{kind=link}

I’ve obtained fairly a number of emails asking why I haven’t been posting for the previous couple of months (10 months to be precise, eek!). The one actual reply I’ve is that I’ve had a number of different tasks happening, and in addition with the state of the overall markets proper now, we’re sort of in a “wait and see” part with many property, so quite than attempt to discover issues to waffle on about, I made a decision to focus my vitality elsewhere.

If you happen to have been paying consideration you’ll have observed that I’ve up to date my funding portfolio and charts/graphs on the finish of each month so you would all the time see most of what I’m doing, there was simply no commentary with it.

The reality is, P2P has sort of misplaced its luster with me now banks are paying higher charges. Additionally lots of the platforms I used to like have both gone, or look like on their method out. After I take a look at my total XIRR (return) by P2P (not together with any future potential losses) over the 9+ years I’ve been investing, it’s round 5.40%. Contemplating I simply opened a 2 12 months bond with Vanquis Financial institution at 6.20%, which is FSCS insured, and over the past 12 months I’ve additionally opened bonds at 5%, 5.5% and 6%, it simply seems to be the way in which ahead (for now at the least). P2P has served me nicely when banks have been paying just about nothing, nevertheless after I can get 6%+ with FSCS insurance coverage (so close to zero threat) with just about no problem, that’s what I’ve determined to do which a lot of my revenue based mostly capital whereas financial institution charges are nonetheless respectable. I’ll come again to P2P if financial institution charges begin to subside once more (I all the time look right here for the perfect financial institution charges in case you have been questioning).

Including to the above is the truth that a number of UK P2P platforms are shifting to institutional funding, are in hassle, or look like in hassle. I’ll provide you with a fast rundown of the place I’m sitting with my present platforms, what my emotions are about them, and the place I nonetheless have capital invested. These are simply my opinions and are subjective in fact. My notion may be improper so please do your individual analysis earlier than investing or pulling cash out of an account in a rush.

Peer to Peer Lending

Ablrate – what I mess this platform is. They determined to mainly wind the corporate down and naturally since then I’ve seen just about nothing in repayments. I presently have £3,500 caught in there that I’ll seemingly by no means see once more. I do maintain out hope that maybe I’ll see “some” of it again. There’s sort of a stir with this platform proper now because it seems the CEO has run off to Dubi and is having fun with himself on a seaside there if you happen to imagine what you learn. Simply rumour in fact 🙂

Assetz Capital – Closed to retail lenders – £560 caught in 2 loans by the outdated Property Secured Account and Nice British Enterprise Accounts that had a “discretionary” provision fund incase issues went dangerous. That fund didn’t get used sadly so we’ll see if I ever get that again. As it’s asset secured, hopefully I’ll get some half again sooner or later (hopefully I’m nonetheless alive, or at the least my heirs are). 🙂 Very dissatisfied with Assetz Capital total. Enterprise was very badly run however they did an excellent job of “spinning” it. In fact as soon as they went to institutional lending, mainly two fingers as much as the retail traders that had given them their hard-earned cash over a few years to that time. They’re charging traders all types of charges now to “handle” their investments whereas they wind down the person lender loans (that traders had no selection about paying). There are literally a few regulation fits filed in opposition to them for this I imagine.

Assetz Alternate – nonetheless a fairly secure funding I believe, nevertheless as a result of I can get comparable charges from banks now, I made a decision to begin to transfer out what I might. Sadly I nonetheless have about £16k caught in there that I can’t get out with out taking a loss in the mean time even when I might discover a purchaser, (as a result of property values go up and down with AE, and a few are extra invaluable than others relying on revenue and many others. which implies for some there are not any patrons in any respect). I don’t fear an excessive amount of about this platform because the properties are nonetheless paying month-to-month revenue at round 6%’ish, so both the property values will rise once more and I’ll promote out, or they are going to be offered by AE when the lease time period ends and hopefully at that time I ought to get many of the funding again. The opposite factor that worries me about AE is that the Assetz Capital CEO nonetheless has possession on this firm and after what they did to traders in fact who is aware of what might occur. Though AE say they’re a completely separate firm, the information nonetheless stay.

