{kind=link}

Are you anticipating purchasing your desire home in the UAE however unsure exactly how to finish the residential or commercial property acquisition with a Home mortgage as an employed individual? You are not the only one, and you remain in the ideal location.

Allow’s recognize the procedure detailed according to UAE Banks criterion.

📘 Allow’s Understand Mortgages for Employed people

What is a Home mortgage?

A home mortgage or a home mortgage is a loaning you extract from the financial institution to get a residential or commercial property, whether for your very own use or for a financial investment. In return, you pay the financial institution month-to-month installations (EMI’s) which is a mix of principal and rate of interest.

It’s like a lasting residential or commercial property rental arrangement, where you pay lease for the arrangement duration and the only distinction is that you will certainly come to be the complete proprietor of the residential or commercial property at the end of the arrangement duration.

Just How Home Mortgage Functions in the UAE

In the UAE, financial institutions provide home loans to employed individuals based upon their month-to-month revenue, task security, credit report account, and race. The financial institution pays the residential or commercial property vendor, and you pay the financial institution in EMIs (month-to-month installations) over 15 to 25 years.

Advantages of Taking a Home Mortgage as a Salaried Customer

-

You don’t require to pay 100% of the residential or commercial property worth

-

Rates of interest are fairly reduced

-

You develop equity gradually

-

Numerous financial institutions provide unique advantages for employed specialists

📝 That Can Use? Qualification Requirements in UAE

Minimum Wage Needs

A lot of UAE financial institutions need a month-to-month wage of AED 8,000 to AED 15,000. The greater your revenue, the far better the home loan bargain.

Work Period & Company Kind

You ought to be utilized for at the very least 6 months to 1 year. Some financial institutions might likewise need your business to be noted with them, however at Compare4Benefit, we aid also if your business is not noted.

Visa and Residency Problems

You require to hold a legitimate UAE home visa. If you’re on probation or simply relocated tasks, you could require to wait up until your probation mores than.

Age & Credit Report Needs

You need to be 21 years or older, and generally not older than 65 at the end of the car loan. A credit history over 650 is liked, though some financial institutions approve reduced with problems.

📂 Called For Papers List

Don’t fret—we’ll aid you arrange all these:

-

Key & visa duplicate

-

Emirates ID

-

Salary certification

-

Financial institution declarations (6 months)

-

Most current payslips (If variation in wage)

-

Residential property papers (MOU, Title Action) – If Chosen

-

Existing loan/card responsibilities

💸 Deposit and Loan-to-Value (LTV) Guidelines

Deposit for Deportees vs UAE Nationals

-

Deportees: Need to pay 20% deposit for homes under AED 5M, and 30% if it’s above.

-

UAE Nationals: Simply 15% deposit for homes under AED 5M.

Optimum Car Loan Qualification

Based upon your wage and DBR, you can obtain a car loan for as much as 80% of the residential or commercial property worth.

📉 The Function of DBR (Financial Obligation Strained Proportion)

What is DBR?

DBR = Your month-to-month loan/credit settlements ÷ your revenue. If it’s greater than 50%, your home loan might be decreased.

Just How to Compute It

Accumulate your charge card fees, auto loan EMI, individual car loan EMI, and the predicted home loan EMI—after that divide by your wage. You can compute your DBR currently on DBR Calculator UAE

Why DBR Issues for Authorization

Financial institutions are stringent regarding DBR. Maintaining it listed below 50% increases your authorization opportunities and permits greater car loan qualification.

