{kind=link}

The data supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

Whereas there isn’t any arduous rule about what number of bank cards you need to have, the common variety of bank cards an American grownup has is sort of 4.

As you construct up your monetary understanding, you would possibly surprise: what number of bank cards ought to I’ve? Finally, the appropriate quantity for you’ll rely in your monetary state of affairs and wishes. Some people profit from having a single bank card, which presents straightforward administration and fewer choices. Then again, some folks can maximize bank card rewards by retaining monitor of many alternative playing cards—usually 5 or extra.

The variety of bank cards you will have can have an effect on your credit score rating each straight and not directly. Learn on to study extra about easy methods to discover the appropriate variety of playing cards for you, what number of playing cards folks sometimes have and the way having a number of playing cards can have an effect on your credit score.

Key takeaways:

- There isn’t a set variety of bank cards you need to have—it is determined by your particular person monetary state of affairs.

- People have a mean of three.84 bank card accounts.

- Having a number of bank cards is handy and might profit your credit score, although it may be difficult to maintain monitor of a couple of card.

What number of bank cards is just too many?

There isn’t a most variety of bank cards you need to have, because it’s not a one-size-fits-all reply, although some consultants say it might appear like a pink flag to lenders.

Bruce McClary, senior vice chairman on the Nationwide Basis for Credit score Counseling, warns that even when bank cards have low balances, it could scare lenders. Every bank card utility you fill out reveals up in your credit score report, and McClary says this may increasingly give the notion of a “compulsive borrower.” That is very true if the functions are crammed out inside a brief time frame.

Senior Trade Analyst at CreditCards.com Ted Rossman recommends making an attempt to house out your bank card functions. Extra particularly, solely apply for one or two inside a six-month interval and not more than 5 inside two years.

Take into account whether or not any of the next circumstances align with your individual:

