{kind=link}

By Persis Yu and Abby Shafroth | December 22, 2021

Within the coming weeks, tens of tens of millions of American households will face a mix of monetary catastrophes: the brand new Omicron variant quickly upending our financial restoration, Congress yanking badly-needed Little one Tax Credit score (CTC) advantages away from working households, and the return after virtually two years of debilitating month-to-month pupil mortgage payments. These new hardships will arrive in opposition to a backdrop of record-setting will increase within the worth folks should pay for fundamental items.

New analysis by the Pupil Borrower Safety Middle and the Nationwide Client Legislation Middle reveals the devastating impact that this upcoming fiscal cliff could have on households in all 50 states. Specifically, our evaluation signifies that except the Biden administration adjustments course, pupil mortgage debtors at present receiving month-to-month CTC funds will quickly be compelled to make an common of $400 in month-to-month pupil mortgage funds concurrently they lose an common of $400 in direct monetary help from the federal authorities. General, we discover that with out rapid motion, tens of millions of People will see a adverse swing of their family funds averaging $800 monthly.[1]

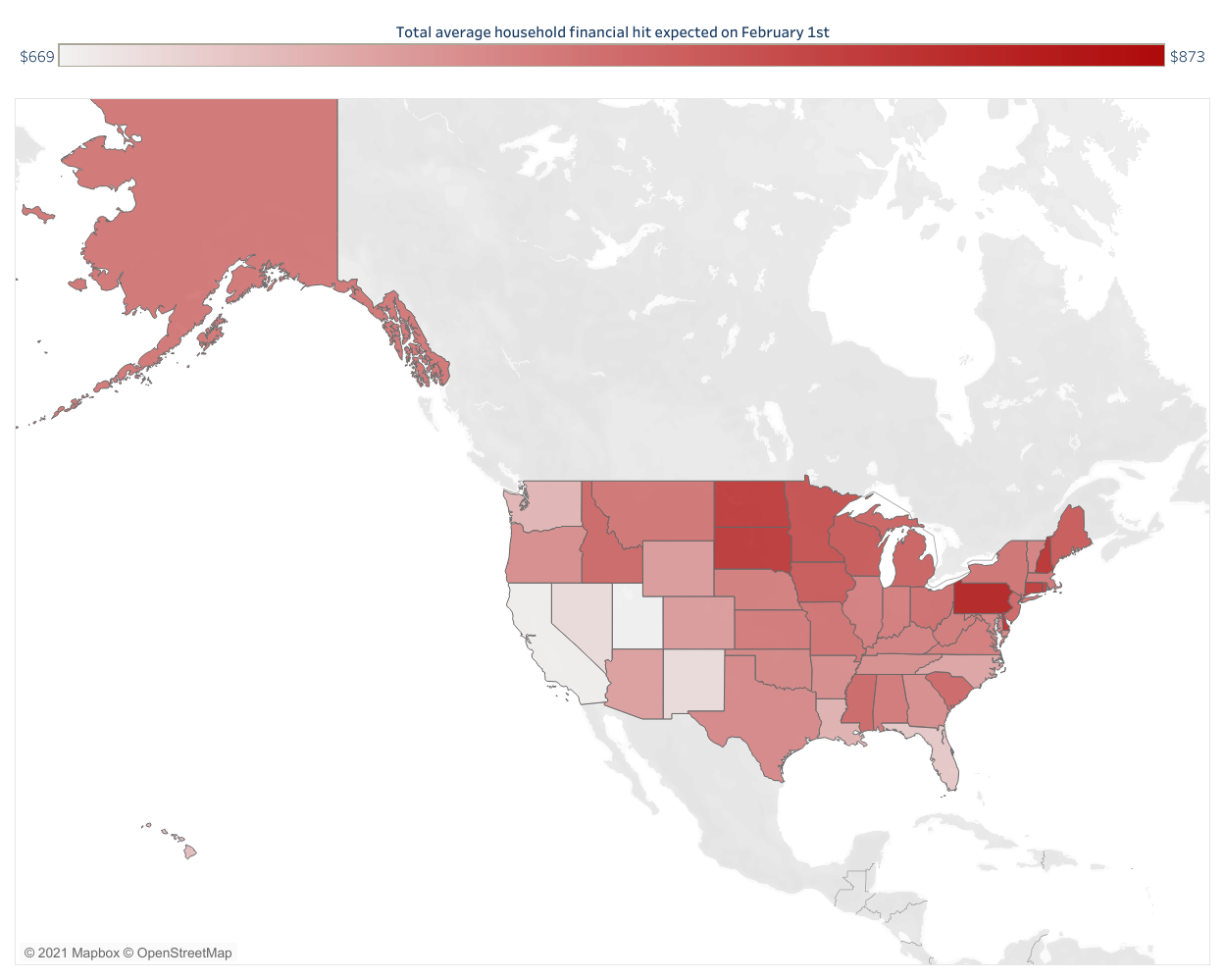

This upcoming monetary shock will attain debtors in each nook of the nation, from large cities to small cities and from the mountain West to rural communities within the East. The interactive map beneath exhibits the common budgetary swing working households will face on February 1st.

