possibly be a major look forward to something to occur, however I’m in no hurry as most of my present property are Staked and making returns anyway.

So we’ll see what occurs 🙂

It goes with out saying, please don’t simply comply with investments that I make. And in the event you do determine to take a position, based mostly by yourself analysis, don’t put money into Crypto what you’ll be able to’t afford to lose, or a minimum of maintain on to for a very long time, as a result of it’s nonetheless the wild west of investing and really unstable as the previous couple of weeks have proven.

Abstract

That’s all for this replace. I’ll carry on monitoring all the pieces and we’ll see how I do with the varied investments.

If in case you have any feedback or solutions, please be at liberty to touch upon the put up, or e mail me instantly in the event you desire.

Good luck together with your investments within the coming months! Bear in mind, it’s about endurance & persistence, not perfection! When you begin investing in varied property if you end up younger, only a small quantity each month like I did, you’ll be amazed how shortly it turns into a major portfolio. You’ll even be amazed at how shortly you get previous 😀

My greatest to you and your households. Keep secure and I’ll put up an funding replace once more quickly.

Disclaimers:

This web page is offered for informational functions solely. I’m not a Monetary Adviser and due to this fact not certified to offer monetary recommendation. Please do your individual analysis and make your individual funding selections. Don’t make funding selections based mostly solely on the data offered on this web site.

* My opinions, critiques, star scores and danger scores are based mostly on my private investing expertise with the corporate being reviewed. These scores are private opinions and are subjective.

** A few of the hyperlinks on this web site are affiliate referral hyperlinks. Whenever you click on on these hyperlinks, I can generally obtain a fee, at completely no value to you. This helps me to proceed to supply new critiques & month-to-month portfolio updates right here on my web site. I don’t obtain commissions from all platforms and it has no impact on my ongoing opinions on investments & funding platforms. Revenue from my investments and capital preservation are my fundamental motivations.

Platforms reviewed on this web site I’m at the moment investing with, or I’ve invested with up to now. You possibly can see with full transparency on my Portfolio Returns web page which property & platforms I’m invested with (or have beforehand been invested with) at any cut-off date. I’m not paid a payment by any of the businesses to put in writing critiques, so the critiques are unbiased and purely based mostly alone private experiences.

Please learn my full web site Disclaimer earlier than making funding selections.