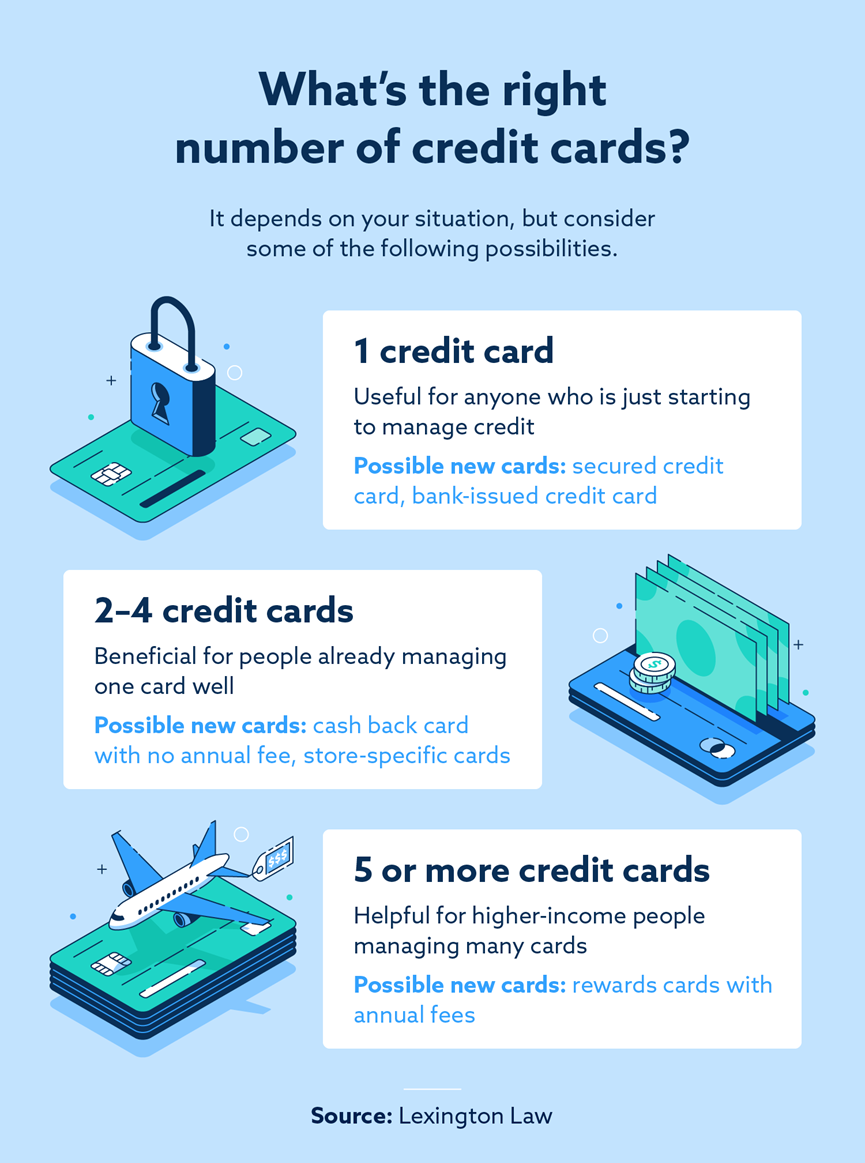

- You’re simply beginning out with bank cards. (Whole bank cards: one.) In the event you’re trying to get your first bank card, it’s normally smart to stay with a single account. Managing credit score may be troublesome, and including a number of accounts proper from the beginning can add to the problem. In the event you’ve by no means had a bank card earlier than, you possibly can think about getting a secured bank card, which has restrictions that show you how to construct credit score whereas studying the ropes.

- You’re trying to begin producing rewards along with your bank cards. (Whole bank cards: two to 4.) In the event you’ve constructed up your rating to the purpose that you may apply for rewards playing cards, that could be useful for you. Many individuals have a cashback card with no annual charge in addition to a retailer bank card with rewards for a retailer they store at usually.

- You’re managing vital quantities of credit score and have the next earnings. (Whole bank cards: 5 or extra.) Some people with excessive incomes and vital bank card spending can profit from rewards playing cards with annual charges. For instance, enterprise vacationers could get a journey rewards card that gives advantages like airport lounges or airline miles. Earlier than working towards one in all these playing cards, be sure that your spending habits and monetary state of affairs will justify the annual charge.

Once more, the variety of bank cards you select to have will rely significantly in your state of affairs, like how a lot you earn and spend, in addition to the way you’re managing credit score presently. Typically, you’ll wish to think about including extra bank cards to your identify solely you probably have a particular purpose for doing so. Having bank cards for their very own sake is normally not advisable, so think about rigorously earlier than opening a brand new account.

Is it good to have a number of bank cards?

Having a number of bank cards can profit your credit score by decreasing your credit score utilization charge, which accounts for 30 % of your FICO® credit score rating. Opening new accounts will increase your whole credit score restrict and reduces your credit score utilization—as long as you retain your balances down.

Whereas this issue is necessary, cost historical past accounts for a good bigger portion of your credit score rating (35 %), which implies making on-time funds on the cardboard(s) you do have is much more necessary than having a number of playing cards.

What number of bank cards do folks normally have?

Though everybody has totally different wants for credit score, the common variety of bank cards that American adults have is sort of 4, in response to Experian®, one of many three credit score bureaus.

In fact, the common variety of playing cards varies primarily based on a number of elements, together with location. For instance, in 2020, residents of New Jersey had the very best variety of bank cards on common in the US (4.54), whereas Alaskans had the fewest bank cards on common (3.06).

Much more fascinating is the generational hole amongst bank card holders. Members of older generations are inclined to have extra bank cards, however we additionally see older folks beginning to shut accounts as youthful folks open extra traces of credit score.

| Common variety of bank cards by technology | ||

|---|---|---|

| 2019 | 2020 | |

| Gen Z (18 to 23) | 1.76 | 1.91 |

| Millennials (24 to 39) | 3.18 | 3.18 |

| Gen X (40 to 55) | 4.35 | 4.23 |

| Child Boomers (56 to 74) | 4.81 | 4.61 |

| Silent Era | 4.00 | 3.64 |

What are the professionals and cons of getting a couple of bank card?

In the event you’re making an attempt to determine whether or not to stay with a single card or apply for a brand new line of credit score, it may be helpful to consider the benefits and downsides of getting a couple of bank card.