With out Motion by the Biden Administration, Hundreds of thousands of American Households Will Lose An Common of $800 a Month in 2022

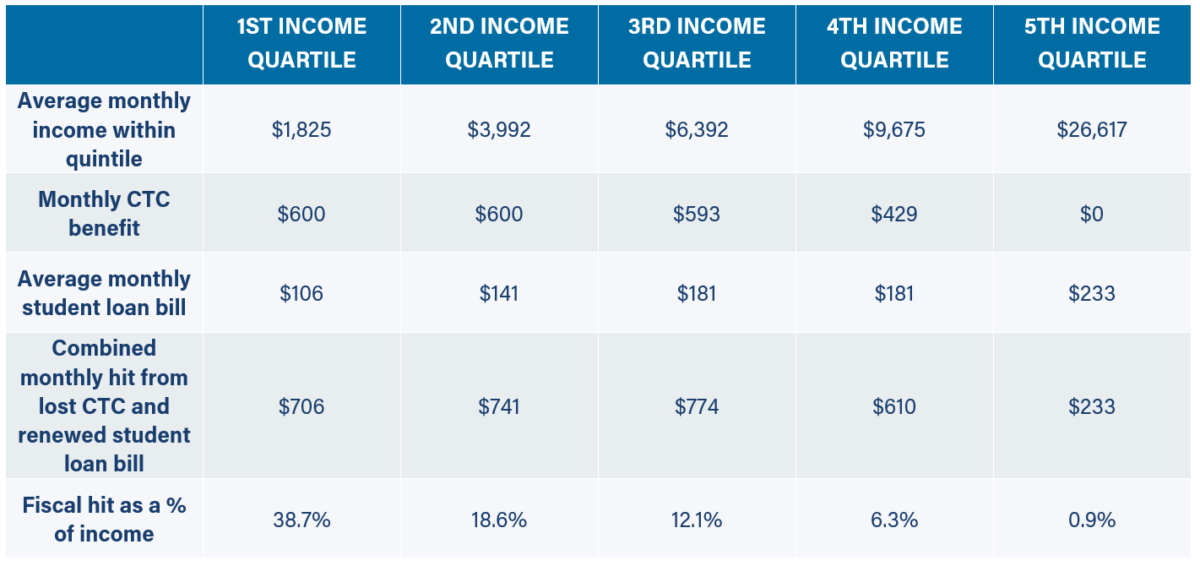

Worse, our evaluation exhibits that this upcoming monetary shock could have the biggest affect on low-income households. Utilizing public knowledge on earnings ranges, pupil mortgage balances, Little one Tax Credit score advantages, and extra, we in contrast how the mix of misplaced CTC advantages and resumed pupil mortgage funds will have an effect on People throughout the earnings distribution. We discovered that the upcoming monetary cliff will value the bottom earnings households an quantity equal to greater than 38 % of their earnings, whereas it’s going to value the best earnings households an quantity equal to lower than one % of their earnings.[2]

The Biden Administration Has to Act Earlier than It’s Too Late to Forestall Monetary Devastation

Our state-by-state evaluation comes on the identical day that Preventing Probability for Households launched a brand new ballot revealing that nearly half of debtors have no confidence of their potential to make pupil mortgage funds ought to the Biden administration restart funds in February 2022 as deliberate. This sentiment minimize throughout occasion strains, being voiced by pluralities of Democrats and Republicans and a majority of independents. On the identical time, fewer than 1-in-7 folks with pupil debt reported being “very assured” of their potential to make pupil mortgage funds once they come due.

The information is obvious: restarting pupil mortgage funds whereas permitting CTC funds to run out is a kick within the enamel to all working American households. Permitting these prices to coincide as deliberate will hurt tens of millions, significantly these already in probably the most tough monetary positions, because the omicron variant threatens our already fragile financial restoration. And that is earlier than even contemplating the large operational breakdowns that debtors are already grappling with as they put together to return to reimbursement.

COVID-19 is totally detached to debtors’ funds, to the need of help for working households, or the large burden that pupil mortgage debt locations on People. The Biden administration should select to not be detached.

###

Persis Yu was the Coverage Director and Managing Counsel on the Pupil Borrower Safety Middle. Persis is a nationally acknowledged skilled on pupil mortgage legislation and has over a decade of hands-on expertise representing pupil mortgage debtors.

Abby Shafroth is a employees legal professional on the Nationwide Client Legislation Middle and focuses on pupil mortgage and for-profit college points.

Have you ever misplaced your Earned Revenue Tax Credit or Little one Tax Credit due to federal loans in default? Please share your story with us right here.

[1] SBPC calculations based mostly on Pupil Mortgage Planner and the Division of the Treasury. Considers solely households with pupil loans that obtained month-to-month CTC advantages, and assumes for simplicity that their common pupil mortgage fee and CTC profit displays that of the general public as a complete. Provided that these debtors are possible lower-income, making it possible they might qualify for comparatively bigger CTC advantages and be extra reliant on pupil loans, the above estimates are possible conservative relative to the true monetary hit these debtors face.

[2] SBPC calculations based mostly on the Congressional Funds Workplace, the Washington Put up, Individuals’s Coverage Undertaking, and the Schooling Information Initiative. Assumes 10 years remaining in reimbursement on the restart level. Assumes 10 years remaining in reimbursement on the restart level. Assumes a single head of family with two kids underneath 6.

**The total weblog submit is out there at https://protectborrowers.org/if-payments-resume-and-child-tax-credit-benefits-expire-february-1st-will-mark-a-fiscal-cliff-for-millions-of-households-in-all-50-states/