{kind=link}

I wished to wait up until today to evaluate in on the brand-new prepare for Fannie Mae and Freddie Mac to buy MBS to see where the chips dropped.

And it appears like what I anticipated, a renovation of .125% to .25% in 30-year set home loan prices so far.

Trump revealed the other day on his Reality Social account that he advised Fannie and Freddie to get $200 billion well worth of megabytes.

The relocation is meant to reduced customer home loan prices, and soon afterwards article, FHFA supervisor Expense Pulte reacted on X, stating “On it.”

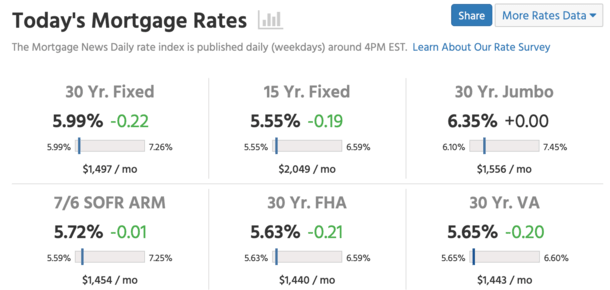

Today, we have a 5.99% home loan price, per the current read from Home mortgage Information Daily.

This will certainly rate information to practically everybody. The inquiry is will prices remain to relocate lower, or is it a one-time pick-me-up?

Trump Admin Obtains Its Sought-After 5% Home Mortgage Price Heading

I discovered it intriguing to see MND fix the 30-year set right under 6%, at 5.99% today.

That’s a huge emotional triumph for the Trump management, as something like 6.01% wouldn’t have virtually the exact same effect.

It implies they can state they decreased home loan prices to 5% once again after they rose to 8% under Biden.

National politics apart, it implies extra current home owners will certainly have the ability to reduced their home loan price through a price and term re-finance.

And extra possible home customers will certainly have the ability to receive a home loan many thanks to a reduced month-to-month settlement.

The beginning of 2026 was currently looking quite intense prior to this information, and currently it’s that little more vibrant.

I had actually forecasted a sub-6% home loan price by the initial quarter in my 2026 home loan price forecasts article, and it shows up to have actually come also previously than anticipated.

The following huge inquiry is just how the real estate market reacts. I’ve stated for a long time that home loan prices and home costs aren’t well associated.

Simply put, they can both drop with each other, climb with each other, or enter different instructions.

So don’t simply presume home costs are mosting likely to rise once again since home loan prices are dropping.

A 30-year set valued in the high or probably mid-5s is really a wonderful wonderful place where price is much better, however not suddenly a large deal.

This must enhance home customer need without it developing into a craze, while likewise pressing even more prospective vendors to provide their buildings.

Preferably, this causes a wonderful equilibrium of customers and vendors and even more supply to select from, without the bidding process battles and over-asking costs.

Large Financial Institutions Reduced Their Prices .125% Overnight

I’ve been speaking to home loan brokers and financing policemans today to see what occurred with prices over night.

As I thought, the enhancement has actually been around .125% much better, in spite of MND stating concerning .25%.

It will certainly depend upon the financial institution and loan provider concerned, however my resources stated rates improved by concerning .50%, which converts to approximately .125% reduced in price.

I likewise took a look at 3 significant financial institutions I’ve been tracking recently and they all enhanced by .125%.

This is what that appears like:

– Was 5.99%, currently 5.875%

– Was 5.625%, currently 5.50%

– Was 6.125%, currently 6.00%

So among the huge financial institutions is still estimating a 6%+ price, while the others that were currently sub-6% have actually relocated a little much deeper right into the 5% array.

Preferably, this can obtain us a grip in the fives so we don’t simply break back to the sixes once again, comparable to in 2015 when we maintained slipping back towards the sevens.

If there’s even more liquidity in reduced megabytes containers, loan providers will certainly have the ability to provide even more home loans in the fives moving on.

It is a favorable advancement for the real estate market, however it’s not a go back to 3% home loan prices.

This is not an additional round of QE, where the Federal Get acquired trillions in mortgage-backed protections and long-dated Treasuries.

It’s a relocate to soak up megabytes to boost rates and reduced home loan prices for customers through spread compression.

Simply put, the 10-year bond return can remain level and home loan prices can still boost many thanks to this order.

Notably however, the results will certainly be even more silenced without enhancement in bond returns.

Still Focus On Economic Information If You Desire Considerably Lower Home Mortgage Fees

If you intend to see a lot reduced home loan prices (that doesn’t?), you’re still mosting likely to require extra weak work records and even more reduced rising cost of living records.

Mentioning, we obtained the December work report today and it was sort of a variety, many thanks to task development disappointing assumptions (50k vs. 73k), however the joblessness price dipping to 4.4% from 4.5%.

That caused level bond returns today, however didn’t hinder of this brand-new megabytes acquiring information either.

If the labor market remains to deteriorate and rising cost of living remains to cool down, we might see the 10-year bond return loss also.

Paired with the MBS acquiring, you might picture home loan prices dropping closer to 5.5% and past.

The outcome would certainly be extra quotes in the high-4s presuming customers paid price cut factors at closing. Certainly that’d suffice to deal with the home loan price trouble.

However there’s no warranty that takes place, so watch on the information as it’s launched and be alert if you’re thinking about a price lock.

Problems can transform swiftly.

Prior to developing this website, I functioned as an account exec for a wholesale home loan loan provider in Los Angeles. My hands-on experience in the very early 2000s motivated me to start covering home loans 19 years ago to assist possible (and existing) home customers much better browse the mortgage procedure. Follow me on X for warm takes.