CrowdProperty – turned out to be a “lower than interesting” platform. I began attempting to tug cash out of there in April 2022. I had about 33k invested on the time and I began to “assume” I used to be smelling one thing dangerous (unsure what however I get intestine emotions about issues and I’ve realized “ignore them at my peril”). Roll on 15 months later and I’ve been in a position to get about half of the cash out however the remainder I’ve to say I’m involved about. Right here is my account as of July 2023.

As you possibly can see, not significantly encouraging with over 70% of the loans overdue (some greater than 2 years overdue imagine it or not). They’re secured by property however when the property goes into administration it will possibly take a number of time and authorized prices and many others. lots to get your a reimbursement. On the intense facet there are (savvy traders) individuals who nonetheless place confidence in CP (Ace, that one’s for you if you happen to’re studying this) so maybe I’m simply being paranoid? Time will inform. Have a look simply how late among the loans are within the screenshot under:

easyMoney – to be trustworthy, this can be a platform that I believed was “respectable” however over time they’ve turn into considered one of my favourite and moved from “respectable” to “nice”. I nonetheless have about £20k with easyMoney, a few of which I’ll seemingly transfer to banks, solely as a result of I can get mainly the identical fee from a financial institution with FSCS safety and I’m decreasing my total publicity to P2P. Each time I’ve determined to promote loans or transfer cash in or out of easyMoney, by no means an issue with liquidity. There was one little factor that I didn’t understand; while you need to promote loans, if any loans are inside 1 month of redemption, your cash is caught for that month as they received’t allow you to promote the mortgage. Not an enormous deal however it’s one thing to notice if you happen to assume you may get each penny out the identical day if you happen to want it. Aside from that, very respectable platform which I received’t hesitate to return again to if the chance/reward warrants it.

Funding Circle – I began exiting Funding Circle in Could 2019 after I observed a rise in defaulted loans. After I began exiting I had £31k in that account. After 4+ years lastly I’m right down to £480. The XIRR on that account ended up at 3.41% which I assume was higher than banks on the time. Each month I get a number of kilos from repayments.

