{kind=link}

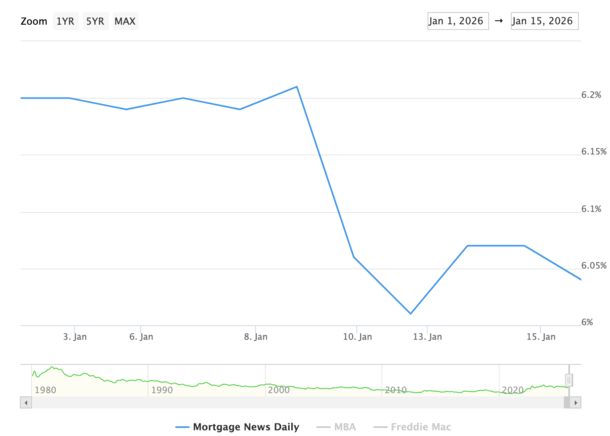

Finally glimpse, the 30-year repaired was back in the 6% variety, increasing from a short spell in the fives after information damaged that Fannie and Freddie would certainly acquire mortgage-backed safeties (MEGABYTESES).

Trump’s prepare for both to acquire $200 billion in MBS sent out home loan prices down last Friday to sub-6% degrees.

Yet the preliminary 5.99% analysis at Home loan Information Daily was temporary, and prices finished the day with a noontime reprice of 6.06%.

They opened up Monday at 6.01%, prior to jumping to 6.07% midweek, and after that dropping back to 6.04%.

So while they aren’t in the fives rather yet, at the very least when we think about the nationwide standard, they sure are close.

Home Mortgage Fees Battle to Appear to the 5% Array

While it looked like if we were ultimately right into the fives last Friday, it verified to be evasive as a reprice sent out prices back to 6.06%, per MND.

The preliminary response to the $200 billion MBS purchasing program was applauded by home loan lending institutions, lending police officers, and home loan brokers alike, however after that we saw a pullback.

The 30-year repaired dropped from 6.21% last Thursday to 5.99%, a huge one-day relocation of virtually 0.25%, prior to jumping and finishing the day a little bit greater.

It after that shut the complying with Monday at 6.01%, however once more, not rather the 5.99% analysis everybody so frantically desired.

Regardless Of this, the nationwide headings kept up the 5.99% analysis that remained in play briefly and didn’t recall.

Plainly it seems a great deal much better to state home loan prices remain in the fives than it does stating 6.01%.

I constantly believed it was intriguing that MND basically selected 5.99% as their price that day considering that there’s some degree of subjectively in the price index.

Had they stated 6.06% at first, the response would certainly have been even more low-key, regardless of the distinction in settlement being minimal.

Yet it does sort of indicate resistance at the 6% limit.

Lenders Always Cost Home Mortgage Fees Defensively!

This is a great suggestion that home loan lending institutions constantly rate defensively.

The very best method to show this is they fast to boost home loan prices if we obtain negative home loan price information.

On The Other Hand, if we obtain excellent home loan price information, they’ll take their wonderful time reducing prices.

Besides, they won’t wish to obtain surprised and be valued listed below market and shed their tails. Megabytes capitalists additionally require time to re-calibrate.

Nevertheless, they still did reduced their prices with numerous providing a 30-year repaired an .125% or a .25% listed below degrees the day prior.

So they didn’t rest on their hands, however offered the information was sort of out of no place, they most likely didn’t prolong the complete price cut either.

They require the dirt to resolve to see exactly how it’ll all function, the timeline, and perhaps simply the guarantee it’s in fact mosting likely to occur.

For the document, Fannie and Freddie were currently upping their acquisitions of megabytes prior to this information damaged, however with no excitement.

This is a much larger buy, presuming it takes place, so it was a lot more impactful.

Just How Much Reduced Can Home Mortgage Fees Obtain?

Currently the inquiry is if/when this program obtains underway, will mortgage prices go down much more?

Or is it mainly baked in currently offered prices are still floating near to 6%, which is much listed below the 6.21% we saw prior the statement?

One can make the affordable debate that regarding half the price cut is currently valued in, and an additional fifty percent can be coming.

So if the 30-year repaired by MND’s step went down regarding 15 basis factors, we can see an additional 15 bps in enhancement.

Provide or take a basis factor, maybe that obtains us to 5.875%. It’s not a huge settlement distinction, however it would certainly be a huge emotional win for the real estate market.

It’d be proclaimed as large information and certainly proclaimed by the White Home as a significant success for home customers.

Simply keep in mind that the megabytes acquiring is simply one element of home loan price rates.

We still need to take notice of what’s taking place in the broader economic situation, with rising cost of living and labor still significant elements that drive prices.

If that information isn’t positive, it can balance out the advantage of the MBS acquiring. Naturally, if the information is rate of interest rate-friendly, prices can be pressed even more right into the fives…

Keep Reading: 2026 Home Mortgage Price Forecasts

Prior to developing this website, I functioned as an account exec for a wholesale home loan loan provider in Los Angeles. My hands-on experience in the very early 2000s motivated me to start covering home mortgages 19 years ago to aid potential (and existing) home customers much better browse the home mortgage procedure. Follow me on X for warm takes.