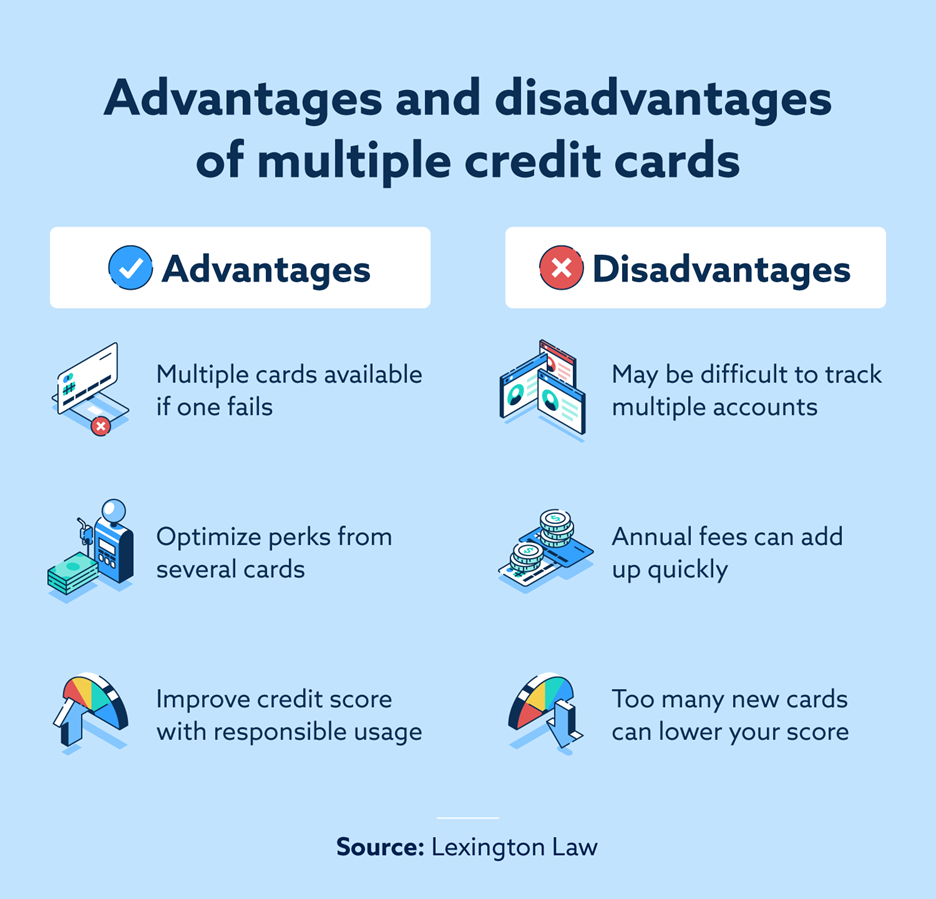

Among the advantages of getting a number of playing cards embody:

- If one card stops working, you will have one other card accessible.

- You may optimize rewards by utilizing perks from totally different playing cards.

- You might be able to enhance your credit score when you use all playing cards responsibly.

Then again, having a number of playing cards might have a number of disadvantages:

- Maintaining monitor of a number of accounts may be troublesome, particularly for making on-time funds and expecting fraudulent exercise.

- Annual charges from a number of playing cards can shortly add up, making rewards probably much less helpful.

- Getting too many new playing cards without delay might decrease your rating by dropping your common age of credit score and putting arduous inquiries in your credit score report.

Ideas for managing a number of bank cards

In the event you determine that having a number of playing cards is an effective alternative for you, observe the following tips for managing them successfully:

- Use your playing cards strategically to maximise rewards. For instance, you probably have one card that gives 5 % money again on fuel purchases and one other card that gives 1 % money again on all purchases, be certain you’re utilizing the one that gives 5 % if you hit the fuel station.

- Maintain monitor of phrases and circumstances. You probably have 4 bank cards, you’ll must be accustomed to the phrases and circumstances, credit score limits, rates of interest, due dates, rewards and extra for all 4 playing cards. Maintain a spreadsheet with all of this info so that you don’t lose monitor.

- Solely carry the playing cards you really use. You doubtless don’t must bodily carry each single card you will have. For example, when you use one card particularly for paying payments, it doesn’t must take up house in your pockets—preserve it at house for comfort and added safety.

- Pay on time and in full. That is the golden rule in terms of utilizing credit score responsibly. It might be useful to get your funds on the identical schedule so it’s simpler to recollect or arrange autopay so that you by no means miss a cost.

Whether or not you select to have a single bank card or many, you’ll wish to get within the behavior of checking your credit score rating in addition to your credit score report. Your credit score report reveals what every of the three credit score bureaus is aware of about your credit score historical past—accounts, balances and funds. In the event you discover any inaccurate info, like an account that doesn’t really belong to you, you’ll wish to file a dispute with the credit score bureaus to probably get that info eliminated.

In the event you’re working to handle adverse objects in your credit score report or when you’ve had some other difficulties managing credit score, study extra about how Lexington Legislation Agency’s providers might help.

Notice: Articles have solely been reviewed by the indicated legal professional, not written by them. The data supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for normal informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained throughout the web site don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.