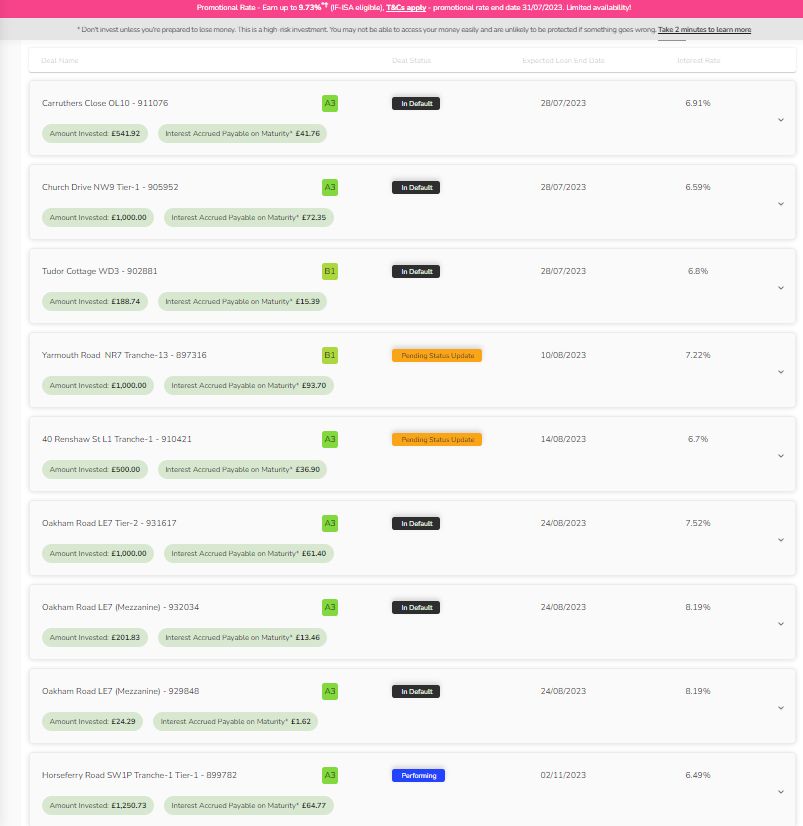

Kuflink – “was” considered one of my most favourite platforms for the final 5 years which I (solely very just lately) determined to scale back my publicity to. They’ve raised their charges just lately (8-9% pretty straightforward to get now) which is nice, they usually nonetheless have loads of new loans coming on-line. I’ve observed although that they began to have a number of defaults now (which I had actually by no means seen earlier than with Kuflink within the final 5 years). Here’s what the primary web page of loans in my account seem like now (there are 2 different pages with good performing loans after this to be honest, so take this as only a pattern of due and upcoming due loans):

On the identical time Kuflink just lately introduced bringing in a financial institution (Paragon) to begin funding loans, which is worrying for a lot of traders after what has occurred to different “well-known” platforms after bringing in institutional funding (though Paragon is providing Kuflink a line of credit score as I perceive it, not truly funding the loans as a Paragon funding). Add to this the minimal funding necessities (additionally just lately introduced which have precipitated a little bit of a stir within the P2P world) and it seems the writing “might be” on the wall for small traders (i.e. they don’t need them anymore, let’s hope I’m improper). Both method I’ve determined that 6.2% in a FSCS insured financial institution is extra comfy in the mean time than 8-9% with a platform making so many (seemingly damaging in the direction of particular person traders) modifications with publicity to the bridging and improvement mortgage market, which might get (/is maybe beginning to get with all of the defaults?) hit arduous if rates of interest maintain rising. It will solely take a few biggish losses to show that 8-9% into 5-6% or worse.

Kuflink additionally began to do a little bit of “spinning” on the way in which they promote their auto-invest rates of interest which irritated me a bit, subsequently reducing their credibility (like what else do we have to be careful for that they’re spinning?). You may see right here what I imply. Actually foolish enterprise resolution in my thoughts for a platform that had such a superb repute. Hi there Kuflink – did you ever hear the saying “if it ain’t damaged, don’t repair it”?

LendingCrowd – stopped permitting new funding throughout COVID however have paid again actually since. I nonetheless have simply £165 on this platform which I’ll most likely get again within the subsequent couple of years.

Loanpad – undoubtedly nonetheless the perfect and most secure platform on the market for my part. Their charges maintain rising however sadly banks are in entrance of them only a bit. I simply opened a 2 12 months 6.20% bond as you understand, Loanpads’ Premium Account is paying 5.80% (shifting to six% on August 1st, and 6.2% on the fifteenth). I’ll be leaving some cash with Loanpad as they pay “about” the identical as banks however I can get cash out with 60 days discover from the Premium Account or subsequent day from the Normal Account (underneath regular market circumstances). Their charges are rising each month, nevertheless for example, as I’m penning this replace, Loanpad’s Normal Account (subsequent day entry underneath “regular market circumstances”) is paying 4.80% (shifting to five% in August) and Chip (an prompt entry checking account I opened) is paying 4.51% and I can get entry to the funds instantly (inside minutes) that are FSCS insured in fact. What makes most sense for immediate entry to bigger quantities of capital proper now with all of the uncertainty on this planet?