🏦 Contrast Home Mortgage Deals in the UAE

Right here’s a fast contrast:

| FINANCIAL INSTITUTION | INTEREST RATE (Beginning With) |

MINIMUM INCOME | FINANCE QUANTITY (MAX) |

|---|---|---|---|

| Conventional Chartered Home Mortgage One | 4.39% (minimizing) | 15000 AED | 18 Million AED |

| RAKBANK Home in One | 4.39% (minimizing) | 15000 AED | 20 Million AED |

| CBD Home Loan for Deportees | 3.99% (minimizing) | 15000 AED (Employed individuals); 20000 AED (Independent) |

10 Million AED |

| Emirates NBD Home Mortgage for Deportees | 3.99% (minimizing) | 15000 AED | 15 Million AED |

| Conventional Chartered Home Collection | 4.29% (minimizing) | 15000 AED | 18 Million AED |

| ADIB Home Financing for Deportees | 3.99% | 15000 AED | 15 Million AED |

Compare4Benefit reveals prices from 25+ financial institutions—you choose the very best!

📊 Apartment Rates Of Interest vs Decreasing Rates Of Interest

Financial institutions in UAE fees rate of interest based upon minimizing rate of interest just, minimizing price is fees on the superior quantity.

Apartment Rates of interest is just the typical interest rate billed on the real car loan quantity.

For instance: Decreasing rate of interest of 3.49% yearly amounts 2% Apartment price if period is 25 years.

You can refer Level price Vs Decreasing price calculator for far better understanding

🔁 Changing to a Much Better Home Mortgage (Acquistion Alternative)

Currently have a home mortgage? You may be paying too much.

What is a Home mortgage Acquistion?

It’s changing your home loan to one more financial institution for far better terms.

Advantages of Moving

We manage the complete button for you—no documentation tension.

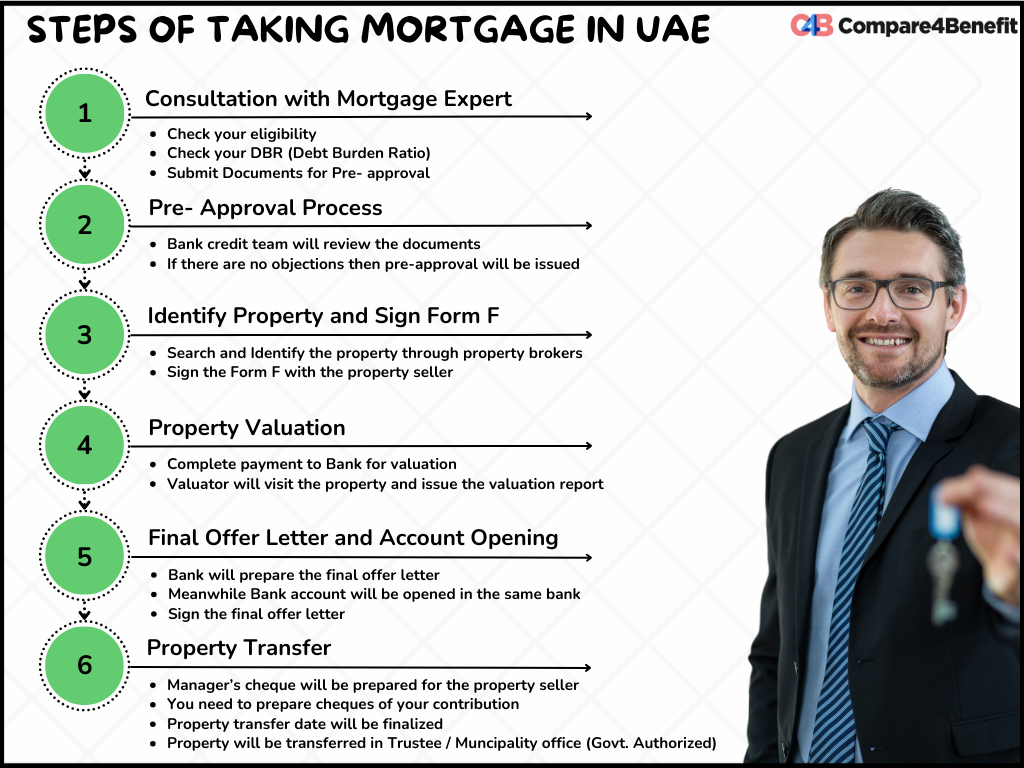

📋 Step-by-Step Home Mortgage Refine for Salaried Customers (Upgraded)

