{kind=link}

Everybody is aware of excessive mortgage charges have been a complete drag these days, particularly for potential dwelling consumers going through extraordinarily excessive asking costs.

However what if I informed you that almost half of those that bought a house not too long ago nonetheless received an rate of interest under 5%?

Sounds fairly unlikely, given the truth that the 30-year fastened is again over 7%, and by no means went decrease than 6% during 2024.

Nonetheless, that didn’t cease 45% of “mortgage consumers” (non-cash consumers) from acquiring a sub-5% mortgage fee, per a brand new survey from Zillow.

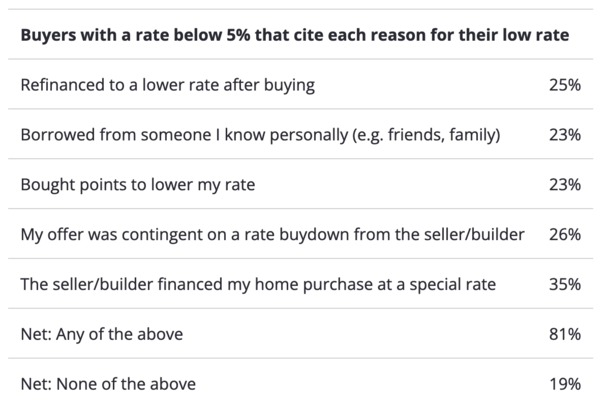

As for the way, the commonest motive cited was particular financing supplied by the vendor or dwelling builder.

Particular Mortgage Charges from House Builders

Some of the widespread methods to get a below-market mortgage fee has been by way of the house builders.

They typically function in-house mortgage firms to make sure their prospects make it to the end line.

And because of a financing instrument name “ahead commitments,” they’re in a position to supply tremendous low mortgage charges to the purchasers who use their captive lender.

These commitments contain shopping for low mortgage charges in bulk, forward of time, after which deploying the low charges to prospects who purchase properties in choose communities.

Whereas some solely supply momentary fee buydowns, these days many have supplied everlasting fee buydowns for the total 30-year mortgage time period.

This in all probability sounds fairly candy, however bear in mind you’ll want to purchase a newly-built dwelling to get your arms on a particular fee.

Some have argued that the low cost is constructed into the next gross sales value, so proceed with warning.

Additionally learn my piece on utilizing the house builder’s mortgage lender for extra on that.

For the document, particular person dwelling sellers can supply gross sales concessions that can be utilized to purchase down the mortgage fee too.

And along with builder buydowns, that was probably the most generally cited motive for a low fee at 35%.

One other 26% stated their supply was contingent on a fee buydown from the vendor/builder. So greater than half of the low charges got here from these preparations alone.

Shopping for Factors to Decrease Your Price

The third most typical motive a current dwelling purchaser was in a position to get a low mortgage fee was as a result of paying low cost factors (at 23%).

In case you have the obtainable funds, it’s at all times an possibility to purchase down your fee by paying some cash upfront.

This can be a type of pay as you go curiosity the place you pay at the moment for financial savings tomorrow. The important thing although is conserving the mortgage lengthy sufficient to expertise the financial savings.

The issue with that is if mortgage charges occur to go even decrease earlier than the breakeven level (when the factors grow to be worthwhile), it disincentivizes a fee and time period refinance.

Or should you occur to promote the property too quickly, similar factor. In distinction, momentary buydowns don’t lead to misplaced funds.

Should you promote/refinance quickly after a temp buydown, the leftover funds are usually utilized to the excellent mortgage stability.

Lengthy story brief, there’s danger when shopping for factors in that you just’ll go away cash on the desk.

The identical may very well be stated of momentary buydowns in that mortgage charges won’t be decrease when the speed reverts to the upper notice fee.

Quite a lot of people have purchased the home and dated the speed, assuming the mortgage charges would come down. To date they haven’t.

Obtained a Mortgage from a Buddy or Household Member

One other 23% of consumers stated they received a low fee as a result of they borrowed from a good friend or member of the family.

That is fairly stunning to me seeing that it’s such a big share of the inhabitants. I can’t think about that many dwelling consumers getting particular financing from mother and pa or another person.

However per Zillow’s research, that is what the numbers point out. For me, it’s fairly uncommon to make use of intrafamily financing, but it surely positively is a factor, particularly with charges a lot larger at the moment.

An instance could be your dad and mom providing to finance your property buy with a particular low fee from the Financial institution of Mother and Dad, maybe at a cool 3.99%!

Should you’re so fortunate, nice. However for many this sadly isn’t a actuality.

One other widespread motive people received a sub-5% mortgage fee was by refinancing after they purchased the house.

They will need to have nailed the timing (and paid factors) as a result of charges by no means formally went under 6% this 12 months.

Lastly, sub-5% mortgage charges have been related to adjustable-rate mortgages, homebuyer help, and shorter loans phrases, such because the 15-year fastened.

After all, if it’s not a 30-year fastened, sub-5% doesn’t have fairly the identical that means or worth.

Nonetheless, it’s spectacular to see that almost half of dwelling consumers received inventive and located a solution to overcome the mortgage fee hurdle.

Downside is there’s nonetheless the excessive dwelling value to deal with, and little method round that in the mean time.

The Zillow Shopper Housing Traits Report 2024 research concerned 18,500 profitable dwelling consumers and was fielded between March and September 2024.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) dwelling consumers higher navigate the house mortgage course of. Observe me on Twitter for decent takes.