Unbolted – final however not at all least is our outdated pal Unbolted who’ve simply raised their charges to 10.2% every year (0.85% monthly). I actually like Unbolted as they don’t cope with property as many of the different lenders do (though they do have a sister firm that does). They’re used to defaults (pawn store loans) and are completely consultants at coping with them, promoting the gadgets and recovering capital (not all the time protecting every little thing, however typically returning capital and a few curiosity). Over the entire time I’ve been investing in P2P Unbolted have constantly been the highest of the XIRR tree, often nicely over 8%. The issue in fact is that everybody in P2P is aware of this so it’s all the time a case of extra capital ready to be invested than loans. I simply regarded again and I presently have extra invested now at £15k than I’ve ever had with Unbolted in 6+ years. This isn’t as a result of I restrict it, it’s as a result of it’s tough to get massive quantities of capital invested with them. I’d love to have the ability to get 50 or 60k with them however it might most likely by no means occur with out huge money drag that would scale back the general charges significantly. I’ll seemingly begin to slowly run down the account a bit over time as I scale back my normal publicity to P2P, most likely leaving some in there simply because I really like them 🙂

Different Investments

Only a fast phrase about among the different investments and what I’m doing with them:

Crypto – this account is down over 50% so not an awesome funding to date. For now I’ll simply maintain maintain and let the staked tokens maintain constructing. Maybe at some point it is going to come again. For now I don’t want the cash I’ve left on this funding & I don’t like the concept of accepting a loss for no motive so I’ll simply go away it and see what occurs. Who is aware of, possibly it is going to storm again at some point? In the long run I believe Crypto (and particularly Bitcoin, sure I’ve modified my view on that) will turn into essential as our economies falter underneath the load of printing fiat forex and the mess most governments are making of our nations.

Shares/Bonds/Gold – the expansion portfolios are doing simply what they’ve all the time completed. At present making their method again up from a drawdown (which occurs each couple of years) however finally they’ll get again to the place they have been. In all probability as quickly as inflation begins to curb (which apparently is beginning already) and the central banks begin to loosen their maintain on rates of interest. I believe we’ll see bonds take off huge time at that time too and pull the portfolios up (TLT). The inventory market is nearly again to the place it was anyway if you happen to take a look at VTI. REIT’s are nonetheless a good distance from recovered although.

Discover UK Property – this palms off, buy-to-rent alternative turned out to be an awesome funding to date. They pay revenue often a few weeks earlier than due (they pay quarterly), and the worth of the property I bought has already gone up about 11% (plus the 6% revenue for the 12 months). I’m truly going to purchase a pair extra properties over the subsequent couple of years I believe. Simply ready to see if costs dip anymore earlier than I do (UK property costs already down 5% as I write this).

Whisky – I took revenue on a number of months in the past. It’s by no means improper to take revenue I used to be taught however on this case I left a bunch of cash on the desk. Oh nicely, can’t win em all 🙂

With that brief replace I’m going to say “till subsequent time”, each time that could be. No sense in posting updates with nothing to say. If/after I get different attention-grabbing investments or one thing occurs price speaking about, I’ll put up an replace and allow you to learn about it (assuming you keep subscribed to my checklist in fact). You may all the time e-mail me in case you have particular questions on something. Contact information is on the backside of the web page.

Take care and I want good well being and happiness to you and your households.

All the perfect,

Mark – The Apparent Investor

Disclaimers:

This web page is introduced for informational functions solely. I’m not a Monetary Adviser and subsequently not certified to offer monetary recommendation. Please do your individual analysis and make your individual funding choices. Don’t make funding choices based mostly solely on the knowledge introduced on this web site.

* My opinions, opinions, star rankings and threat rankings are based mostly on my private investing expertise with the corporate being reviewed. These rankings are private opinions and are subjective.

** Among the hyperlinks on this web site are affiliate referral hyperlinks. Whenever you click on on these hyperlinks, I can generally obtain a fee, at completely no value to you. This helps me to proceed to supply new opinions & month-to-month portfolio updates right here on my web site. I don’t obtain commissions from all platforms and it has no impact on my ongoing opinions on investments & funding platforms. Earnings from my investments and capital preservation are my important motivations.

Platforms reviewed on this web site I’m presently investing with, or I’ve invested with prior to now. You may see with full transparency on my Portfolio Returns web page which property & platforms I’m invested with (or have beforehand been invested with) at any cut-off date. I’m not paid a payment by any of the businesses to put in writing opinions, so the opinions are unbiased and purely based mostly alone private experiences.

Please learn my full web site Disclaimer earlier than making funding choices.