{kind=link}

The data offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra info.

It’s higher to go away a bank card with a zero steadiness open as a result of eradicating the account may negatively influence a number of credit score elements.

Nonetheless, canceling a bank card generally is a sensible monetary transfer in sure conditions. For instance, when you have a card with a excessive annual price and barely use it, canceling it is likely to be a good suggestion to keep away from pointless expenses.

For those who’ve efficiently paid down a bank card, chances are you’ll be questioning if it’s higher to shut it or go away it open with zero steadiness. Whereas it’s beneficial that you simply maintain unused bank cards open as a substitute of canceling, there are particular situations when canceling that bank card could also be in your greatest curiosity financially.

Let’s look at the professionals and cons of conserving and shutting your zero-balance

Is it higher to cancel zero-balance or maintain them?

The final rule of thumb is that it’s greatest to maintain your unused playing cards slightly than cancel them. Open bank cards, even ones you aren’t actively utilizing, assist you to construct up your credit score historical past and improve your obtainable credit score. That improve helps decrease your credit score utilization price, which is the share of obtainable credit score you may have used. These particulars are essential as a result of they relate to 2 elements that credit score bureaus depend on when figuring out your credit score rating.

For those who select to maintain a bank card open, attempt to use it often to stop the cardboard issuer from lowering your credit score restrict or closing your account as a consequence of inactivity.

On the flip facet, generally the information that you’ve got a bank card obtainable for purchases is simply too large of a temptation. For those who’re having bother controlling your bank card spending or in case your bank card has a excessive annual price, chances are you’ll be higher off canceling your card.

How does closing a bank card may influence your credit score?

Canceling a bank card, significantly an older one, can result in a credit score rating drop. The 2 major potential causes of this drop are:

- A rise in your credit score utilization price as a result of you may have much less obtainable credit score

- A lower within the common age of your credit score historical past

Let’s look extra intently at how these two elements can instantly influence your credit score rating. Understanding every one might help you identify whether or not or not you need to shut your zero-balance bank card account.

Your credit score utilization price may skyrocket

Even in case you aren’t making purchases on a bank card, that obtainable credit score helps to spice up your credit score utilization price, which accounts for 30 % of your credit score rating. The extra obtainable credit score you’re utilizing, the more severe off your credit score rating can be.