-

Talk With a Home Mortgage Professional

Begin by consulting with a specialist home loan consultant (like us at Compare4Benefit) to recognize the procedure, your choices, and obtain quality on the following actions. -

Examine Your Qualification & DBR with the Expert

Your consultant will certainly inspect your Financial Obligation Worry Proportion (DBR) and wage qualification with various financial institutions to discover one of the most ideal loan provider for your account. -

Submit Papers for Pre-Approval

Once the ideal financial institution is determined, send your papers to get a pre-approval. This offers you a conditional authorization and verifies your loaning capability. -

Complete the Building

With pre-approval in hand, you can currently with confidence begin your residential or commercial property search and pick the ideal home or financial investment. -

Authorize the MOU with the Vendor

When you’ve picked the residential or commercial property, both you and the vendor authorize the Memorandum of Recognizing (MOU). This describes the acquisition terms and obstructs the residential or commercial property for you. -

Financial Institution Performs Building Evaluation

The financial institution will certainly send out an authorized appraisal business to examine the residential or commercial property’s market price, guaranteeing it straightens with your acquisition rate. -

Last Deal Letter (FOL) is Released by the Financial Institution

After the appraisal is total and approved, the financial institution problems the Last Deal Letter (FOL) for your home loan. -

Customer Opens Checking Account & Indicators FOL

You will certainly currently open up a savings account (otherwise currently existing) in the financing financial institution and authorize the Last Deal Letter to continue. -

Financial institution Prepares Supervisor’s Cheques for Vendor

Once the FOL is authorized, the financial institution procedures and prepares the Supervisor’s Cheques to pay the vendor and cover various other fees like DLD costs. -

Transfer the Building at DLD Trustee Workplace

On the scheduled day, both events fulfill at the Dubai Land Division Trustee Workplace to finish the possession transfer. The residential or commercial property is currently formally in your name. -

Home Loan is Paid Out

After effective transfer, the financial institution pays out the home loan straight to the vendor and your payment period starts.

💼 Charges and Surprise Costs Described

Financial Institution Costs

Federal Government Costs

-

DLD cost: 4% of residential or commercial property rate

-

Trustee cost: AED 4,000–6,000

-

Home loan enrollment: 0.25% of car loan

We provide you a total expense sheet upfront—not a surprises.

🧰 Devices That Make It Easy

💡 Why Pick Compare4Benefit.com

-

Contrast from 25+ UAE financial institutions

-

Obtain special offers with non-listed business

-

Pre-approvals within two days

-

100% totally free solution for employed customers

We lead you from begin to complete.

🚀 Your Following Action

All set to take the jump?

👉 Examine qualification

👉 Contrast finest offers

👉 Schedule a totally free examination at Compare4Benefit.com

✅ Final Thought

Obtaining a home mortgage in the UAE as an employed customer isn’t brain surgery—it simply requires the ideal support. From comprehending DBR to picking dealt with vs minimizing prices, we’ve obtained you covered. With Compare4Benefit at hand, you’ll have your desire home funded in a snap—without the frustrations.

❓ Frequently Asked Questions

1. What is the minimal wage for a home mortgage in UAE?

A lot of financial institutions need AED 8,000 to AED 15,000 monthly.

2. Can I obtain a home mortgage if my business is not noted with the financial institution?

Yes! We provide non-listed business home loan choices via certain financial institutions.

3. How much time does home loan authorization absorb UAE?

First pre-approval takes 24 to two days. Complete authorization might take 5–10 functioning days.

4. Can I obtain a home mortgage as a consultant or freelance?

Yes, however it’s harder than for employed customers. You’ll require audited financials and income tax return.

5. What occurs if I miss out on an EMI settlement?

You might encounter late costs and credit history effect. It’s finest to notify your financial institution beforehand if there are any kind of problems.

Incoming Web Link Suggestions:

Outbound Web Link Suggestions: