{kind=link}

The minds over at Yahoo Financing laid out to figure out a five-year home loan price anticipated making use of standard study and Anthropic’s Claude.

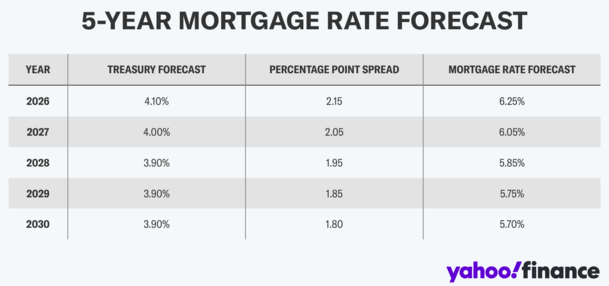

When integrating 10-year treasury return projections with forecasted spreads, they created 30-year set home loan prices for the following 5 years.

What they uncovered is that home loan prices are greatly anticipated to decrease, from around 6.25% this year to 5.70% by the year 2030.

Simply put, the price you see today could be the greatest price you’ll see for a very long time, disallowing the common, temporary ups and downs.

Which pleads the concern, if prices are mosting likely to be reduced, why opt for a 30-year dealt with?

Are We Extremely Dependent on the 30-Year Fixed Home Mortgage?

I seem like we’re also dependent on the 30-year set home loan.

Past that, many times it simply comes to be the default car loan alternative without more factor to consider.

It appears no one also discusses choices, be it the 5/1 ARM or the 7/6 ARM.

Those items are around, however frequently only represent a small piece of the general home loan market.

And frequently they simply most likely to well-off individuals that are much more smart and with the ability of dealing with any kind of disadvantage that could include an variable-rate mortgage.

Currently don’t obtain me incorrect. The 30-year dealt with is extraordinary. It’s distinctly American and among the very best devices a home owner contends their disposal.

However home loan prices aren’t for sale any longer. Securing an extremely reduced price isn’t an opportunity in 2026.

Those days are lengthy gone. Today, the 30-year dealt with is basically near its long-run standard.

It’s in fact a little listed below if we copulate back to the very early 1970s, as it balanced approximately 7.75% ever since.

Home Mortgage Fees Are No More for sale

The factor is it’s not a shouting bargain right now, so securing that price for the following three decades could not be so beneficial.

Specifically if these price projections from Yahoo Financing become right.

Basically, it made an universe of feeling to secure a price of 2-4% for the following three decades. However a 6 or 7% price? Ehh.

There could be a far better option – a variable-rate mortgage, such as a 5- or 7-year ARM that’s dealt with for the initial 60 or 84 months specifically.

That suggests it’s a crossbreed car loan, with a fixed-rate duration for rather a very long time prior to you need to bother with the price adjusting.

And also afterwards time, the price might not also readjust greater.

If we take these price quotes at stated value, prices are forecasted to relocate reduced in between currently and the year 2030.

That makes it much less beneficial to secure the price in for the following 3 years, considering that it’s not so unique.

ARMs Can Deal a Considerable Discount Rate If You Choose the Right Lending Institution

So if you secured claim a 5-year ARM today, it wouldn’t have its initial modification up until 2031.

If home loan prices were to drop at any kind of factor along the road, you can do a price and term re-finance and make the most of that.

This is likewise real if you select a 30-year dealt with. You can re-finance that right into one more fixed-rate car loan if you desired.

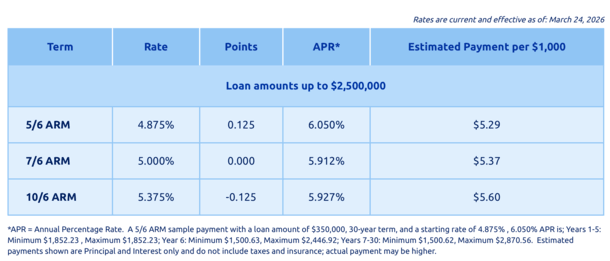

However with the ARM, you obtain a price cut. Which price cut can be substantial, maybe also 1% less than the 30-year dealt with.

This lending institution over has actually a 30-year dealt with at 6.375%, or a 7/6 ARM at 5%! Substantial distinction. And in the fours for a 5/6 ARM.

That’s the entire factor. If you secure the 30-year dealt with at 6.50% or whatever it occurs to be, you’re banking on prices going greater.

If they don’t, you don’t obtain any kind of benefit. You spend for the safety and security of that price not going greater, also if it never ever in fact does.

With the ARM, you obtain the price cut due to the fact that those guarantees aren’t baked right into the car loan.

To Make Sure That’s the disadvantage. That’s why most individuals don’t get ARMs.

Anything Is Feasible with Home Mortgage Prices

Anything is feasible with home loan prices. They can rise over the following 5 years, whereupon the ARM would certainly be a substantial obligation.

This occurred to those that chose ARMs back in 2017-2021, and stopped working to re-finance prior to prices fired greater.

However that was when prices were traditionally well below par (or at document lows). As kept in mind, they are currently basically according to lasting standards.

The various other concern is you could not have the ability to re-finance. Picture home worths plunge and you’re inverted on the car loan.

Certainly, that also would certainly violate background, as small home rate decreases are exceptionally uncommon.

There’s likewise the concern of getting approved for a home loan, thinking you shed your work, have negative credit rating, and so on.

So a home loan re-finance is never ever a bang dunk. Points can show up, and with the 30-year repaired you don’t need to bother with it.

However you do require to take a look at home loan prices a little in a different way today due to the fact that they’re back to regular.

Thus, looking past simply the 30-year dealt with is something we ought to all take into consideration.

Also if you can’t re-finance when the adjustable-rate duration ends, you could not require to. The fully-indexed price can be simply great.

And also all the financial savings throughout the initial 5 or 7 years.

Prior to developing this website, I functioned as an account exec for a wholesale home loan lending institution in Los Angeles. My hands-on experience in the very early 2000s influenced me to start discussing home mortgages 19 years ago to assist possible (and existing) home customers much better browse the home mortgage procedure. Follow me on X for warm takes.