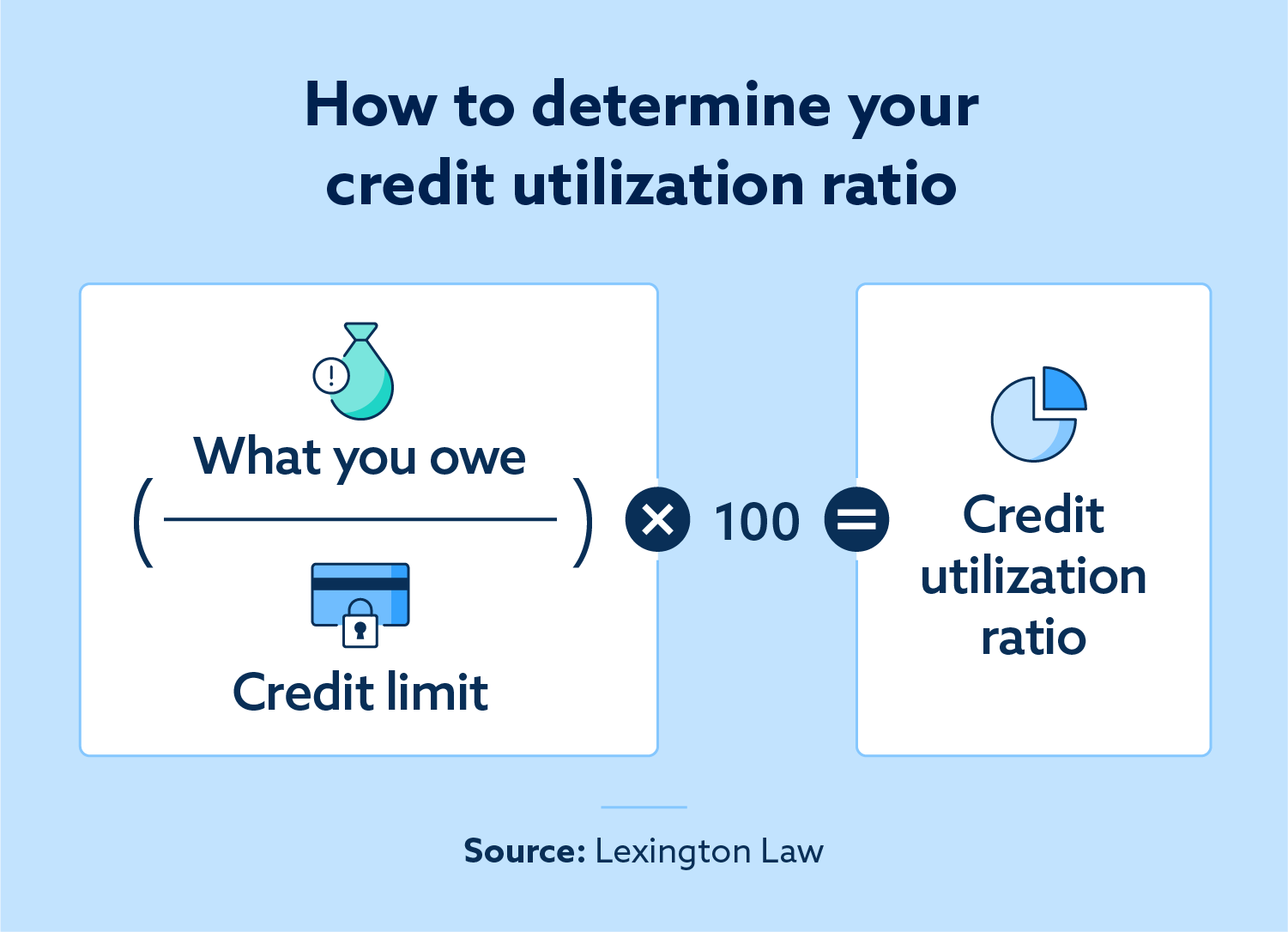

To know how your credit score utilization ratio — and thus your credit score rating — could possibly be affected by closing a bank card, right here’s a useful instance. Let’s say you may have two bank cards:

- One has a $3,000 restrict and a $3,000 steadiness (that is the cash you owe).

- The opposite has a $3,000 restrict and $0 steadiness.

- Your bank card utilization price between each playing cards is 50 % ($3,000 complete steadiness divided by $6,000 complete restrict multiplied by 100 = 50 % utilization).

- Nonetheless, in case you shut the bank card with the $0 steadiness, your credit score utilization price jumps to 100% ($3,000 complete steadiness divided by $3,000 complete restrict multiplied by 100 = 100% utilization).

In accordance with FICO®, the objective must be to maintain your utilization ratio under 30 %. There’s a straightforward system you should use to calculate your credit score utilization ratio:

- Step 1. Divide the full quantity of your general credit score debt by the full credit score restrict obtainable throughout all your bank cards.

- Step 2. Multiply the end result by 100 to supply your credit score utilization ratio.

Professional tip: Earlier than you shut a bank card, take a while to find out what your credit score utilization ratio could be. If that quantity will leap considerably, it might be a greater concept to maintain your zero-balance card open till you may pay down your complete bank card steadiness.

The size of your credit score historical past may lower

The longer you’ve had a bank card open, the higher. This helps to construct your credit score historical past, which accounts for 15 % of your credit score rating. You probably have a constructive historical past related along with your bank card paired with years of getting that card in your title, it’s a good suggestion to maintain that card open and in use, because it improves the size of your credit score historical past.

One simple strategy to maintain a bank card in use with out driving up your steadiness is to solely use it for recurring funds for issues like streaming companies or different subscriptions. That manner, you’ll know precisely how a lot is occurring that card every month and might simply repay the steadiness in full.

When must you shut your zero-balance bank card?

Relying in your monetary scenario, there will be compelling causes to cancel your unused bank card.

The cardboard has a excessive annual price

For those who’re charged a excessive annual price by your credit score issuer, canceling could also be a sensible cash transfer. Nonetheless, it’s value making an attempt to have the price waived earlier than you resolve to cancel, particularly in case you obtain rewards by the cardboard resembling journey credit and perks. Name your bank card issuer to ask for the annual price to be waived and point out that you simply’re contemplating closing your account. It by no means hurts to ask.

You’re a sufferer of fraud

In case your bank card is misplaced or stolen, the issuer will often shut the account and ship you a substitute. However, if a enterprise continues to permit unauthorized expenses even after you report the problem, closing the cardboard is likely to be the very best monetary transfer to guard your self from additional fraud.

You’re going by a divorce

For those who’re separated or getting a divorce, it’s a good suggestion to shut any accounts you share along with your ex, as you might find yourself saddled with a bank card steadiness they’ve accrued on the account.

You’re out of debt

Everyone seems to be completely different, and for some, the temptation to maintain a bank card and never use it’s too excessive. For these struggling to get out of debt or for individuals who just lately climbed out of bank card debt, it is likely to be a good suggestion to cancel your unused bank card and stick with utilizing money or your debit playing cards to keep away from sinking again into revolving bank card debt.

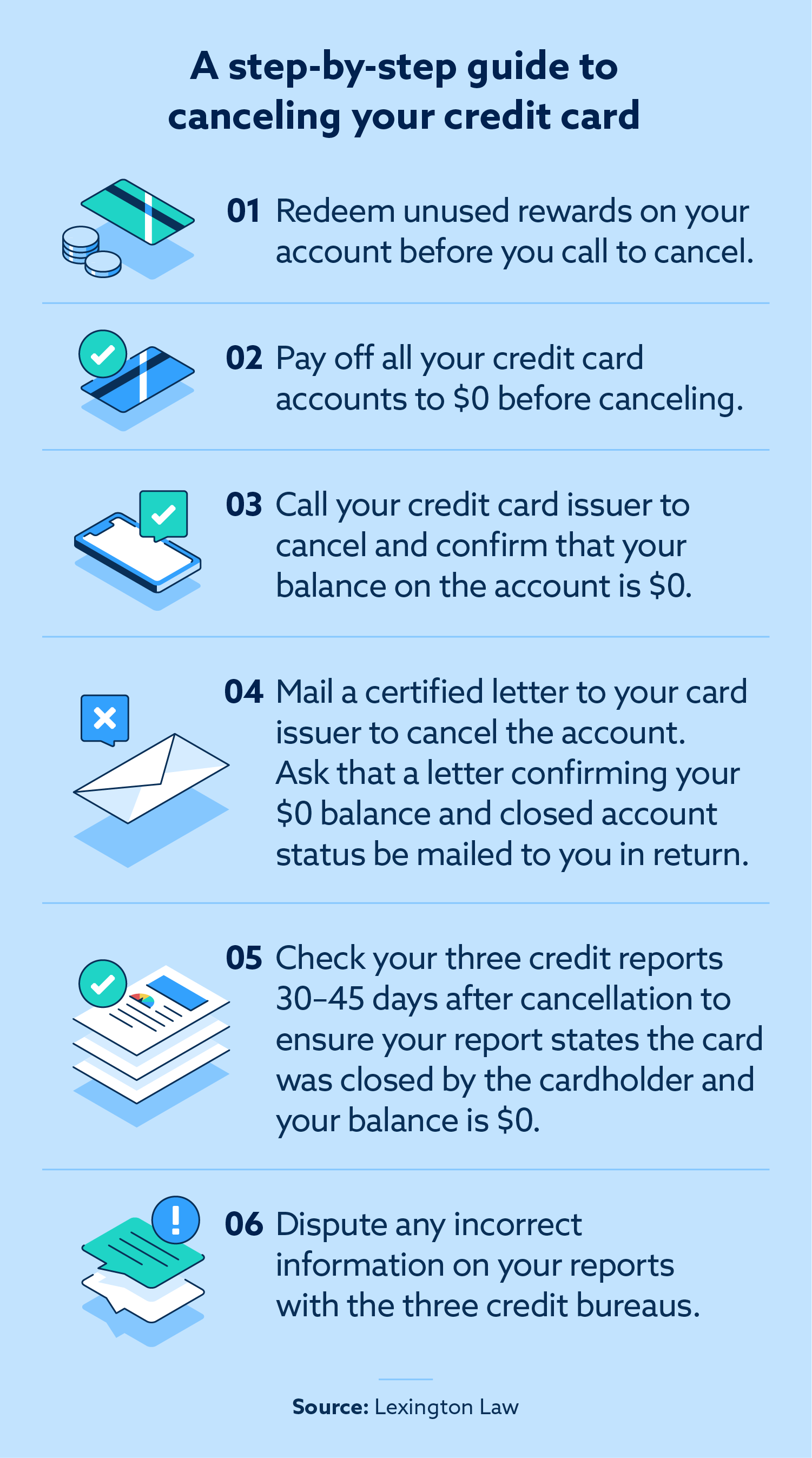

Tips on how to cancel your bank card in 6 steps

For those who do resolve to shut your bank card, there are a number of steps you need to take to make sure you’ve correctly closed your account.

- Redeem rewards factors: Discuss with your bank card’s redemption guidelines to discover ways to redeem your factors previous to closing your account.

- Repay your steadiness to zero (if it isn’t already): Repay any remaining steadiness in your card earlier than making an attempt to cancel it.

- Affirm your zero steadiness: Contact your bank card issuer on-line or by way of telephone to guarantee that your steadiness is zero.

- Make it official with licensed mail: Ship a licensed letter to the corporate that issued your card requesting they ship you a written letter verifying the zero steadiness and the closed standing of your account. Maintaining a paper path is an effective way to keep up a document of when the account was closed in case it’s essential to contest any info in your credit score report down the road.

- Monitor your credit score studies: Examine your credit score report 30-45 days after your card is closed to ensure the cardboard is formally reported as “closed.”

- Dispute any errors: When you’ve reviewed your up to date credit score report, be sure you dispute any incorrect info chances are you’ll discover.

Backside line: It is dependent upon your monetary scenario

Deciding if it’s higher to shut a zero-balance bank card or go away it open is a private determination — the reply will rely in your distinctive monetary circumstances. Regardless of your scenario, it’s essential to cancel any unused playing cards in a manner that retains your monetary well being intact and minimally impacts your credit score rating.

For some, having unused bank cards could also be no temptation in any respect, however for others, the information of getting a card obtainable to make use of could possibly be tough to disregard. Canceling a bank card received’t essentially change your spending habits in the long term, so it’s essential to develop a wholesome strategy to your private funds by creating a sensible finances and sticking to it.

Tame your bank card debt with Lexington Regulation Agency

When you may have a bank card with a zero steadiness, the choice whether or not to maintain it open or not is dependent upon your credit score rating objectives. If inaccurate info in your credit score studies is dragging your rating down, credit score restore companies might help you problem these errors and doubtlessly increase your rating.

Be aware: Articles have solely been reviewed by the indicated legal professional, not written by them. The data offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained inside the web site don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.